U.S. architecture firms have been whipsawed by a weak and volatile economy over the past several years. With architecture firms losing almost 30 percent of their payroll employees during the recession, many firms have also lost design specialties, technical staff, institutional history, and key marketing contacts.

As firms continue to rebuild their practices, they also need to reshape their strategies to adjust to the new realities that are defining the practice of architecture. In some respects, this entails rebuilding their project base and lost institutional capacity. Additionally, though, it consists of refocusing their project portfolio to reflect the changing construction opportunities, and reshaping their staff to reflect the evolving workforce.

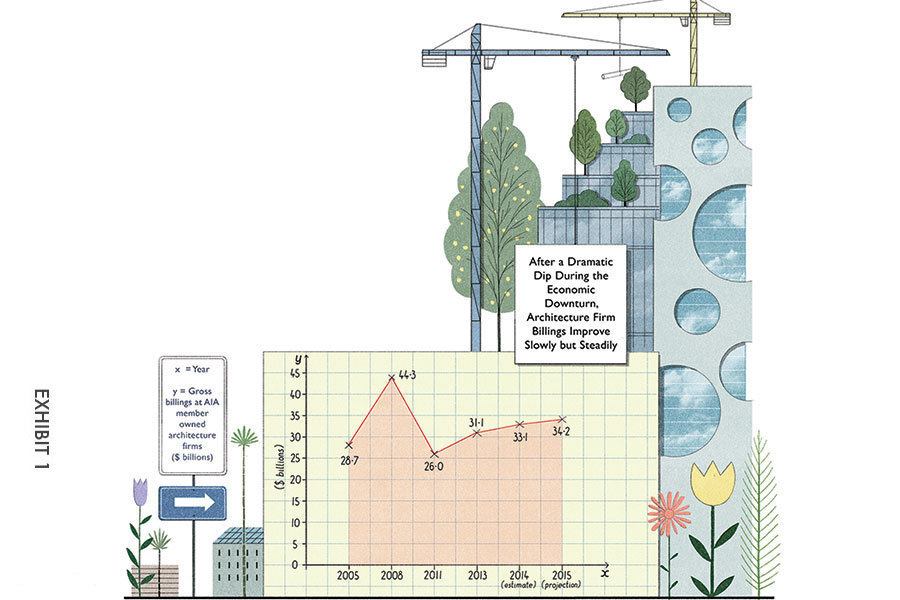

Find the Work, Get the Work

The first task for most firms is rebuilding their shrunken project base. Architecture firm billings have fluctuated wildly over the last decade, peaking at $44.3 billion in 2008 before declining by more than 40 percent over the next three years (see the “Exhibit 1” chart, above). Architecture firm billings have since begun to rebound, according to the latest figures available from the 2014 AIA Firm Survey Report, and estimates for 2014 and 2015 firm billings indicate that they should continue to increase. When asked in late 2014, architecture firms anticipated that their billings would increase by 6.5 percent for the year and projected additional modest growth of 3.2 percent for 2015.

One factor that has contributed to the increase in net billings at firms in the years since the downturn is a decrease in pass-throughs—or an increase in the cost that a client pays because of an increase in the firm’s cost. Pass-throughs accounted for more than a third of gross billings in 2008, compared to just a quarter in 2013. During the downturn, architecture firms kept more work in-house instead of using external consultants. However, as workloads continue to increase, firms may once again find themselves increasing their use of outside partners and specialists.

More Offshore

For many firms, a key source of new project activity will be international work. While the U.S. continues to have the world’s largest economy, a disproportionate share of construction activity in coming years will be in more rapidly growing areas like China; East Asia and the Pacific region; the Middle East; Sub-Saharan Africa; and South America. Though the share of architecture firm billings from international work has declined since peaking in 2008, it is expected to rebound in coming years (see the “Exhibit 2” chart, above). International work generated $1.7 billion in revenue in 2013, but that amount is only slightly more than half of the $3 billion that was generated in 2008.

The economic downturn affected countries around the world, particularly countries like Greece and Spain that continue to feel the impact today. Even in the Middle East, which was expanding rapidly throughout the late 2000s, design and construction activity has slowed in recent years. However, as these economies rebound, and technology makes it easier for firms to expand into overseas work, competition for international projects will likely increase, as will firm revenue from these projects.

A Better Mix of Talent

Staff diversity at architecture firms will need to reflect the changing composition of the national workforce. About a quarter of our national population consists of racial or ethnic minorities. Additionally, women now comprise almost half of the U.S. labor force. But when you look at architecture firms, only 20 percent of architecture staff is composed of racial and ethnic minorities, and less than 30 percent of architecture practitioners are women. The size of architecture firms has fluctuated over the last five years, from an average of 10 total employees in 2008, down to nine in 2011, and then to back up to 11 in 2013. However, the composition of architecture staff at firms has changed little, aside from an increase in the share of firms that are sole practitioners and a modest increase in the share of architecture staff that is licensed. The share of architecture staff that is comprised of women and racial/ethnic minorities has gained some ground in the last decade but still accounts for a relatively small share overall. In 2013, women accounted for 28 percent of all architecture staff but only 17 percent of firm principals/partners (see the “Exhibit 3” chart, above). However, there are higher shares of women in the pipeline, as nearly four in 10 interns on the path to licensure at architecture firms are women.

As mentioned earlier, racial/ethnic minorities make up an even smaller share of architecture staff than women. However, that share has increased by 4 percentage points since 2005. In addition, more than 20 percent of interns on the path to licensure at architecture firms are racial/ethnic minorities, as are 16 percent of licensed architects and 11 percent of firm principals/partners. Firm diversity has increased dramatically over the last several decades, and although the pace of growth has slowed somewhat in recent years, the composition of architecture firm staff should increasingly mirror the demographics of the national population in the coming years.

As economic conditions improve, architecture firms will rebuild their staff and regain some of their lost project workloads. In addition, new firms will need to respond to evolving market forces—the shifting of construction activity to the developing world and the emerging market importance of women and racial and ethnic minorities domestically—if they are to retain their leadership position in the coming decades.

Kermit Baker, Hon. AIA, is the AIA’s chief economist. Jennifer Riskus is the AIA’s economics research manager.