Entering 2008, nonresidential construction was among the bright spots in the U.S. economy. While consumers were fighting their way out of a mound of debt and coping with falling home prices in many markets, businesses were taking advantage of favorable financing costs, a healthy stock market, and emerging international opportunities, particularly given a favorably priced dollar. These conditions resulted in the need for additional nonresidential facilities.

What a difference a year makes. While a devastated housing market remains one of the few constants, we’re entering 2009 trying to cope with an international credit market meltdown, a national economy that appears to be well into a recession, and a nonresidential construction market that has suddenly reversed direction.

In this environment, it’s no surprise that architects are concerned about their future. According to ARCHITECT’s 2008 Confidence Survey, 94 percent of respondents are worried about how the economic downturn will affect their firm. At most architecture firms, commercial projects (offices, retail, and hotels) began to soften earlier this year. Recently, we’ve seen signs that even the usually vigorous healthcare and education markets will not be spared from this downturn.

As this issue goes to press, the national unemployment rate has reached a 16-year high, and architects are not being spared. Sixty-five percent of respondents know of architects who have been laid off during this downturn. And while two-thirds feel reasonably certain that their job is secure, a quarter are nervous about their prospects, and 8 percent feel that their position is almost certain to be eliminated.

This pessimism springs from client actions in the face of a weaker economy. Almost half of respondents report that one or more projects at their firm have been canceled in recent months, while almost eight in 10 report at least one project put on hold. Of those projects that are continuing, budget cutbacks are common.

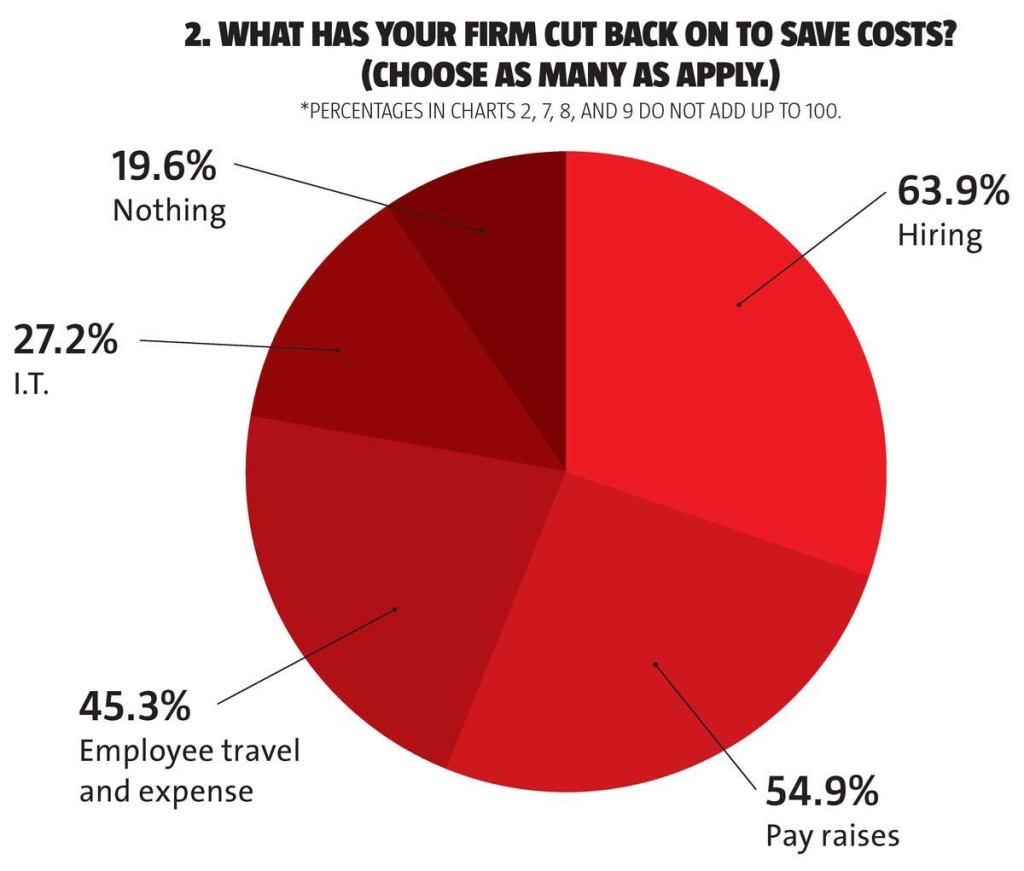

With increasingly frequent cutbacks by clients, architects report that their firms are also implementing cost-cutting measures. Almost two-thirds of respondents report hiring cutbacks at their firm, over half are seeing more modest staff pay increases, and others report restrictions in expenses like I.T. investments and travel.

Business cycles are unpredictable, but many respondents are preparing themselves for the worst. Just over 60 percent feel that we’ll see better conditions sometime in 2010, while 30 percent feel that the economic and construction downturn will remain through 2011 or 2012. The remainder are bracing themselves for a downturn that will extend beyond 2012.

Kermit Baker is chief economist of the AIA and a senior research fellow at Harvard University’s Joint Center for Housing Studies.