The technological revolution that is just beginning to hit the AEC industry has the potential to dramatically lift profitability for firm owners—and in doing so lift compensation for architects. To get there, firms will need to have a better strategic vision of how to harness these technologies to make the design process more efficient.

Architects, as well as the entire AEC industry, have been on a solid run over the past several years. Since the current construction recovery began in 2011, spending on construction projects nationally has increased almost 10 percent per year and, as a result, payrolls at architecture firms have increased about 4.5 percent annually. As a profession, architecture is almost back to where it was when the Great Recession began in 2008.

Business conditions have been so good that we may not have noticed that the design professions are still stymied by many of the same old business problems. Fees continue to be under tremendous pressure, even though many firms have more work than they can comfortably handle. Maintaining profitability remains a challenge for a significant share of firms. Compensation for architects continues to be well below that of other professions with comparable educational requirements; architects bemoan the fact that many of their college classmates who chose careers in law, medicine, business management, or technology had higher starting salaries than they likely will see even after 15 to 20 years of architectural practice.

There are many reasons why architectural practice remains challenging from a business perspective. Phillip Bernstein, an associate dean and senior lecturer at the Yale School of Architecture, points to the architecture business model as the chief culprit. Many firms price their services as a commodity—for a fixed price or as a percentage of the costs of construction—which typically doesn’t provide a premium for a superior design solution. If architects were instead rewarded based on the performance of their designs—health facilities that improved health outcomes, schools that enhanced educational performance, or offices that commanded higher rents—owners would no doubt be willing to increase fees commensurate with these outcomes.

But there may be a more basic reason for the business challenges that the profession faces. Key to increasing employee compensation and business profitability is to increase the productivity of the workforce. Productivity is the measure of how much output can be produced in a given period of time. Since it is fundamentally a manufacturing concept, productivity is a bit trickier to apply to service industries like design because quality is integral to determining the value of a service. The quality of one’s work is often more important than the quantity. However, the basic relationship is the same: If architects produce more high-quality services, firms will generate more revenue.

Even with the significant complexities that surround the measurement of architects’ productivity, there are good reasons to factor this concept into the analysis of how well the profession is performing. On its face, the results are not good. Twenty years ago, architects, as a profession, were designing almost 20,000 square feet of nonresidential space in the U.S. for each architectural position at U.S. firms. Currently, this figure is just half that, under 10,000 square feet per architectural employee. However, this situation is not as bad as it appears. Architects are doing more building renovations and retrofits, which don’t increase the amount of building space. They are also providing clients with additional design services that don’t directly translate into additional space—including space planning, zoning and code compliance, historic preservation, and sustainable design—and providing planning and predesign services as well as post-construction operations and maintenance services.

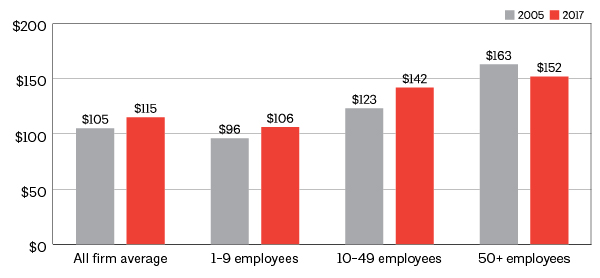

Since design activity doesn’t always show up as increased building space, firms more traditionally look at net revenue per employee as a proxy for the concept of productivity. Conceptually, this measure makes sense, since the services that clients are willing to pay for are probably a reasonable measure of an architect’s productive activity. However, even this measure doesn’t paint a very favorable picture for trends in architect productivity. Net revenue per employee (adjusted for inflation) has increased only modestly in recent years— less than 1 percent per year on average between 2005 and 2017. For larger firms, this measure of productivity declined over this period (Figure 1).

FIGURE 1: Net revenue per employee has increased only slightly over past decade. Revenue per employee, in thousands, average across all firms, in 2017 dollars.

Emerging Technologies and Improvements in Productivity Gains

In most industries, new technologies have been the critical pathway to increased productivity: Think Henry Ford and the automotive assembly line that allowed workers to focus on a single repetitive task, or more recently, computers, the internet, smartphones, and—in the case of architects—AutoCAD and BIM.

While there may be some debate as to whether design software has made architects more productive, increasing productivity in service industries like architecture is a challenging task. Technology may improve the quality of the service provided (better building designs) but not the quantity provided (more building designs). For architecture, like many service industries, quality is often difficult to measure.

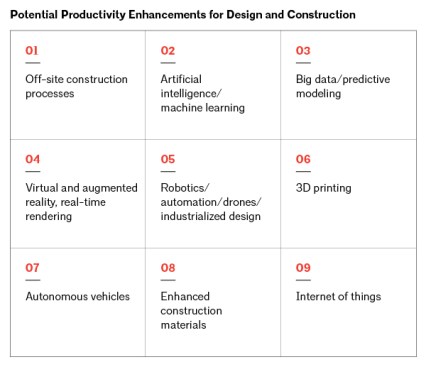

Still, several new technologies currently being developed and applied could dramatically affect the productivity of architects, including:

- Virtual reality, augmented reality, and real-time rendering: to visualize, test, and validate designs;

- 3D printing: for design models and, potentially, on-site production of construction products;

- Big data and predictive modeling: to monitor consumer behavior, construction processes, and project history;

- The internet of things, including sensors that generate data: to control systems and monitor behavior; and

- Artificial intelligence and machine learning: to generate best practices and prototypes.

Architecture is not the only field that is witnessing a revolution of new technologies. Others could dramatically change the construction process or the environment in which design and construction occur. These emerging technologies include:

- Enhanced construction materials: such as specially cured concrete, smart fenestration, microbiology, nanotechnology;

- Robotics, automation, drones, and industrialized design: to improve productivity in construction;

- Off-site construction processes: such as prefabrication, modularization, and preassembly; and

- Autonomous vehicles: that will influence building designs, use of space, and locational choices.

However, most of these emerging technologies are largely unproven in terms of how they could influence the AEC industry. And even if there were a consensus that a technology could potentially reshape the profession, the timing of that change is unknown. The time frame for the adoption of generally accepted technologies is surprisingly long and unpredictable.

The adoption cycle for BIM is a good example. An AIA survey estimated that in 2005 about 10 percent of architecture firms were using BIM on billable projects. Since then, it has come to be viewed as the industry standard and it is used by virtually all firms with 50 or more employees. But as of 2017, fewer than half of all U.S. architecture firms reported using BIM on billable projects, and over a quarter of firms don’t use BIM and have no plans to use it in the future.

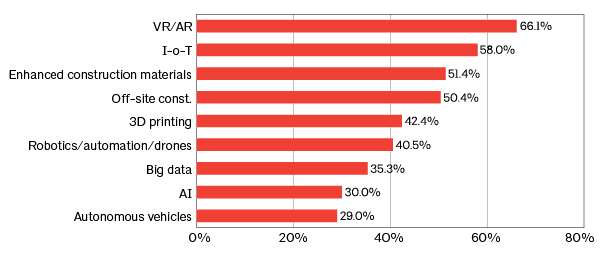

Still, architects are confident that many of these emerging technologies will have a significant impact directly on architecture or on the AEC industry more broadly over the coming decade. In a survey conducted in April 2018, architect respondents were asked which emerging technologies would have a significant impact on the AEC industry over the next five to 10 years. Almost two-thirds felt that virtual reality (VR) and augmented reality (AR) would become popular technologies, likely because of the growing adoption of BIM that facilitate the use of these related applications. Other technologies were viewed as being almost as significant, with the internet of things, enhanced construction materials, and off-site construction processes viewed as having a very significant impact on the AEC industry over the next five to 10 years by more than half of architecture firms (Figure 2).

FIGURE 2: Emerging technologies are predicted to impact the industry over the coming decade. Share of firms rating trend as "very significant" in terms of impact to AEC industry over next 5-10 years.

The Productivity Disconnect

These results suggest that architects are surprisingly bullish regarding the potential impact of emerging technologies on design practice and construction techniques. Despite their enthusiasm, however, the emerging technological revolution is likely to have minimal impact on architect productivity for the foreseeable future for three reasons:

- Firms have a difficult time not only implementing productivity improvements but even assessing whether productivity is a major concern that they should be addressing;

- To the extent that they view productivity as a concern, firm leaders generally focus on more immediate and tangible fixes, not on introducing unproven technologies where the benefits are unlikely to be realized for many years; and

- Many architecture firms strive to be perceived as technologically sophisticated. This goal may encourage them to remain fluent with emerging technologies, but not to encourage them to actually implement the technologies in their practices.

Also, given that productivity of architects is difficult to measure, it’s easy for firms to think that their productivity is better that it is. In a recent survey of architecture firms, most felt that their firmwide productivity levels had increased over the past few years. When asked how they would rate their architecture staff ’s productivity compared to that of their peers, only one in six firms felt that their staff was less productive than that at their peers, a third felt that they were as productive, and half felt that they were more productive. Many firm leaders thus must be overestimating the productivity of their staff.

Even though architecture firms generally believe that their productivity will increase in the coming years and recognize the potential of these emerging technologies to reshape the profession, most focus on more immediate issues to improve their practices’ day-to-day operations. For example, most architects use smartphones and tablets on projects, and most use cloud computing to make project information more accessible. By way of contrast, however, very few use VR or 3D printing for billable project tasks.

When asked in a recent survey to identify one thing that they would do to improve productivity at their firm, access to emerging technologies was rarely mentioned. Only 5 percent of firms mentioned anything that had to do with technology, and most proposed innovations that involved enhancements to their current AutoCAD and BIM systems, not an implementation of any new and emerging technologies.

Instead, firms were quick to point to the need for improved training or professional development for their staff. Over a third of firms listed the need to hire more experienced staff as their single best action to improve productivity. Improving project management, coordination, and communications among the project team was the next most commonly desired productivity enhancer, listed by more than a quarter of firms. Improving firm strategy, operations, systems, and management resources was a common response, with almost 20 percent of firms selecting an action in this category. Avoiding nonbillable outside distractions (such as texting, email, and social media), better cooperation from clients in making key project decisions, better definition of the scope of projects, and avoiding overdesign were also mentioned.

While harnessing emerging technologies doesn’t seem to be a prime motivation for improving productivity at firms, developing or maintaining technological proficiency is a priority for many. When asked to characterize the degree of technological sophistication among their staff and at their firm on a five-point scale—from “not technologically sophisticated” to “very sophisticated”—almost three-quarters rated their firm as either 4 (fairly sophisticated) or 5 (very sophisticated).

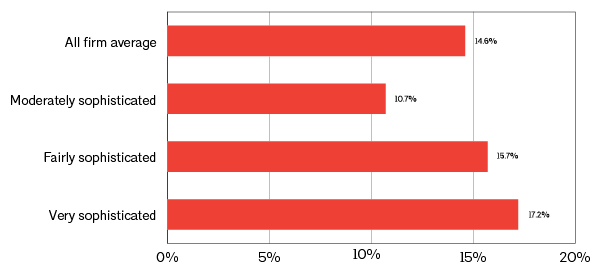

This focus on technological competence apparently encompasses more traditional products and systems rather than emerging technologies. However, this strategy has been very successful in generating better results for firms through more-efficient operations, improved communication across the design team, attracting better employees, or producing a better-trained staff. Firms that rated themselves highly in terms of technological sophistication have been performing better recently, with above-average revenue growth for 2018 as well as above-average profits for the year (Figure 3).

FIGURE 3: Technologically sophisticated firms have been more profitable. 2018 profitability by perceived technological sophistication, average percent across all firms.

It may be that the adoption of emerging technologies has less to do with staff productivity and firm profitability, and more to do with the fact that productive and profitable firms are more likely to promote an image of being on the leading edge of pursuing new ideas.

FIGURE 4: Potential productivity enhancements for design and construction.