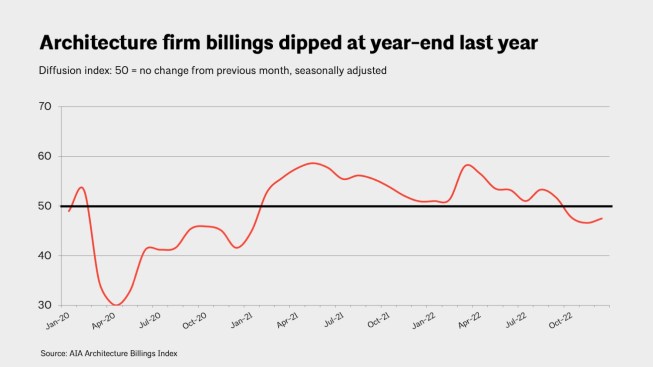

Another design recession appears to be developing at architecture firms. Design billings declined in the fourth quarter of last year, according to AIA’s Architecture Billings Index (ABI), and on average firms are expecting no gains in revenue this year. However, large design backlogs matched by equally large backlogs at construction companies should help provide a bridge to the next design expansion. In the meantime, firm leaders are expressing concerns in three main areas in navigating this unexpected downturn: tightening project management given all the uncertainty, maintaining firm profitability, and coping with staffing issues.

Architecture firms enjoyed less than three years of healthy business conditions between the onset of the pandemic in the United States in March 2020 and the emerging downturn at the end of last year. However, over this period, firms experienced some of the strongest growth that they had seen in decades, leading to a growing shortage of staff across the profession. It was also a period of chronic supply chain disruptions for key construction commodities; the highest rate of inflation in the economy in four decades; and rapidly rising interest rates. These trends put pressure on firms to develop affordable designs in an environment of rapidly rising costs, help clients navigate the construction process that was constantly under pressure from cost escalation and scheduling delays, and potentially offer materials substitutions or design solutions when preferred items were unavailable or unaffordable.

Construction Follows Suit

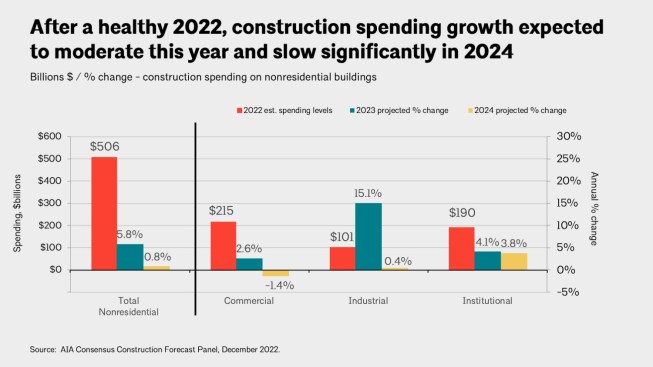

The nonresidential building construction market traditionally follows a similar pattern to design activity, just with a considerable lag. Spending on the construction of nonresidential buildings didn’t begin to recover from the pandemic-induced downturn until the latter part of 2021, but in 2022, as much of the rest of the economy was reeling under the pressure of high prices and supply problems, spending on the construction of buildings increased at close to a double-digit pace. The fact that nonresidential construction payrolls increased by almost 4% that year points to significant growth in construction activity beyond just higher input costs, as reflected by the ABI numbers from that time period.

However, the healthy pace of growth in construction spending in 2022 masks the unevenness of those gains. While the commercial/industrial sector increased by more than 15%, according to the ABI, spending on institutional facilities hardly saw any improvement.

And even while the robust commercial/industrial sector saw increases, including in manufacturing and distribution facilities, offices and lodging facilities saw virtually no growth.

This uneven nature of the growth in nonresidential building activity has accelerated with economic developments that evolved during the pandemic. For example, spending on the construction of manufacturing facilities almost doubled between February 2020 and the end of last year, per U.S. Department of Commerce construction spending data. Manufacturing gains have resulted in large part from reshoring efforts by U.S. companies to limit their exposure to supply disruptions. The Reshoring Institute estimates that reshoring and other foreign direct investment in the U.S. produced 350,000 manufacturing positions in 2022, almost three times the annual average of the prior decade.

Likewise, due to explosive growth in e-commerce activity during the pandemic, the distribution component of the retail category has seen strong gains in construction. The pandemic also has been a boon for data centers, due to the adoption of cloud computing with remote work. The largest end users of data centers—financial services, IT and telecom, government, and energy and utilities—have been some of the fastest growing sectors in our economy over this period.

At the other extreme, the pandemic significantly curtailed business and personal travel. By the end of 2022, U.S. Department of Commerce data tells us that spending on lodging declined almost 40% compared to pre-pandemic levels. Also, remote work became much more common during the pandemic, reducing the need for office space. Spending on office construction over this period declined 10% relative to pre-pandemic levels.

A key question that construction forecasters are grappling with is the extent to which sectors seeing strong growth in recent years have overshot market demand, and those seeing declines have undershot longer-term potential. The real estate market offers insights in this regard. For example, office vacancy rates nationally are in excess of 17%, while they have averaged 14.5% over the past two decades, according to the Urban Land Institute, indicating an excess supply of office space. In contrast, industrial availability rates are averaging under 5%, having averaged almost 10% over the past two decades.

Factoring in all these trends, the AIA Consensus Construction Forecast Panel is projecting spending on nonresidential buildings to increase almost 6% in 2023, down from the almost 10% growth in 2022. Next year, growth is projected to slow to under 1%. Much of the anticipated growth this year will come from the industrial sector, while next year the institutional sector will provide most of the meager growth that is expected.

Different Strokes Required for This Down Cycle

If the current weakness in design activity continues, architecture firms will confront their second design downturn in less than three years. While managing business through a downturn may be fresh in firm owners’ minds, this cycle needs to be treated very differently than the pandemic downturn in early 2020.

As the pandemic hit the economy in the U.S., much activity stopped suddenly. Many architecture firms were forced to temporarily cease operations, as were many construction job sites. The underlying health of the economy was generally not a concern; rather, it was a question of when public health conditions would permit a reopening of activity. As a result, revenue at architecture firms immediately plummeted to levels not seen in any prior economic cycle in decades, according to AIA research.

The driving forces of this cycle have been supply chain disruptions causing spiking prices and availability issues for construction commodities, elevated rates of inflation for many construction inputs, rising interest rates and more restrictive financing terms for construction projects, and a labor shortage both for architects and construction workers. With supply chains beginning to get back to normal, inflation rates beginning to ease, and long-term interest rates stabilizing, many feel that this downturn will be relatively mild and short-lived.

This optimism is supported by two other factors. Architecture firms have seen growing backlogs over the past decade. In large part this was the result of a surge in demand for facilities, coupled with labor shortages that forced design and construction schedules to be extended. Many firms feel that their current project backlogs—averaging almost seven months entering 2023—will serve as bridge to a recovery in the demand for design services.

Additionally, smaller reconstruction projects (perceived as more stable by firm owners) have come to dominate the design portfolio at many firms. The AIA recently reported that more than 60% of revenue at both commercial/industrial firms and institutional firms is derived from reconstruction projects. These projects have become more popular in recent years because of their favorable sustainability potential, as well as the ways that the pandemic has reshaped consumer demand. Architecture firms recently reported that adaptive reuse is the most common goal of their portfolio of reconstruction projects.

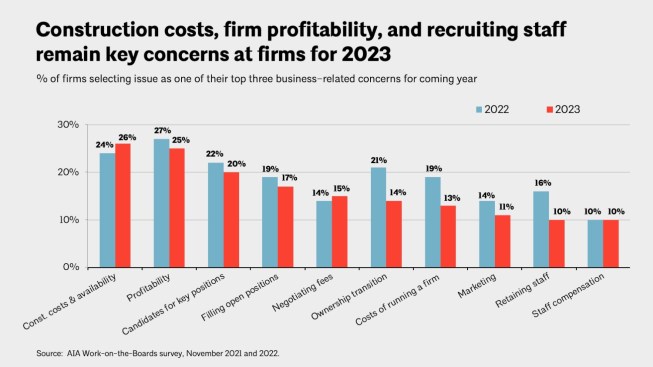

As a result of the often-unique characteristics of this current economic cycle, architecture firms are finding that many of their priorities are shifting as they attempt to manage through this current period of economic weakness. When recently asked to rank their top business-related concerns heading into 2023 via AIA’s Work-on-the-Boards survey, they largely fell into three categories:

- Tighter project management: Given the uncertainty surrounding materials costs and availability, architecture firms often have had a difficult time designing projects within the client’s budget. Per AIA’s Work-on-the-Boards survey, more than a quarter of architecture firms ranked coping with volatile construction/building materials costs and availability as one of their top concerns (out of three) entering 2023. While this issue seems to be resolving itself as the economy cools, firms have been largely helpless in dealing with this problem over the past two years, and therefore are wary that it may re-emerge in the future.

- Firm profitability: Profitability chronically makes the list of top concerns at firms, but there is a slightly different twist this time. Firms have seen operating costs increase dramatically over the past year with the costs of healthcare, technology, and employee benefits all on the rise. The key area, however, is staff compensation given the extremely tight labor market. There are two broad strategies for firms to deal with this situation: increasing revenue or cutting costs. Increasing revenue given the currently overstretched staff resources at many firms is difficult, if not impossible. Likewise, cutting costs is even less feasible in this economic environment given that, far and away, the largest expense category is staff compensation. Most firms have had to raise compensation to attract new staff and retain their current employees. As a result, profitability has suffered, which is why a quarter of firms name this issue as one of their top three concerns for 2023, per the Work-on-the-Boards survey.

- Staffing: Half of the top 10 concerns of architecture firms entering 2023 are related to staffing, labor, and firm leadership issues, per the Work-on-the-Boards survey. These were also five of the top 10 concerns for 2022, so staffing is becoming a chronic issue in architecture. However, there are several dimensions to the staffing and labor issue. The first deals with firm leadership and filling key positions. Ownership transition has become a major issue with the ongoing retirement of members of the large baby-boom generation. A related issue is filling key positions within the firm. As firms have grown in recent years, their ability to staff critical positions by promoting from within is often limited, per AIA’s Work-on-the-Boards survey, and recruiting senior staff from outside the firm can be very challenging in this economic environment.

A related issue is the general problem of filling open positions and retaining current staff. Even in the face of a severe staffing shortage, firms added only 1,300 payroll positions nationally over the last three months of 2022, which accounted for only .5% of all payroll positions at architecture firms, according to the U.S. Department of Labor.

Finally, and clearly related to the other two staffing challenges, is the issue of staff compensation. In a period characterized by high inflation, pressure on firm profitability, and labor shortages, compensation levels are a critical concern. However, increasing compensation does not help to resolve profession-wide staffing shortages, at least in the short run. When asked to evaluate their level of concern with almost 50 potential business issues, firms cited staffing among the top 10 most pressing.