A perennial concern for architects is whether or not there are sufficient numbers of practitioners to serve the evolving needs of the profession. It seems as though the “sweet spot” of staffing is elusive—what seemed like a surplus of architects yesterday has morphed into a deficit today. Architecture firms, most of which fit the definition of small businesses, are not well-equipped to continually rightsize their staffing. Downsizing is an extremely painful experience for both firm owners and employees. Adding staff under the pressure of growing workloads is almost as difficult, given the training time typically required before new staff are fully productive.

Architecture firms have developed several coping mechanisms to deal with their need to adjust staffing to shifting project workloads. When there are insufficient workloads, in addition to reductions in staff, firms may reduce the hours that regular staffers work, rely more on contract or part-time workers, or freeze or even reduce compensation. When workloads are excessive, in addition to adding staff, firms might offer overtime, outsource work to other firms or offshore service providers, extend the proposed project schedules, cut back on design services offered, or even not bid on projects that might otherwise fit their skill set.

None of these strategies to cope with staffing are ideal, either from the perspective of an individual firm or for the overall profession. We lack a methodology for thinking about current staffing requirements across the profession and, more importantly, about what we’ll need five or 10 years from now. These concerns motivated us here at the AIA to think about a process for estimating our current needs and projecting our likely future needs. Given that many of the variables of projecting future needs are likely to change—new design software will alter how productive we are, new services for clients will be proposed, and more international work will be done by U.S.-based firms—these projections will need to be continually enhanced and updated.

Our approach here attempts to estimate the current need for architectural staffing at firms by examining the historical relationship between construction activity and architecture positions. Additionally, these needs over the coming decade are projected by estimating the additional staff that will be required to accommodate future growth in construction activity, as well as to replace current staff who will be leaving the architecture workforce.

Our major conclusions are twofold. First, while in the past there have been major gaps nationally between existing architectural staff and the number required to handle current workloads, at present this gap is at historically low levels. Second, we’ll need about 25,000 additional architectural staff over the coming decade to handle growth in the construction industry and replace those who will leave the workforce. This need accounts for about half of all future graduates of accredited architectural programs nationally who are eligible to work in the United States.

What’s the Current Need for Architecture Staff?

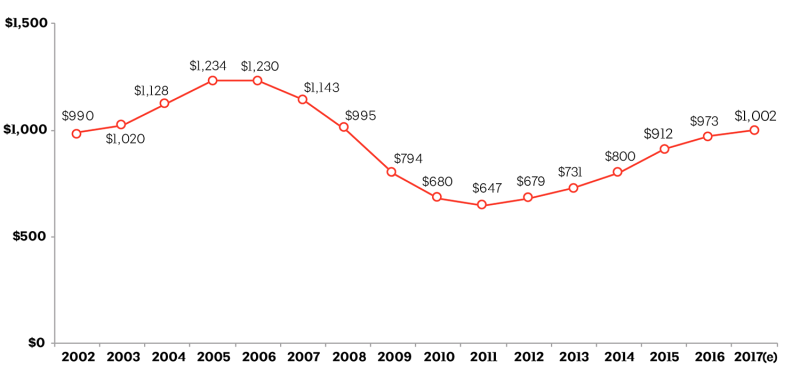

Domestically, the amount of staff needed is largely driven by the amount of residential and nonresidential building activity. Unfortunately from the perspective of determining the need for architectural positions, the business cycle of the construction industry varies considerably, causing the amount of activity to change significantly. While this past cycle was more extreme than most, it does still illustrate how quickly the levels of building activity can change. For example, construction spending for homes and buildings declined by almost half between the 2005/2006 high and the 2011 low, and spending through 2017 is up more than 50 percent from that low point (Fig. 1).

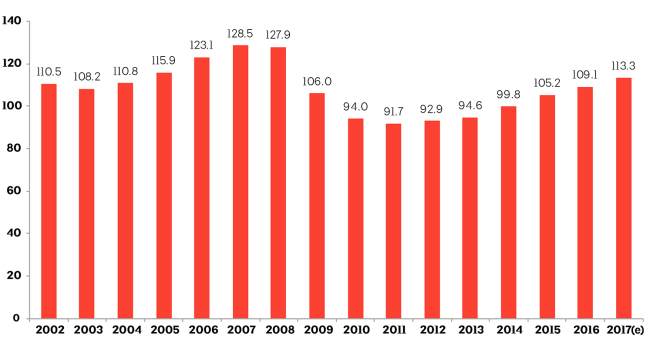

Architect positions at firms reflect this volatility in construction activity. For the past cycle, the AIA estimates that the number of architecture positions at U.S. firms declined by almost 30 percent between the high in 2007 and the low in 2011. Through 2017, architecture positions have increased by almost 25 percent from that 2011 low. While dramatic, these changes have been less extreme than those in the underlying construction activity, suggesting that firms might not totally adjust their staffing to account for changes in overall market activity levels (Fig. 2).

Figure 2: Number of architecture positions at U.S. firms has been slowly recovering after steep decline during the recession. Estimated number of architecture positions at U.S. architecture firms, in thousands.

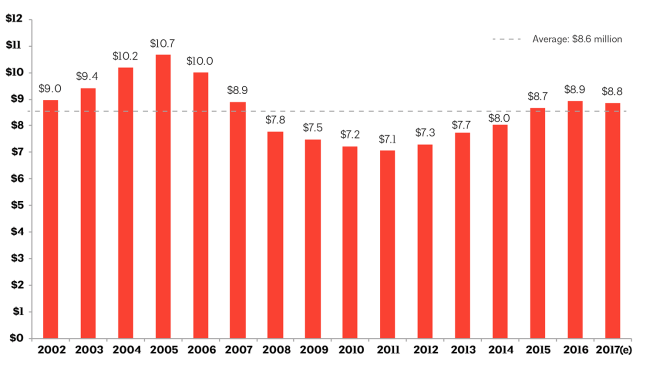

Construction cycles also appear to influence the output of architects. During periods of strong growth in construction spending, the value of construction activity per architect rose; during construction slowdowns, the same metric declined. Over the past decade and a half, an inflation-adjusted average of $8.6 million of building construction has been generated annually by each architectural position in the U.S. Since this average was calculated across years of strong growth as well as steep declines in construction activity, it is used here as an estimate of the typical relationship between architectural staffing and construction activity. On average, we would expect to see a continuing average of $8.6 million of construction activity generated every year for each architectural position (Fig. 3).

Figure 3: Architectural staffing positions don’t adjust as quickly as construction activity, causing average output to fluctuate. Estimate of construction activity per architectural position, in millions of 2017 dollars.

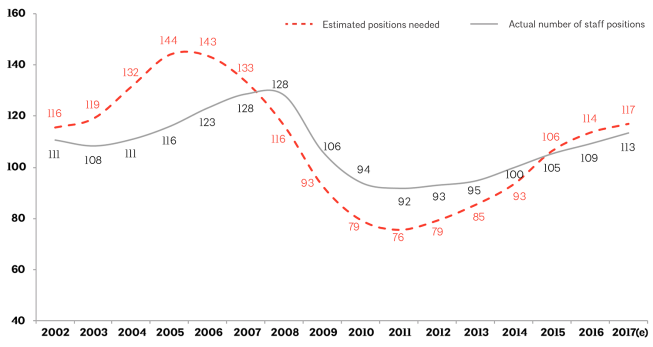

Over the past 15 years, there have been periods of considerable discrepancy between the actual number of architectural positions at U.S. firms and the estimated number of positions needed to produce the total amount of construction activity nationally. During the construction boom of 2002 to 2007, there was a significant estimated undersupply of architectural positions. During the downturn of 2008 to 2014, an apparent oversupply existed, with more positions than were estimated to be needed. Beginning in 2015, market conditions shifted to another apparent undersupply of architectural positions, estimated at just under 4,000 nationwide at the end of 2017 (Fig. 4).

This analysis of estimating architectural needs by the amount of construction activity ignores many other complicating factors we face in estimating the need for architectural staff. While difficult to explicitly build into any analysis, the following factors are among those that help refine the estimates of the number of architectural positions required in our economy:

• Location where architects are needed and where they are available

• Characteristics of projects, such as new construction vs. building renovations, or complex vs. more straightforward design solutions

• Staff productivity improvements as a result of experience, training, or new technologies

• Skills required by a firm, compared to those available in the applicant pool

• Range of services offered by the firm, such as facilities planning, predesign, and post-occupancy

• International work done by U.S. firms that isn’t reflected in the construction figures

• Design work done by paraprofessionals or other design professionals that might otherwise be done by architects

Figure 4: While understaffed during boom and overstaffed during bust, labor needs are more in balance at present. Annual estimated architectural positions needed vs. actual number of positions, in thousands.

How Many More Will We Need Over the Coming Decade?

Moving forward, our economy will need additional architectural staff to both accommodate a growing construction sector and replace current architects who are leaving the workforce, most notably due to retirement. Comparing these needs to the number of architects entering the workforce—principally graduates of professional architectural programs who are seeking careers in private practice—will determine whether we’re likely to have a deficit or surplus of architects.

The U.S. Department of Labor projects that over the coming decade (2016–26), overall employment in our economy will grow by 7.4 percent. Many of the fastest-growing occupations will be in the areas of technology (e.g., software developers), healthcare (e.g., home health aides), and alternative energy (e.g., solar photovoltaic installers).

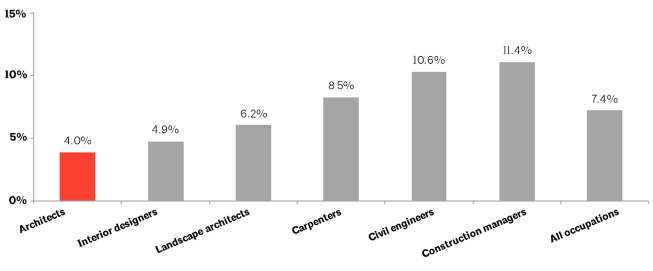

Architect positions are projected to grow only 4 percent over the next 10 years, slower than the overall growth rate and even somewhat slower than related design professional positions such as interior designers and landscape architects. Many construction-related positions are expected to grow at a faster pace, likely due to the present extreme worker shortages in many construction specialties (Fig. 5).

Figure 5: Architecture positions are projected to increase by 4 percent this coming decade, a slower pace than in related occupations. Projected change in employment, by percent, 2016–26.

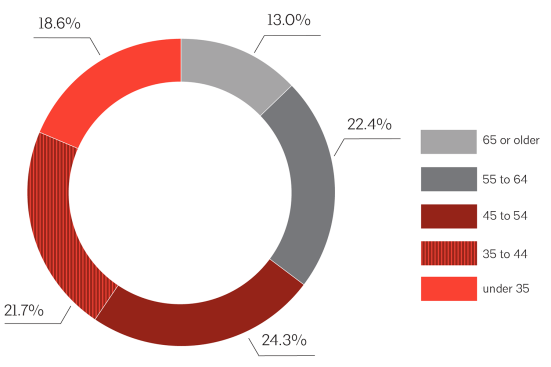

More significant than generating a need for future architects is replacing current employees who will leave the workforce, particularly due to retirement. As with the overall U.S. workforce, the architecture profession is aging. Because 13 percent of current architect members of the AIA are at least 65 years old and an additional 22 percent are between 55 and 64, we can expect significant numbers of architects to retire in the coming years. According to an AIA survey of firm leaders conducted in the summer of 2015, architecture firms expect that almost 10 percent of their current professional architecture staff will retire or significantly curtail their involvement in the firm over the next five years (Fig. 6).

Figure 6: Like our overall population, the architect profession is aging. Age of AIA architect and associate members, 2015.

Given the considerable amount of the current architect population who are nearing traditional retirement ages (35 percent of whom are 55 or older), it might be expected that the share of architects retiring over the coming decade would be even higher. Complicating this is that many workers, including architects, are working beyond traditional retirement ages. This may be because of financial losses during the Great Recession, or, as longevity increases, concern over having enough money for a longer retirement. The Labor Department projects that the share of the U.S. labor force that is 65 or older will grow substantially over the coming decade. Some of this is that more baby boomers will move into this age range, but more older workers are also staying in the workforce longer. A decade from now, more than one in 10 persons 75 and older are projected to still be in the workforce.

The additional architects needed to both accommodate future growth in the industry and replace those leaving the workforce will come primarily from the pool of graduates of architecture programs. Just over 6,000 professional architecture degrees were awarded in 2016, according to the National Architectural Accrediting Board (NAAB). While this figure is about 3 percent below the average number of degrees awarded during the prior five years, those previous years may have seen inflated numbers of degrees due to the recession, when students used a weak labor market as an opportunity to go back to school to earn an architectural degree.

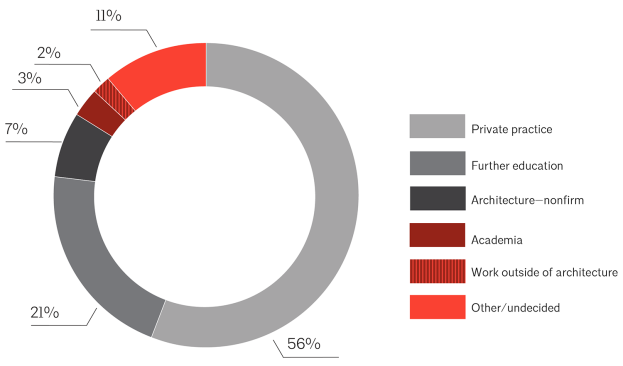

Figure 7: Most architecture students plan to continue in the profession and work in private practice. Architecture student plans after graduation, by percent.

Not all of these graduates are currently eligible to seek permanent employment in the U.S. About 15 percent of professional architectural degrees awarded in 2016 went to nonresident aliens, according to the NAAB, and that share has doubled since 2009. Additionally, not all graduates are looking to pursue careers in private practice. According to a 2016 survey of post-graduate plans for architecture students, more than half were planning for a career in private practice and another 12 percent were planning on pursuing a different career in academia, while almost a third were planning on further education or were undecided about their career path (Fig. 7).

On net, there will be a projected need for approximately 25,000 new architecture positions over the coming decade—5,000 due to industry growth and 20,000 due to retirements and other losses to the architecture labor force. This need will be met by the estimated 60,000 professional degree recipients over the coming decade; about 50,000 of whom will be eligible to seek permanent employment in the U.S., with more than half of them immediately seeking a career in private practice post-graduation and another 15,000 who may eventually seek a career path in private practice.

Currently, the gap between available architects and those needed to support growth in our economy has narrowed and may disappear in the coming years as we get further into the current construction cycle. Over the coming decade, the need for architects should be accommodated by architectural graduates entering the workforce. If either the Labor Department projections for the number of architects needed to accommodate growth or the retirement rates for architects currently in the labor force are overly conservative, there should still be sufficient numbers of graduates to accommodate what will be needed.

However, in addition to managing the inevitable volatility in demand for architectural services across the business cycle, another issue may prove to be more challenging: the potential mismatch between the training of candidates looking to fill positions and the skills that firms are seeking.

Architecture firms regularly note the difficulty of matching the skills that they need with those possessed by available candidates. Sometimes this concern is caused by the general level of experience of applicants, and other times it is specific skills. A 2015 AIA survey of firms looking to fill architectural positions found that more than half reported that finding candidates with either the required technical skills or project management skills was a major problem, while another third indicated that finding candidates with experience in the specialties that the firm offered was difficult. And this concern does not appear to be easing. According to an AIA firm leader survey conducted in late-2017, almost 80 percent of architecture firms felt that over the next few years there would be shortages of architecture staff to meet the needs of firms in their area.

AIA chief economist Kermit Baker, Hon. AIA, is a senior research fellow at Harvard University and project director of its Remodeling Futures Program.

Data Sources. Figure 1: U.S. Census Bureau. Figure 2: U.S. Department of Labor payroll survey, with AIA estimates that architecture positions account for 60 percent of overall staff positions at firms. Estimates do not include architecture staff at firms with no payroll positions. Figures 3 and 4: AIA estimates from U.S. Census Bureau construction spending data, and AIA estimates of number of architectural positions. Figure 5: U.S. Bureau of Labor Statistics; Occupational Outlook Handbook: 2016–2017. Figure 6: Estimates from the American Institute of Architects membership file. Figure 7: Design Intelligence as reported in Architectural Record, September 2016.