For another month, architecture firms across the United States found themselves operating in an economy defined less by momentum than hesitation.

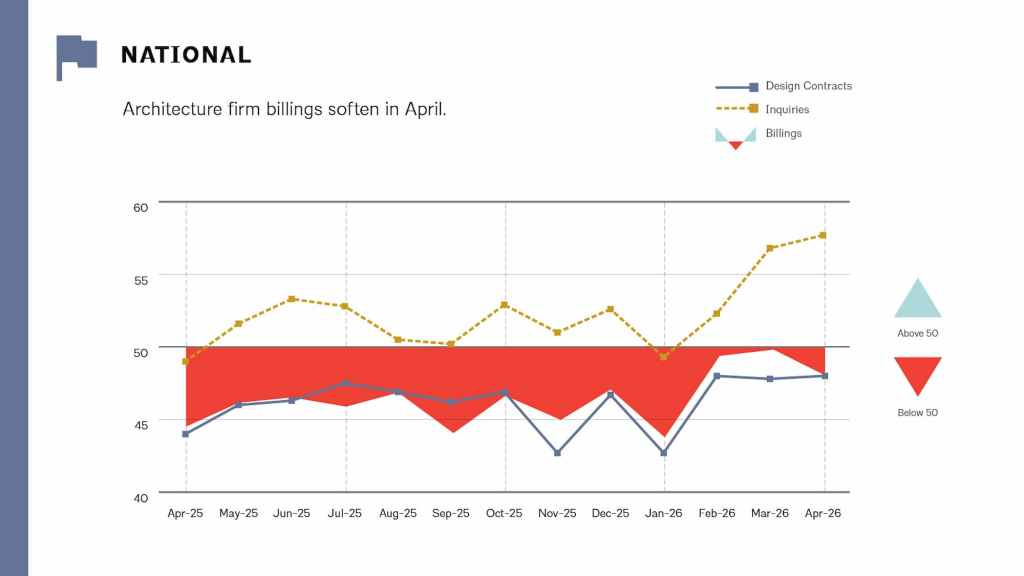

The latest AIA/Deltek Architecture Billings Index (ABI) shows that billings at U.S. architecture firms declined again in April, extending a downturn that has now persisted for more than two years. The ABI slipped to 48.3 in April from 49.8 in March, remaining below the critical 50-point threshold that signals growth.

While the latest numbers suggest the pace of decline may be moderating, the broader picture remains troubling: national architecture firm billings have now stayed in contraction territory continuously since January 2023.

That prolonged slump reflects mounting pressures rippling across the building industry—from inflation and geopolitical instability to rising energy costs and persistent uncertainty around financing and development.

“Architecture firm billings declined modestly in April as broader economic instability continued,” the report stated.

For architects, the ABI’s extended weakness is more than just an industry statistic. Because architectural billings typically precede construction activity by roughly nine to twelve months, the index is often viewed as one of the clearest leading indicators of future building activity in the United States. Continued softness in billings suggests many developers and institutions remain cautious about launching major new projects.

But the April report also revealed an industry that may be stabilizing unevenly rather than collapsing outright.

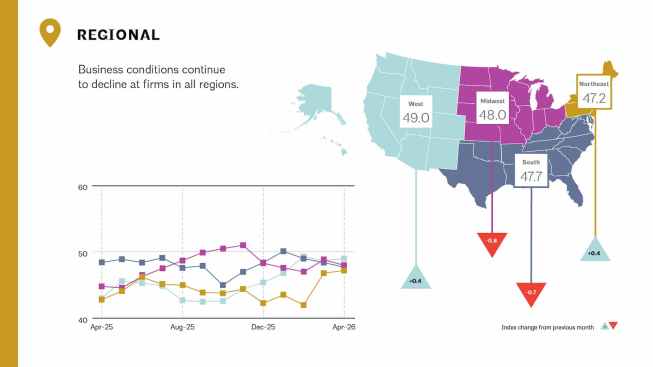

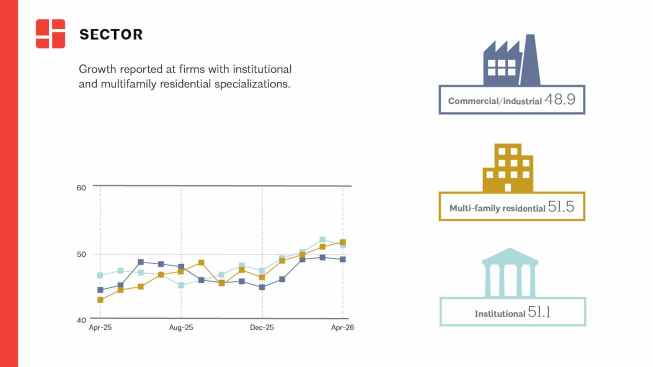

Business conditions remained soft across most regions and sectors, though some areas showed modest signs of resilience. Firms in the South reported slight improvement after suffering earlier declines this year, while institutional and multifamily residential firms posted modest growth in April.

That marks an important shift for residential architecture, which has spent much of the past two years under pressure from high borrowing costs, elevated construction prices, and slowing development activity.

Commercial and industrial firms, however, continue to face steeper headwinds. The sector has remained among the weakest parts of the market for the past six months, reflecting ongoing uncertainty around office demand, corporate expansion, and industrial investment.

Regional differences are also becoming increasingly pronounced. Firms in the West were the most likely to report declining billings for the third consecutive month, underscoring how some of the nation’s largest development markets continue to struggle with the lingering effects of higher interest rates and economic volatility.

Yet amid the continued contraction, one statistic stood out: inquiries into new projects rose for the third straight month in April.

That distinction matters.

Inquiries often function as the earliest stage of the design and construction pipeline—surfacing long before contracts are signed or financing is secured. Even if projects are not yet moving forward, the increase suggests that clients may be beginning to cautiously reengage after months of paralysis.

The value of new design contracts also remained close to returning to growth, another indicator that the market may be inching toward stabilization.

Still, economists remain cautious about what comes next.

“April’s economic picture was mixed as employers continued to add jobs, but inflation accelerated as higher energy prices tied to the conflict in Iran drove up costs,” said AIA Chief Economist Richard Branch, AIA. “While a proposed gas tax holiday could offer some short-term relief, energy prices are unlikely to ease meaningfully until the conflict ends.”

Branch’s comments highlight how deeply architecture and construction are now entangled with global economic forces far beyond the profession itself. Rising fuel prices affect everything from material transportation and manufacturing to labor costs and construction logistics. In an industry already grappling with tight margins and financing uncertainty, even modest cost increases can cause projects to stall.

Key ABI highlights for April include:

- Regional averages: West (49.0); Midwest (48.0); South (47.7); Northeast (47.2)

- Sector index breakdown: multifamily residential (51.5); institutional (51.1); commercial/industrial (48.9); mixed practice (firms that do not have at least half of their billings in any one other category) (42.5)

- Project inquiries index: 57.7

- Design contracts index: 48.0

The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

The prolonged downturn also reflects a larger recalibration happening across the real estate and development sectors. During the post-pandemic boom, low interest rates and intense demand fueled aggressive building activity across housing, commercial development, logistics infrastructure, and mixed-use projects. That environment has changed dramatically.

Developers are reevaluating risk. Institutional clients are delaying commitments. Office construction remains constrained by evolving workplace patterns. Financing has become more expensive and harder to secure.

And yet, long-term demand drivers remain firmly in place.

The United States continues to face severe housing shortages, aging infrastructure, climate adaptation pressures, healthcare expansion needs, and growing demand for data centers and advanced manufacturing facilities. Many architecture firms are therefore caught in a strange contradiction: the long-term need for design expertise remains enormous, even as short-term project pipelines continue to weaken.

For many firms, survival now depends on diversification, adaptability, and patience.

The April ABI numbers do not yet signal a recovery. But they do suggest that the industry may be moving from outright deterioration toward a more fragile and uneven stabilization phase.

After more than two years of contraction, even that shift is enough to command attention.

For now, architecture firms remain suspended between caution and cautious optimism—waiting to see whether rising inquiries can eventually evolve into signed contracts, active projects, and a broader return to growth.