A Brick Wall, Quite Literally

Montreal is a city built in brick and defined by stone. A clause in many of its municipal design guidelines effectively steers new street-facing facades toward masonry, which, in practice, means clay brick. It is a reasonable rule in a city whose architectural identity is inseparable from its material texture.

Monttreal Brick.

Scan Quebec, though, and you’ll find almost no brick manufacturers. Most designers working here specify brick imported from the United States.

That detail sent us back to an embodied carbon study comparing brick sourced from Nebraska, Arkansas, and Ontario. Once transport distance and regional grid intensities are taken into account, the story is uncomplicated: long supply chains often cost more, and emit more.

But after the last round of U.S. tariffs, the brick question is no longer just about cost or carbon accounting. It’s about exposure. When a core input is routinely imported to meet a local design expectation, border policy becomes a project risk—one capable of disrupting schedules, bids, and substitutions with little warning. In Canada, that uncertainty now extends beyond any single material category. It sits across the assemblies that make housing possible.

What U.S. Tariffs Reveal About Canadian Housing

From an American vantage point, Canada is often seen as an extension of the U.S. market: aligned standards, integrated supply chains, and trade agreements designed to reduce friction. The post-tariff reality is more complicated.

In 2025, the United States raised tariffs on steel and aluminum imports, starting at 25% in March and climbing to 50% by June, including materials coming from Canada. Duties on softwood lumber also continued to increase.

These pressures are building alongside a broader source of uncertainty: a scheduled review of the USMCA trade agreement in July 2026. For U.S. architects and developers, this can read like “Canada’s problem.”

For Canadians, it has become a stress test of how housing delivery now depends on supply chains that are simultaneously carbon-intensive and politically fragile. The lesson is transferable: when trade pressure rises, the material assumptions embedded in standard assemblies become visible, and visible fast.

The Hidden Layer of Housing Affordability

Canada’s housing affordability crisis is typically framed around land prices, zoning, financing, and labour. But there is another constraint that sits behind both cost and carbon: the supply chains feeding our building components.

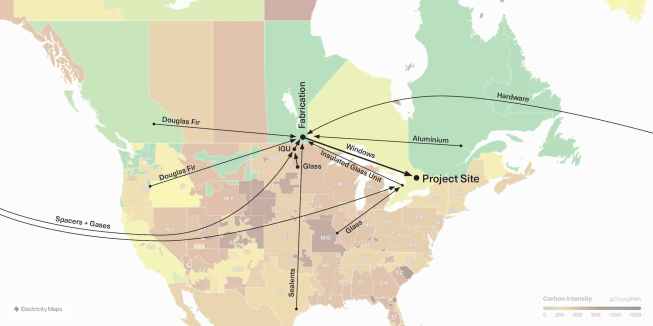

Every assembly carries a lineage. Windows depend on float glass plants, timber, extrusions, and specialized hardware. Insulation depends on petrochemical processing or mineral extraction. Mechanical systems rely on global networks of compressors, electronics, and controls. When those networks are stable, they’re invisible. When tariffs, trade disputes, or geopolitics disrupt them, the impacts become immediate, and unavoidable.

A recent assessment of materials commonly used in low-rise multi-unit housing found that many core building components are highly exposed to tariff and supply chain disruption — vulnerable to price spikes, sourcing delays, and forced substitutions.

That same assessment found many of these components land in medium-to-high exposure categories when evaluated through an international trade lens. The most exposed families included windows, membranes, rigid insulation, and HVAC systems; all products central to performance, durability, cost, and carbon.

This is where North American integration becomes a partial story. Many products assembled in Canada rely on imported subcomponents. A window fabricated in Ontario may include U.S. glass, European hardware, and spacers manufactured in Asia. A heat pump specified for electrification may depend on a compressor sourced abroad.

Even where final assembly is domestic, vulnerabilities often sit one or two tiers upstream. Housing affordability and embodied carbon are shaped by the same material decisions. Risks are embedded long before a building opens its doors.

Assemblies Under Pressure

To understand how exposure becomes project risk, it helps to look at assemblies, not categories.

Windows and glazing are an obvious example. Float glass manufacturing is geographically concentrated, and modern glazing integrates coatings, spacers, sealants, and hardware that often come from different countries.

When a tariff or border disruption hits, it doesn’t arrive as an abstract headline. It arrives as a bid revision, a lead-time extension, or an “approved alternate” request that shifts the entire envelope package.

Membranes and rigid insulation often carry a different vulnerability: petrochemical dependence. Many are tied to global commodity pricing and energy volatility. In a cost shock, substitutions are common, and in the rush to protect first costs, the risk isn’t just “slightly different performance.” It can mean a shorter service life, higher moisture exposure, earlier replacement, and more waste; a durability issue that quickly becomes a whole-life carbon problem.

HVAC sits at the center of the operational-to-embodied handoff. Electrification strategies depend on heat pumps, controls, and electronics that are often imported. When supply tightens, teams are asked to swap equipment, revise layouts, or compromise on performance. The operational carbon story shifts. The embodied carbon story shifts. The maintenance story shifts.

The deeper problem is that switching course mid-project is rarely simple. The product is already specified, the lead time already committed, the envelope or mechanical layout already designed around it.

Supply Chain Flows.

Call it supply chain lock-in: the vulnerability isn’t a line item in a budget. It’s woven into the assembly itself, invisible until the border moves. For architects on either side of that border, tariff volatility doesn’t simply raise costs. It can distort design intent and force substitutions that change carbon outcomes, lifecycle costs, and building performance, especially when the affected products are performance-critical.

Carbon and Trade Are the Same Conversation

In recent years, built-environment climate strategy has focused on operational energy and embodied emissions. Trade volatility forces a parallel realization: the systems that drive carbon intensity often drive price instability too.

Long-distance supply chains increase transport emissions and magnify exposure to border disruption. Fossil-fuel-intensive materials are tethered to global commodity markets. Concentrated manufacturing hubs amplify geopolitical risk. When a small set of regions supplies a dominant share of a critical component, resilience stops being a procurement detail. It becomes a structural condition of housing delivery.

Breanne Belitski, an embodied carbon researcher with Builders for Climate Action, puts it bluntly: “industrial policy and decarbonization cannot be separated.” Rebuilding domestic capacity without addressing emissions undermines climate goals.

Pursuing climate targets without strengthening local production leaves the construction sector exposed. For Belitski, instability is also a signal. Vulnerabilities point to where opportunity lies, often in what could be produced locally but is currently imported.

Trade pressure forces a closer look at what is produced locally, what is imported, and how those choices intersect with carbon and cost. The issue is not trade itself. It is the misalignment between decarbonization targets and the systems that supply our buildings. Closing that gap means rebuilding domestic production capacity around lower-carbon materials, not as industrial policy but as a climate strategy.

Design as Risk Management

That misalignment lands, inevitably, at the drawing board. It lives in the specifications we write. Specifications embed assumptions about global stability. When building assemblies rely on fossil fuel intensive supply chains that are concentrated in a small number of global producers, volatility is built into housing delivery. When regionally sourced and lower-carbon materials are prioritized exposure can drop,sometimes dramatically.

Canada’s experience is a preview of what happens when you treat availability as a constant. In both countries, housing delivery increasingly hinges on products that are performance-critical, componentized, and globally distributed. When those products are hit by tariffs, duties, or delays, the pressure is felt where it hurts most: the envelope and the mechanical system.

The Montreal masonry expectation captures the contradiction precisely. A local rule reinforces architectural continuity. Yet the absence of local manufacturing exposes a disconnect between cultural intent and industrial capacity.

When brick crosses a volatile border to satisfy a local requirement, cost and carbon are only part of the story. Supply chain resilience becomes part of design, and one concrete path forward is expanding the domestic capacity to produce it.

Growing Domestic Capacity

Canada’s forestry and agricultural sectors offer a direct path to strengthen manufacturing while reducing embodied carbon. Wood fibre insulation, straw-based panels, and other plant-derived products can build on existing resource bases.

Belitski highlights wood fibreboard as a compelling example: residual biomass and offcuts can be converted into insulation that displaces petrochemical foams, reducing both emissions and import exposure.

Agricultural fibres offer similar potential. The transportation networks built to move crops already connect farms, rail lines, and regional markets. Leveraging that infrastructure for building products reduces logistical barriers and strengthens regional economies.

The obstacles are familiar on both sides of the border: certification costs, variable code interpretation, liability concerns, and a conservative market that treats “unfamiliar” as “risky.” These aren’t technical problems,they are policy failures dressed up as market realities. Trade pressures change the calculus. When insulation and facade systems become vulnerable, domestic alternatives don’t just gain strategic value, they become the more defensible specification.

Several shifts could accelerate this without a wholesale redesign of the construction sector. Harmonizing approvals across provinces is the obvious starting point: Canada’s fragmented landscape means every province functions like its own import market, keeping domestic manufacturers too small to compete.

Public procurement needs to do more heavy lifting;ousing agencies and public clients should be requiring EPDs, setting performance outcomes, and creating pathways for bio-based materials to compete on a level footing. Investment in regional manufacturing and material recovery hubs, anchored in regions with forestry and agricultural strength, should be treated as supply chain infrastructure, not economic development afterthought.

And a shift toward performance-based standards would reward materials that meet durability, fire safety, and moisture outcomes while reducing carbon and trade exposure, rather than locking markets into prescriptive lists built around yesterday’s supply chains.

These are not dramatic moves. They are the structural kind, the ones that make the next decade of housing delivery more predictable, and the next tariff shock less disruptive.

What We Specify

The brick facade in Montreal is a reasonable rule producing an unreasonable dependency. It is also an accurate image of where the profession now stands: absorbing the risk of trade relationships that are being renegotiated in real time, through materials specified years before the borders moved.

Housing affordability, embodied carbon, and trade resilience are not separate challenges. They converge in the same column of a specification sheet. The tariff escalations, the lumber duties, the compounding uncertainty around continental trade: these are not external shocks to the construction sector.

They are the construction sector’s problem, because its supply chains made them so. Every assembly that depends on a globally consolidated, fossil-intensive supply chain is a bet that the world will stay still. It hasn’t.

Reducing that exposure doesn’t require reinventing practice. It requires treating the specification sheet as what it actually is: a bet on how the world is organized, and a lever for changing it.

The fragility is designed in. So is the way out.