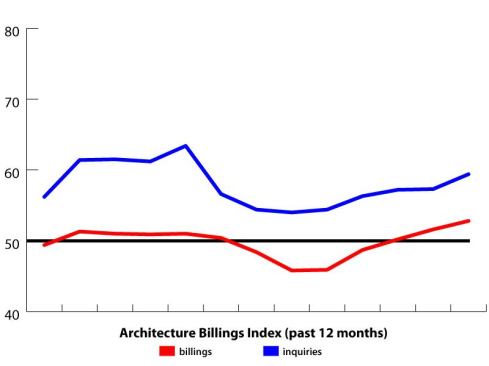

For the third straight month, the American Institute of Architects’ Architecture Billings Index is in positive territory. October’s score came in at 52.8, up from last month’s 51.6. (Any score above 50.0 means growth in billings.) The score for project inquiries also rose to 59.4 from September’s 57.3. As with last month, the market for architectural services is looking hopeful again, and there’s also, thankfully, no sign yet that anxiety from the possibility of the federal government not reaching a resolution to the fiscal cliff is having a deleterious effect.

Except for the Commercial/Industrial sector, all of the nation’s regions and the industry’s sectors are also growing—a first in almost a year. Some of the individual regions and sectors are also experiencing levels of growth not seen since before the construction bubble popped and the financial crisis decimated the economy.

National highlights:

National: 52.8 is the highest national score since December 2010 (52.9), and the second highest score since December 2007 (also 52.9).

Inquiries: 59.4 is the highest score for project inquiries since February, and this is the 45th straight month that project inquiries has been in positive territory.

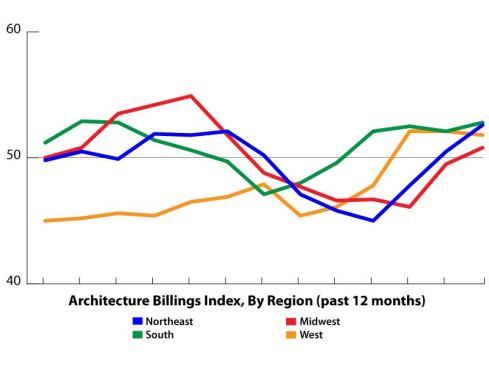

Region highlights:

Northeast: 52.6 is the highest score since October 2010 (52.8).

Midwest: 50.8 is the first time this sector has been over 50.0 since March (51.8).

South: 52.8 is the highest score since December 2011 (52.8).

West: 51.8 is down from the past two months, but the sector is still slowly growing.

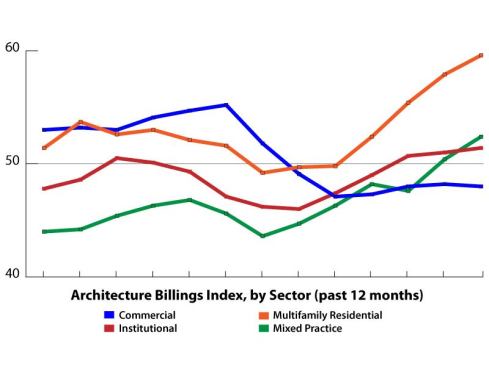

Sector highlights:

Multifamily Residential: 59.6 is the highest score for this sector since April 2005, and the second highest score since October 2004.

Commercial: At 48.0, this is the only sector still contracting.

Institutional: 51.4 is the highest score for this sector since July 2008, which was the last month that this sector was consistently growing.

Mixed Practice: 52.4 is the highest score since December 2007, which was the last month that this sector was consistently growing.

Even more than just the numbers, the consistency over the past few months is a hopeful sign. Except for the Midwest region and the Commercial sector, all of the national, regional, and sector scores have shown growth for multiple consecutive months. Multifamily Residential continues to roar ahead, and while that sector has been the most consistently stable sector over the past four years, it is a surprise to see Mixed Practice—a sector that has had a very rough five years—consistently growing.

Combine this with the increase in residential construction, and maybe we really are seeing the industry turning the corner. But there is also a chance that we are seeing a trend that has repeated the last few years: Billings increase from fall through spring, only to see another lull come the beginning of summer.