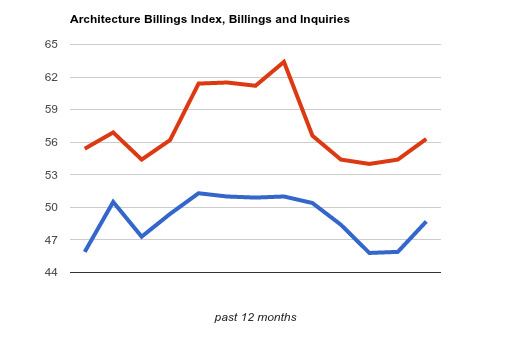

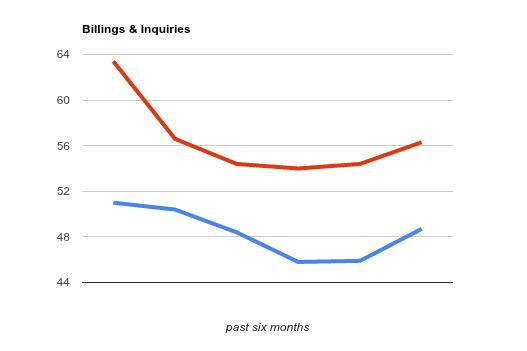

For the month of July, for the fourth month in a row, the American Institute of Architects’ monthly Architecture Billings has shown signs of contraction and weakness in the market for design and construction services. This month, however, the rate of contraction has slowed considerably. At 48.7, the score for July was better than the 45.9 recorded for the month of June, which was a slight moderation in decline from the 45.8 recorded in May (50.0 is the break-even point between contraction and growth). The score for new projects inquiries was up to 56.3 from June’s score of 54.4.

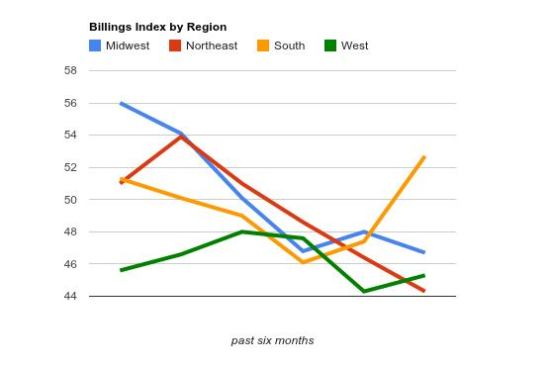

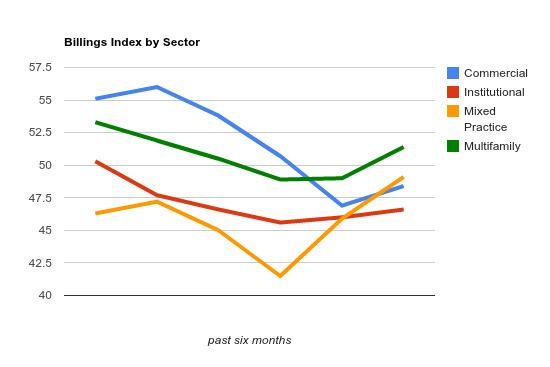

In addition, one of the industry’s sectors, multifamily residential, and one of the nation’s regions, the South, each showed growth in July—coming in at 51.4 and 52.7, respectively. In June, all four of the nation’s regions and all four of the industry’s sectors showed contraction in billings. (The regional and sector categories are also calculated on a three-month moving average, unlike the national score, which is month-to-month.)

But as you can see in the charts in the slide show above, all of the industry’s sectors and half of the nation’s regions showed improvement in July. Billings in the South grew, and the speed of contraction of billings in the West moderated. Multifamily residential billings grew, while the rate of contraction for commercial, institutional, and even mixed practice (which has taken an especially big hit over the past few years) saw their rates of contraction slow. Could we see more growth in the coming months for all of these sectors and regions? Possibly.

If billings do recover and begin growing again this fall, we’ll see a repeat of the trend that we’ve seen the past three years, a cycle that seems to be becoming regular in the wake of the financial crisis of 2008. I don’t know what the reason is—since it seems counterintuitive that the design and construction industries would pick up heading into winter, and then trail off come summertime—but the cycle of weakening billings during the warmer months has repeated itself once again, as you can see in the charts below:

")

")

")

")

Billings in 2009 and 2010 were still contracting, but ever more slowly as a general trend, returning to an expanding market at the end of 2010. The summer months brought a setback to recovery in each of those years. Billings were growing in the spring of 2011 and 2012, only to see a renewed contraction in billings come late spring. Last year, billings were growing again come fall, and if the trend continues, this fall there will be more work to be had as well.