One thing everyone knows is that our current economic woes are driven by a precipitous decline in the construction industry, itself a hangover of the enormous boom in construction of the aughts. As the economist Jeffrey Sachs has written, “As the U.S. shed manufacturing jobs in the 1980s and 1990s, the Federal Government and Federal Reserve tried to compensate by boosting jobs in construction and other sectors shielded from international competition.” Hence the low interest rates of the Bush years, which drove mortgage lending to new heights and spurred the unprecedented growth in home building that we’re now saddled with.

It’s a familiar story, but in important respects it’s mistaken.

For starters, we should distinguish between a boom in housing construction and a boom in house prices. The purchase of a conventional house combines two things. On the one hand, you have the physical object. On the other hand, you have the land that it sits on. In the niche market for mobile homes, the distinction is clear. You buy the home from one person, and you rent or buy the land to park it on from someone else. People who buy normal houses are making two different transactions simultaneously. But the prices of the two different commodities have different implications for construction and job growth. If demand for mobile homes skyrockets, prices will go up. Since prices go up, the profits in the mobile-home-manufacturing sector also rise, and capital flows to mobile-home makers, which means that they can expand production.

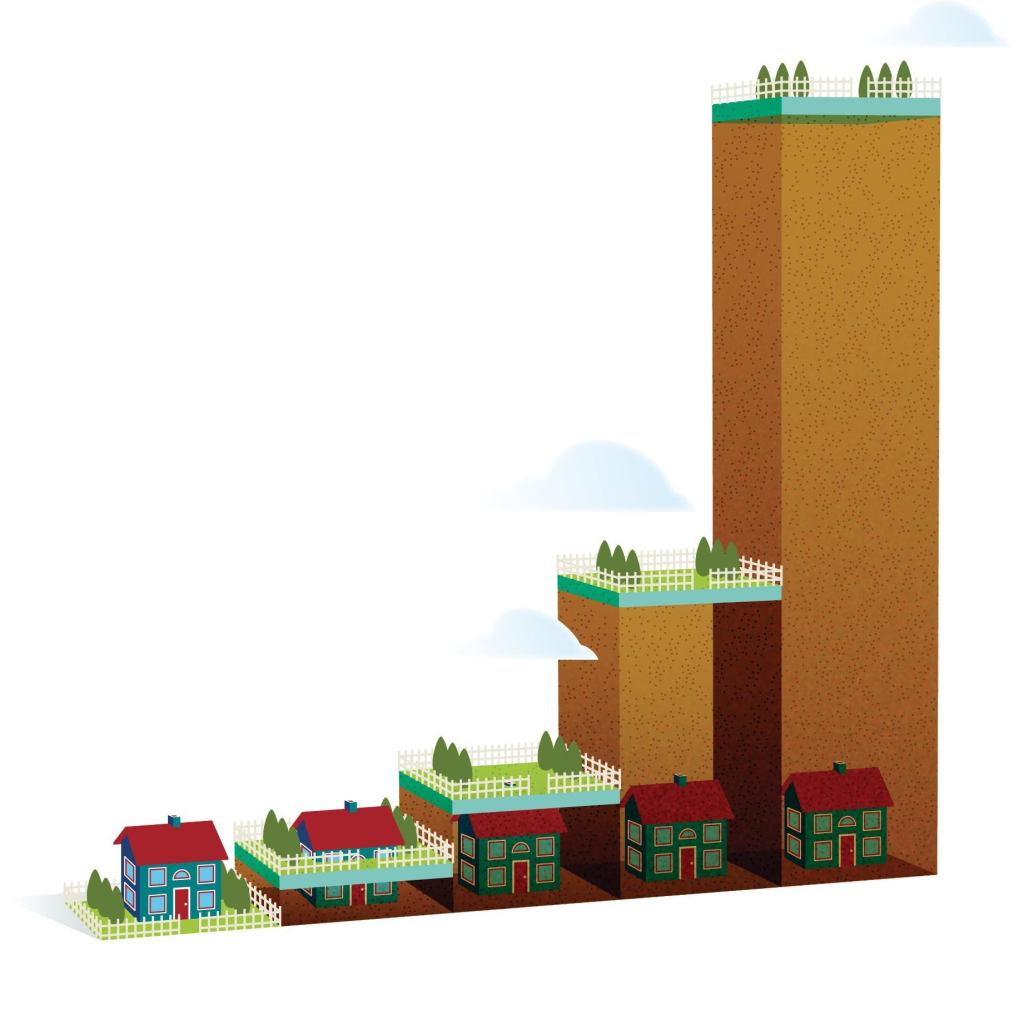

WHAT HOUSE-SIZE BOOM?

The increasing size (in square footage) of single-family homes doesn’t explain the mid-’00s boom in home prices, as homes have been growing larger as far back as size records go.

1975: 1,535

1980: 1,595

1985: 1,605

1990: 1,905

1995: 1,920

2000: 2,057

2005: 2,227

2010:2,169

Source: U.S. Census

But if everybody decides to drive their mobile homes to Southern California to take advantage of the delightful weather, all that happens is the price of land goes up. We’re not going to build more California. Existing landowners simply charge higher rents, or sell the property they already own.

The housing boom, like the housing market itself, had aspects of both a speculative boom in land prices and a boom in house construction. The data show, however, that there was nothing particularly unprecedented about the home-building boom. The really unusual thing is the current massive construction bust.

The federal government keeps data on new housing starts that goes back to 1959. It shows that over the past 50 or so years, the United States has on average added 1.5 million new homes per year. From 1998 through 2006, we managed an impressive nine-year run of above-average home construction. For the majority of those years, however, home building was fairly restrained. It also followed 10 straight years of below-average new starts, meaning that we were largely meeting pent-up demand for new homes. The 2003–2006 period was a bit crazy, with 1.85, 1.95, 2.07, and 1.82 million new starts per year. Still, the total of 7.69 million new starts during this period is by no means the busiest four-year spasm of postwar building. From 1970 to 1973, there were 7.88 million new home starts. That was followed not by a depression, but by a new boom in 1976–79 of 7.22 million new starts. Compare that to the pathetic construction market of the four post-2006 years when we started fewer than 4 million new homes. That’s the worst four-year span since record-keeping began. That span includes the only three years in which fewer than 1 million new homes were started. When the 2011 data are available, this year is likely to be the fourth.

What’s more, population growth was slower in the past. Between the 1970 and 1980 censuses, the U.S. added about 23 million new people. Between the 2000 and 2010 censuses, however, it was more like 27 million.Adjusted for population growth, in other words, what’s unprecedented about the construction market of the aughts isn’t the boom—it’s the bust.

When confronted with this data, many point to ballooning home sizes as their preferred indicator of bloat. And it’s true that homes were getting bigger during this period. In 1997, the year before the launch of the housing boom, the median new single-family detached house was 1,975 square feet. By the final boom year, 2006, that was up to 2,248 square feet. But again, there’s nothing unprecedented about this. In 1987, the median new single-family home was 1,755 square feet. In 1977, it was just 1,610 square feet. In 1973—the first year for which the U.S. Census Bureau has data—it was 1,525. Bigger houses, in other words, are part of a long-term trend that has nothing in particular to do with the recent house-price boom.

Another way of seeing what’s going on here is to look at new household formation. If construction is slow primarily because of past overbuilding, you’d expect to see new household formation occurring at a normal pace as people simply move into the existing stock of houses rather than building new ones. Instead, in both 2009 and 2010 we added fewer than 400,000 new households—a low not seen since the 1940s. There was no new building because there were no new households. But the population didn’t stop growing. Instead, joblessness has kids living with their parents or struggling families doubling up to save on rent. At this point it seems overwhelmingly likely that even a small income-raising economic boost—either through the Federal Reserve and monetary policy or Congress and fiscal policy—could spark a construction rebound and put us into self-sustaining recovery territory. But convincing policymakers to do either requires first disabusing them of the notion that the current slump is some kind of cosmic payback for past maniacal overbuilding.

None of which is to deny that some overbuilding took place. It’s clear that in some specific markets—the Inland Empire of California, the suburbs of Las Vegas, and Phoenix—we really do have too much supply. But the flipside of this is the land-price boom and places where we clearly have too little. Even after the real estate bust, it’s very expensive to live in San Francisco or Manhattan or the nice suburbs and neighborhoods of Washington, D.C.

These are great places to live, and lots of people want to live there, bidding up the price of land. If zoning regulations permitted it, developers would respond to those high prices by building denser housing—smaller yards, taller buildings—to accommodate more people. But by and large they don’t. This supply restriction is what drove people to the sunbelt boomtowns in the first place. If you want to criticize the housing trends of the early aughts for something, pick that. It’s not so much that we built too many houses as that we didn’t build them in the most desirable locations. If and when incomes start rising again, household formation will resume, and we’ll need to build more homes. But unless we improve rules about where we’re allowed to build, we won’t gain nearly as much benefit as we could.

Matthew Yglesias covers economic policy and business for Slate, where he writes the Moneybox column.