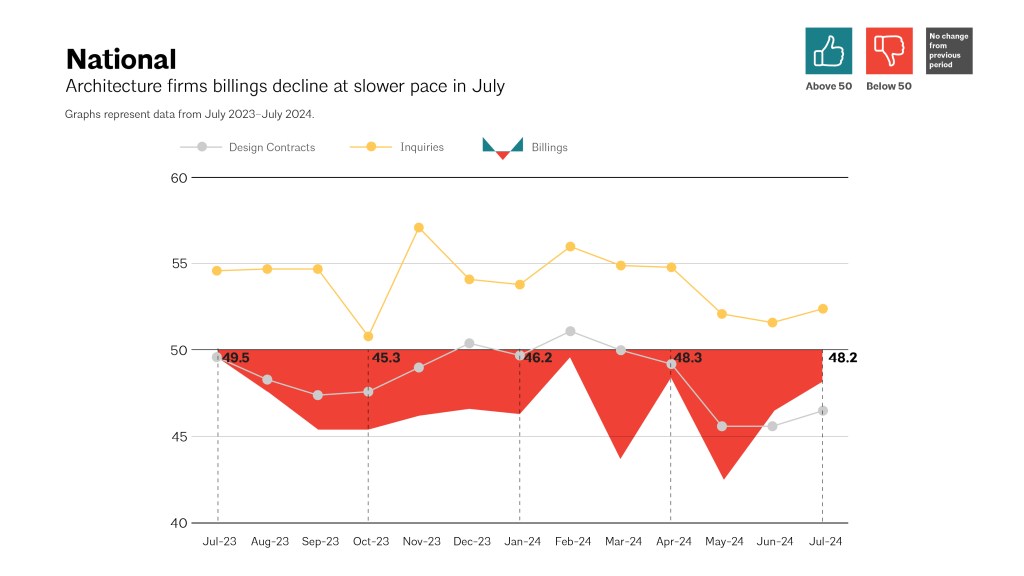

Architecture firms across the United States are grappling with ongoing financial strain, as billings continued to decline for the eighteenth consecutive month, according to the latest Architecture Billings Index (ABI) from the American Institute of Architects (AIA) and Deltek. The ABI score for July was reported at 48.2, signaling that while fewer firms reported declines in billings compared to the previous month, over half of those surveyed still face difficult business conditions.

Kermit Baker, PhD, AIA’s Chief Economist, commented on the findings, stating, “Architecture firms continue to face a billings slowdown. However, the emerging prospects of lower interest rates coupled with a modest uptick in project inquiries suggest that some dormant projects may be revived in the coming months.”

Despite the faint glimmer of hope provided by increasing project inquiries, the landscape remains tough for many firms. The report notes that newly signed design contracts have seen a decrease for the fourth consecutive month, although the rate of decline has somewhat slowed.

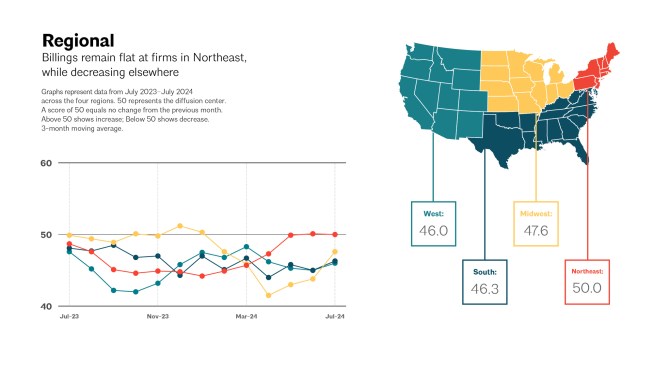

Regionally, architecture firms in the Northeast have managed to stabilize, with billings holding steady for the second month in a row. This marks the first time since mid-2022 that the region has seen scores at or above 50 for two consecutive months. However, other regions are not faring as well, with declines reported across the Midwest, South, and West, although the pace of these declines has eased.

The Architecture Billings Index, a leading economic indicator of construction activity, offers a nine-to-twelve-month forecast into the future of nonresidential construction spending. The index is based on a monthly survey of architecture firms, measuring the change in the number of services provided to clients.

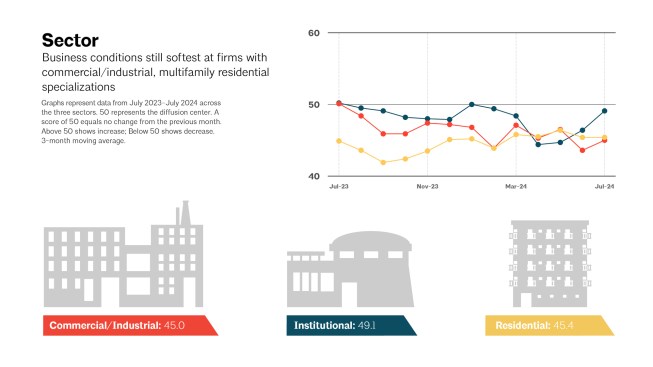

Key ABI highlights for June include regional averages such as the Northeast (50.0), Midwest (47.6), South (46.3), and West (46.0). Sector-specific indices showed commercial/industrial (45.0), institutional (49.1), mixed practice (firms that do not have at least half of their billings in any one other category) (47.7), and multifamily residential (45.4). The project inquiries index was recorded at 52.4, while the design contracts index was at 46.5.

The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

As firms navigate these challenging conditions, the AIA and Deltek continue to monitor these trends, providing crucial insights into the architecture industry’s ongoing struggles and the potential paths to recovery.

Visit AIA’s website for detailed information about this, and past billing index reports.