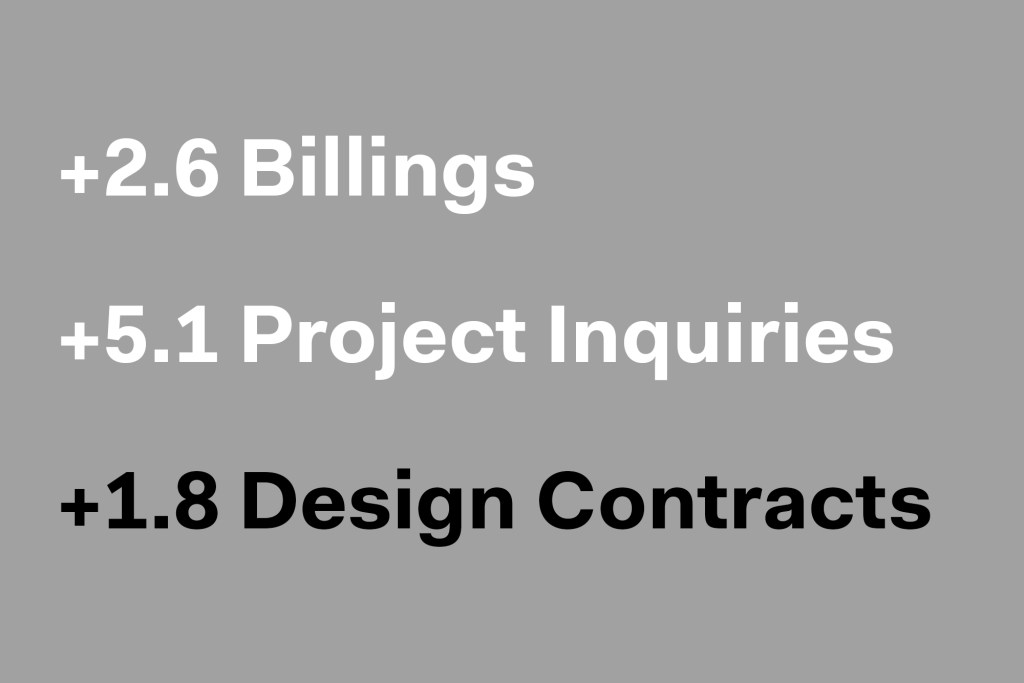

AIA’s monthly Architecture Billings Index improved slightly in January, coming in at 44.9, as compared to a revised value of 42.3 in December. The ABI is a leading economic indicator of construction activity in the U.S. and reflects a nine- to 12-month lead time between architecture billings and construction spending nationally, regionally, and by project type. A score above 50 represents an increase in billings from the previous month, while a score below 50 represents a contraction. Each January, the AIA research department updates the seasonal factors used to calculate the ABI, resulting in a revision of recent ABI values.

“The broader economy entered a soft spot during the fourth quarter of last year, and business conditions at design firms have reflected this general slowdown,” said AIA chief economist Kermit Baker, Hon. AIA, in the Institute’s press release. “While federal stimulus and the increasing pace of vaccinations may begin to accelerate progress in the coming months, the year has gotten off to a slow start, with architecture firms in all regions of the country and in all specializations reporting continued declines in project billings.” New project inquires increased 5.1 points from December’s revised score of 51.7 to 56.8, while design contracts remained in negative territory, though the score did rise 1.8 points from 47.0 to 48.8.

The month-to-month change in scores for regional billings—which, unlike the national score, are calculated as three-month moving averages—were mixed in December, with all four regions again reporting scores well below the threshold of 50. Billings in the Midwest dropped 1.4 points to a score of 42.2, while billings in the West decreased 0.6 point to a score of 42.8. Billings in the South rose 0.6 point to a score of 47.4, and billings in the Northeast also rose 3.1 points to a score of 41.9.

Billings score fell in nearly all individual industry sectors with all four sectors reporting scores below the threshold of 50.0. The commercial/industrial sector decreased 2.9 points to a score of 44.3; the institutional sector rose 1.4 points to a score of 39.9. The multifamily residential score dropped 1.7 points to a score of 44.4; the mixed practice sector fell 0.1 point to a score of 47.9. Like the regional billings scores, sector billings scores are also calculated as three-month moving averages.