This story was originally published on ARCHITECT’s sister site, Builder.

The importance of baby boomers in the housing market and wider economy cannot be overstated as they have the highest homeownership rate among all age groups, control over half of the nation’s wealth, and are the second largest living generation behind millennials.

For the purposes of article, we will address both baby boomers and the 55-plus cohort. The inclusion of the latter allows us to address those that qualify for age-restricted and age-targeted communities.

Baby boomers, those generally considered to be born between 1946 and 1964, are still working in large numbers, but Zonda estimates 12 million to 15 million of those older than 55 may leave the labor force by 2026. According to the U.S. Census Bureau, all boomers will be of retirement age by 2030. Retirement is often a catalyst for additional life changes, including relocation.

In fact, United Van Lines data found that those 55-plus represented nearly 55% of all relocators in 2022. The same data pointed to retirement as the fourth-highest motivation for a move.

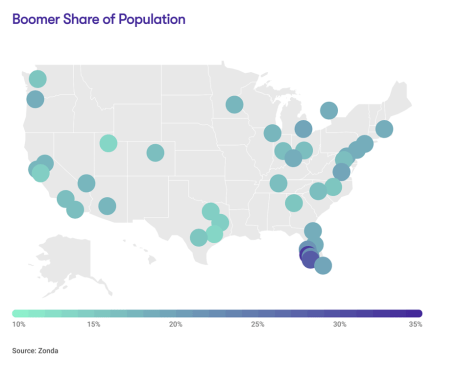

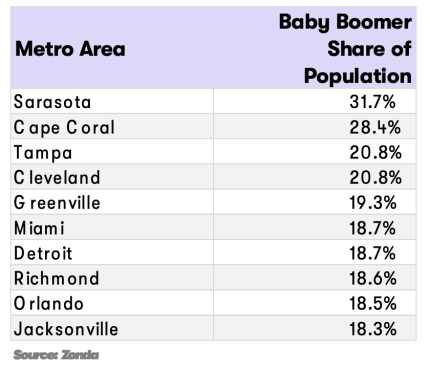

The metros with the largest number of boomers by volume are New York, Los Angeles/Orange County, Chicago, Miami, and Philadelphia. These markets are not surprising, as they are some of the most populous metropolitan areas in the United States.

Instead, if we look at boomer share as a percentage of total population, we find that Florida is home to six of the top 10 metros.

“It is no surprise that Florida has been a prime destination for boomers for years,” explained Kristine Smale, Zonda Advisory senior vice president and Southeast expert. “What has changed, though, is the increase of pre-retirees flocking to the state. Pre-retirees are those who had plans to move to Florida for retirement, but work-from-home options enabled them to do it sooner to take advantage of tax and lifestyle benefits.”

A map with the national view and a table of the top 10 metros can be found below.

Atlanta; Austin and Dallas in Texas; Raleigh, N.C.; and Jacksonville, Fla. have experienced the most 55-plus population growth compared with 2010. The attraction to these markets varies but is driven, in part, by more attainable housing than coastal cities, desirable weather, and proximity to family. For example, all five markets also land on Zonda’s Baby Chaser Index, an index that tracks where boomers are moving to most to get closer to their grandchildren.

When thinking about boomers in the context of the wider housing market, the cohort recently retook the lead from millennials in terms of number of homes purchased. Boomers made up nearly 40% of total transactions in 2022.

As we think about where housing demand goes from here, there are three top considerations related to boomers: wealth, generational transfer of wealth, and relative mobility.

Boomers Hold (Slight) Majority of U.S. Wealth.

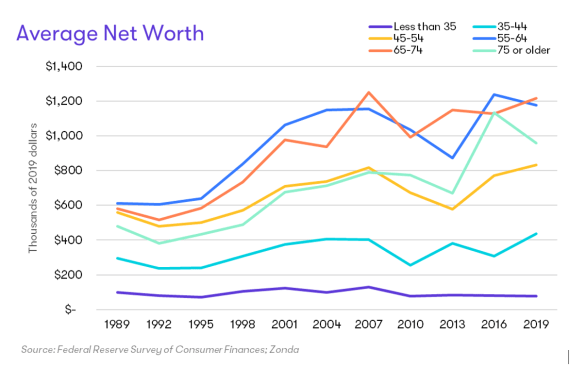

A recent Federal Reserve study showed that those age 55 and older in the United States have seen strong growth in their real wealth over the past 30 years. The average net worth per household is over $1 million for those 55 to 74, the highest of any age group today (see graph below). The growth in wealth can be attributed to many things, including decades-long economic expansion, rising stock prices, and home price appreciation.

Based on Zonda’s estimates, baby boomers control about 51% of the nation’s wealth despite being roughly 24% of the population. (Note: Federal Reserve data from 2022 Q4 showed that the 55-69 age group controlled 46% of the nation’s wealth, a similar figure to what Zonda calculated.)

Boomers also have the most assets. Federal Reserve data finds that total assets for boomers are allocated as follows: real estate, 24%; corporate stocks and mutual funds, 23%; other assets, 22%; retirement funds, 21%; and private business equity,10%.

The wealth discussion becomes important in today’s affordability-challenged housing market. Many boomers are less sensitive to fluctuations in home prices and mortgage rates given their stronger financial position than other generations. This has helped contribute to the share gain of boomers of total housing transactions as we previously discussed. Although not all boomers are flush with cash—a recent study by Credit Karma found that almost one in five people age 59 and older said they don’t have a retirement account.

Generational Transfer of Wealth

As boomers age, there’s a question about what will happen to the accumulated wealth. A 2019 Merrill Lynch Wealth Management poll that asked about distribution of wealth to heirs found that 65% of those 55-plus plan to give away some of their money while they are still living, 27% plan to disperse their money after they die, and 8% plan to give it all away while alive.

Per The Wall Street Journal, Cerulli Associates estimates that older generations will give away $70 trillion between 2018 and 2042, with roughly $61 trillion going to heirs and the remainder going to philanthropy.

These stats become important when thinking about the younger generations that are dealing with today’s housing affordability crunch. Some younger individuals have already benefited from “the Bank of Mom and Dad,” a phrase that describes parents helping their children with a down payment on a home, assistance in getting a loan, or funds to help service monthly mortgage payments, while others are going at it alone.

We know affordability is the key barrier to homeownership. Tracking this generational transfer of wealth could have profound implications for housing demand of the younger generations for years to come.

Mobility Meets Contentedness

As mentioned earlier, those who are 55-plus have the highest homeownership rate of any age group. According to the Census Bureau’s latest data, the homeownership rate for those age 55 to 64 is 75.1%, and for those 65 and older the rate is 79.1%. Compare this with those younger than 35 with a 39% homeownership rate and an overall national homeownership rate of 65.8%.

The higher homeownership rate links back to the growth in wealth discussion as CoreLogic data estimates that homeowners with mortgages have experienced a 7.3% year-over-year increase in total equity, as of Q4 2022, following prior years of equity building as well.

Beyond benefiting from equity gains, some homeowners are no longer paying monthly mortgage payments at all. As of the latest Census data, 42% of homes in the U.S. were owned free and clear (no mortgage). Of those mortgage-free homeowners, 78% were 55 and older. This is important as shelter is typically the largest share of a household’s monthly budget. The lack of a mortgage payment removes the burden of shelter costs from these individuals.

If we layer in increased retirements with high equity and the existence of many mortgage-free households, those 55-plus homeowners are more mobile than most.

A key question for the home building industry, however, is how do we encourage a move? Because, while mobility is possible, 86% of boomers report wanting to age in place. This may be for many reasons, including an unwillingness to reset property taxes (depending on where they live) or mortgage rates (if they have one); sell and buy in today’s high price market; or leave friends, doctors, or other social networks in their area.

Researching specific boomer wants and needs can help encourage more housing turnover. However, demographics alone will contribute to more changes in boomer-owned homes as the cohort ages, including a notable uptick in resale inventory over time.

Boomers clearly play an important role in today’s housing market and will for years to come. Certain areas, such as Florida, remain a magnet for baby boomers, while many are perfectly content living in their current market in their existing home. As they continue to transition out of work, it will be worthwhile to keep tracking changes in lifestyle, wealth, and mobility.

This story was originally published on ARCHITECT’s sister site, Builder.