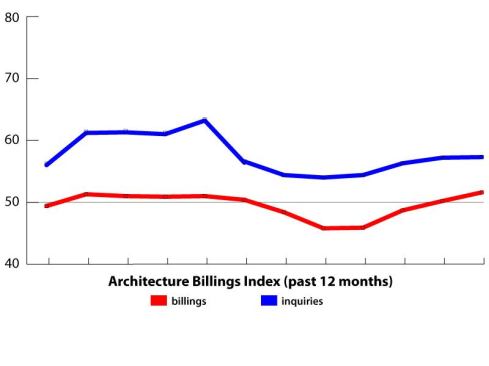

In August, for the first time in five months, the American Institute of Architects’ Architecture Billings Index (ABI) re-entered growth territory (with a score of 50.2). Then last month, that growth sped up.

For September, the ABI was released with a billings score of 51.6, which is the fastest rate of growth for architecture and design services since December 2010’s 52.9. Inquiries also inched up, to 57.3 from August’s 57.2, and that score is the highest since February of this year (which saw a score of 63.4). Looking back over 2012, the billings index appears to be mapping the same trend that we’ve been seeing over the past three years: A growth in billings in the fall, winter, and into the spring, followed by a pullback in billings and work heading into and through the summer. We will be watching this over the next six months or so to see if the pattern repeats again in 2013, or if the design and construction market can break out of this newly regular cycle of transmigration and remain in positive territory without a summer lull.

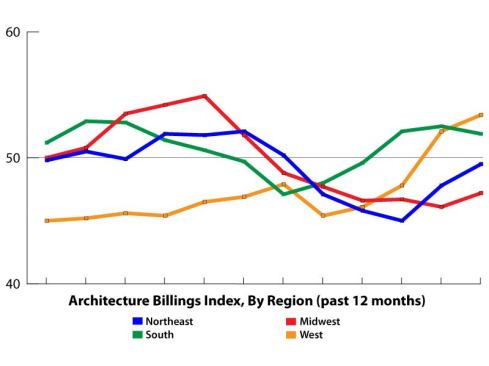

Other trends we saw in August continue. The South and West regions are still growing, while the Northeast and Midwest are still contracting; the West is growing even more quickly this month, while the South region has cooled off a little. The Northeast and Midwest, however, have seen their rate of contraction decrease substantially, so the hope is there that all four regions may grow in the future.

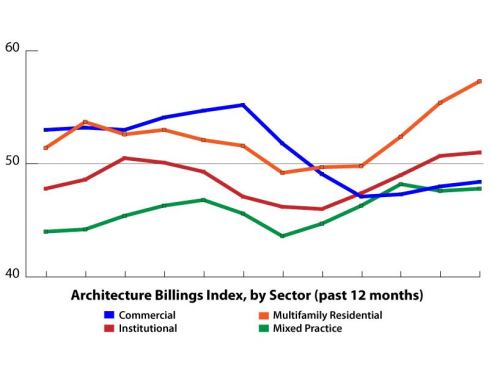

The Institutional sector’s score of 51.0 is that segment’s highest score since June 2008, before the financial crash that happened later that year, and the devastation that the crisis subsequently wrought on state and local budgets. Commercial and Mixed Practice each edged up a little, their rate of contraction continuing to ameliorate while they slowly make their way to a breakeven score of 50.

The real hero for the month of September is the Multifamily Residential sector, one of the few shining lights throughout this otherwise bleak depression, which is picking up even more steam. The sector’s score of 57.3 is the highest it has been since December 2005 and the halcyon days of the housing bubble. The Census Bureau’s report on the housing market this week affirms the ABI’s surge in Multifamily work, with starts on those projects increasing by an astounding 25 percent in September.

The market looks hopeful. If the upward trend can continue and can avoid being stymied by next summer, or by Congress not being able to reach a deal to avoid the effects of the oncoming fiscal cliff, we could, possibly, be seeing the beginning of a true recovery.

Regional Averages

West: 53.4

South: 51.9

Northeast: 49.5

Midwest: 47.2

Sector Index Breakdown

Multifamily Residential: 57.3

Institutional: 51.0

Commercial/Industrial: 48.4

Mixed Practice: 47.8

Note: Unlike the national score, the regional and sector categories are calculated as a three-month moving average.