This story was originally published in Builder.

It took 10 years, almost on the dot—from start to finish—to complete American residential real estate’s “lost decade.”

Now, the moment has come. The data is in. The line has been crossed. It’s official.

Housing, as it encompasses the number of American households earning median incomes that can afford to buy a median-priced home in his or her market, is unaffordable. Too many bidders on too few properties, and now interest rates are going up, endangering one of the past eight year’s sacred cows of recovery: the monthly payment.

The economy is revving up. Unemployment is at record lows, job markets are tight almost everywhere, corporate profitability has been solid, and business fundamentals, aided by new pro corporate investment tax incentives, could hardly be on a more solid footing.

The two glaringly conspicuous non-starters amid years of economic and business recovery momentum are living wages and normalized new residential construction activity.

Underpinning painfully slow earnings growth, it seems companies collectively tolerate lower productivity growth as they try to pivot from paying human talent to investing in non-human, automated, machine-learning driven business and manufacturing productivity solutions. Corporations are hedging their bets, fighting off having to pay people more as they invest ever more heavily in technologies, automation, and data that one day soon, might save them from having to deploy those pay raises.

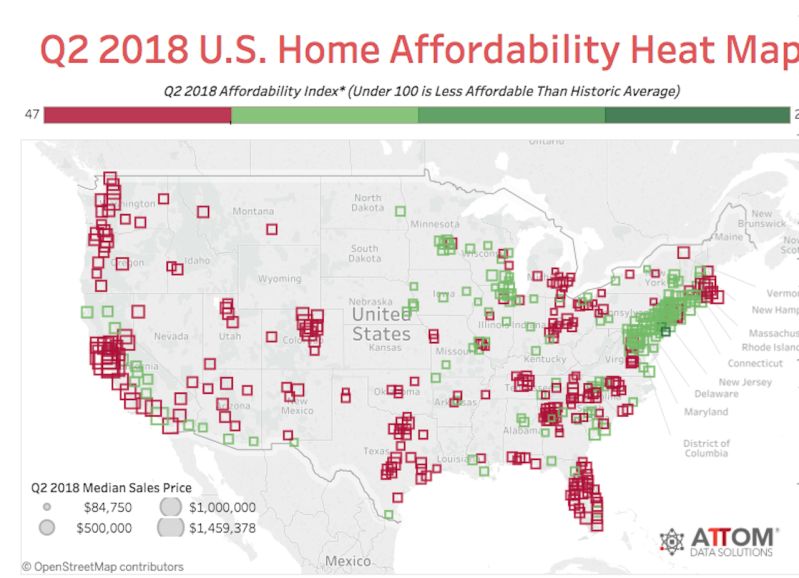

At the same time, construction starts, permits, and completions activity has risen from the dark pits of oblivion in 2010 to what would be regarded as recession-level production in any prior housing cycle context. ATTOM Data Solutions senior vice president Daren Blomquist writes:

Nationwide the median home price of $245,000 in Q2 2018 was up 4.7 percent from a year, down from 7.4 percent appreciation in the first quarter but still above the average weekly wage growth of 3.3 percent. Since bottoming out in Q1 2012, median home prices nationwide have increased 75 percent while average weekly wages have increased 13 percent during the same period.

Annual growth in median home prices outpaced average wage growth in 275 of the 432 counties analyzed in the report (64 percent), including Los Angeles County, Calif.; Maricopa County (Phoenix), Ariz.; San Diego County, Calif.; Orange County, Calif.; and Miami-Dade County, Fla.

This is an important moment for private sector players in residential development, investors, developers, builders, and their manufacturing and distribution partners. It matters as a business moment of truth—one that will separate winners from losers among home builders and the entire spectrum of stakeholders in new residential development—intimately connected with an economic inflection point, but ultimately tied to a societal axiom about the means by which individuals and families can move up in the world.

For eight years running, a key lever for these stakeholders has been one of the most underrated marketing tools of the post-2010 recovery: the monthly payment.

For that part of the population that could get access to housing finance to buy a home, the monthly payment was a powerful means to use dirt cheap money to expand both the price range of the home and the perceived value the home buyer would attach to his or her purchase.

This was a win win, but only for those who were able to participate in a highly restrictive housing finance qualifications “credit box.”

What the current recovery has yet to prove—which past housing recoveries tended to do—is to inspire, motivate, and enable would-be home buyers to work, to save, to fix their credit, and, eventually pass across the dividing line from aspiration to reality. To, literally, get out of the box and make it more inclusive. A true-up to the American Dream that proposed that hard work, and patience, and prudence, and community-mindedness should and could yield real-world benefits.

Recoveries, in other words, are not exclusively about permits, starts, and completions, the unit measures of housing activity. Recoveries past gave “have-nots” the time, the tools, and the sense of realistic hope to climb a wrung or two on the ladder of mobility toward becoming a “have.”

This housing recovery has busied itself and profited and, understandably, focused on investing, designing, developing, building, and marketing so that “haves” could have more. Monthly payments nested extras, upgrades, smart features, amenities, square footage, and gated enclaves for protection, exclusivity, and stature.

But now, at the moment monthly payment calculus seemed on the verge of pushing the bounds, to include those who believe with good reason that they’re excluded, and to inspire more people to work, save, and make the passage across the divide from “have not” to “have a shot,” monthly payments are under increasing stress, in more and more of the nation’s job-centric metro areas, where economies are thriving, but housing growth is not.

As Brookings Metropolitan Policy Program analysts Cecile Murray and Jenny Schuetz note, the issue—from a policy perspective—is not a national one, but rather a local matter:

Local governments broke their own housing markets, and they will have to fix them. Evidence suggests that in many of the Northeastern and Western communities where price-income ratios are highest, those high housing prices result from excessive land use regulation—that is, from policy choices of local governments. Making housing more affordable to middle-income families requires those same governments to revise their zoning and allow more housing to be built, especially near jobs and transportation. States can encourage better local regulation through carrots and sticks, if they figure out the politics. At the federal level, HUD could more effectively use its bully pulpit to call out communities that obstruct new housing, and share information on how to build housing more cheaply.

This report from Core Logic analyst Andrew LePage is entitled “Typical Mortgage Payment U.S. Homebuyers Commit to Outpacing Prices”:

While the U.S. median sale price has risen by just under 7 percent over the past year the principal-and-interest mortgage payment on that median-priced home has increased nearly 10 percent. Moreover, the CoreLogic Home Price Index Forecast suggests U.S. home prices will be up 5.8 percent year-over-year in March 2019, while some mortgage rate forecasts suggest the mortgage payments homebuyers face will rise twice that much.

That doesn’t bode well for getting out of housing’s participation “box,” which is locked. What’s more, the outlook on affordability is worse, not better. Zillow research notes:

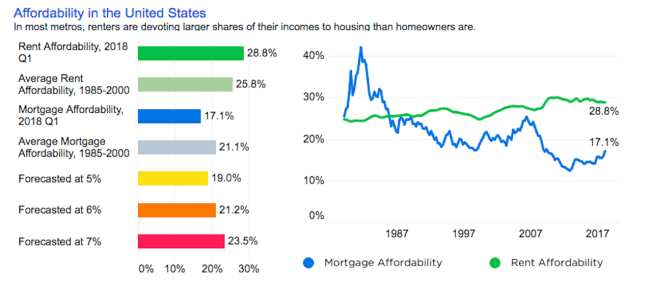

Throughout the recovery, low mortgage interest rates have helped keep homes relatively affordable, even as home values climbed to new peaks. Home values are still soaring—in April, they rose at their fastest rate in 12 years—but mortgage rates are no longer a salve. Rates have gained more than 50 basis points since the start of the year. The change in the first quarter represented the second-largest increase in the share of income home buyers should expect to spend on a mortgage since the housing market collapsed. The largest change was in the fourth quarter 2016, when the share of income needed for mortgage payments moved to 15.6 percent, from 14.1 percent the previous quarter.

Mortgage rates and housing costs represent one side of the affordability coin; income is the other. And while home values have recovered nationally, wages have been slower to bounce back. The price-to-income ratio has stayed the same or increased each quarter since early 2012, a sign of home price increases outpacing income growth. In the most recent quarter, the median U.S. home was worth 3.54 times the typical household income—considerably higher than the 2.78 average between 1985 and 2000. The last time the price-to-income ratio was this high was in the second quarter 2008, when it was 3.63, on its way down from housing-boom highs.

So, is this a business issue, an economic issue, a policy issue, or a social issue?

Your answer to the question matters. A monthly payment, we have seen, can be a powerful antidote to a housing recession. It’s also a key to making a recovery a true and sustaining recovery.

To read more stories like thss, visit Builder.