This story was originally published in Builder.

The day after bad news is a day for leaders.

Yesterday’s news was Census Bureau data for new home sales. We’ll spare you a rehash of the details, which you can link to here, and here.

That makes today Day One in the Amazon sense of the word. It’s fourth quarter, there’s a lot of work to do, and, the good news is, more people need new homes than ever before, and it’s our jobs to figure out how to deal with that.

When a business model that typically depends for growth and sustenance on at least one of three finite resources–land, capital, or labor–being available for a song, the job has gotten tougher.

But think, too, of what it’s like for those who may have the intent to be your customer, but are coming up short when they look at their own means and the financial math of ownership.

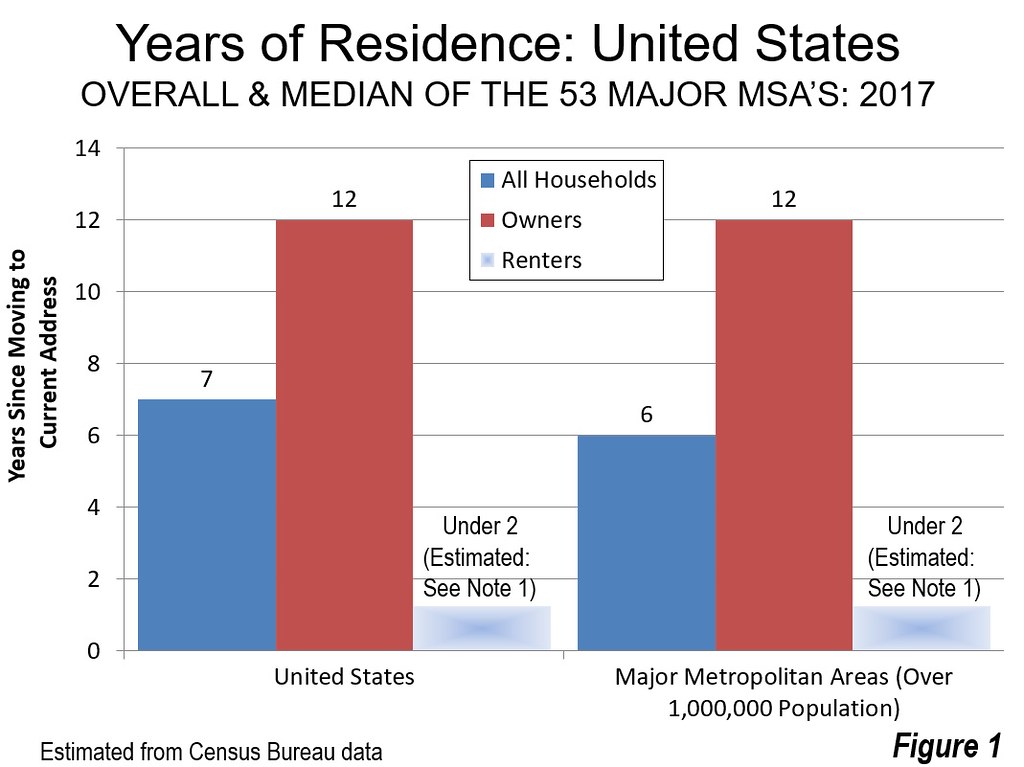

If median sale prices of homes–nationally–have come down to $320,000, let’s unpack that just a little. Average homeownership tenure–which has been increasing since the Great Recession–is now up to 12 years. How much equity could that owner build up during that time period, with monthly payments at the $2,500 mark?

For those would-be customers of yours, calculating their prospective monthly payment at a time interest rates are going up can’t be anything but painful. CoreLogic research analyst Andrew LePage writes:

While the CoreLogic Home Price Index Forecast suggests U.S. home prices will be up 4.3 percent year over year in July 2019, some mortgage rate forecasts indicate the mortgage payments homebuyers will face then will have risen by more than twice as much.

And here, Zillow economist Skylar Olsen notes that–on a national basis–current home prices mean it now takes would-be buyers longer to save for down payments than in the past. Olsen writes:

Using the national median incomes and home values of today, buyers these days need an extra year and a half, for 7.2 years total, to save a 20 percent down payment on the median valued home. Despite the booming job markets of the past decade, buyers saving down payments now – mostly first-time buyers, 61 percent of whom are millennials, according to the Zillow Group Consumer Housing Trends Report 2018 – need even more time to accomplish what previous generations did. First-time buyers say that 46 percent of their down payments come from savings, compared with 35 percent for repeat buyers, the report found.

Leaders know this much. Either the market as whole will work its way out of its three-month losing streak by the beginning of 2019, or it won’t. Cost factors won’t suddenly turn favorable for builders–and are likely only to get worse as trade and tariff measures really start working their way into the supply chain.

And then, fundamentals–the economy, job formation, wage growth, demographics-driven household formations, and family formations–continue to be supportive, constructive, significant.

That said, it’s Day One. It’s a day to manage away the distraction of a macroeconomic data point, and set focus on doing things well, fast, and with commitment, sweat. A day for leaders to look at 60 or so days remaining in 2018, and next year, and five years ahead of that, and do what they do: Lead their teams to accomplish more than they ever thought they could.

This story was originally published in Builder.

{kind=link}