This story was originally published in Builder.

It took two weeks longer to deliver the average new house, from authorization to completion, in 2017 than it did two years earlier.

At the same time, the number of unfilled job openings in construction trended upward during that time period, and has continued an upward trajectory since.

See a connection here?

Logic would suggest that longer average permit-to-completion cycle times and an increase in unfilled construction jobs correlate.

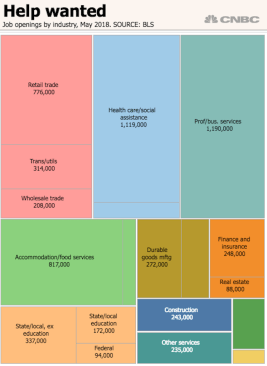

National Association of Home Builders chief economist Robert Dietz unwraps the data from the Bureau of Labor Statistics Job Openings and Labor Turnover Survey here:

According to the BLS Job Openings and Labor Turnover Survey (JOLTS) and NAHB analysis, the number of open construction sector jobs came in at 243,000. The post-recession high count of open, unfilled construction jobs was 255,000 in July of last year. The number of open construction sector jobs was higher than May of last year, when the count totaled 183,000.

The open position rate (job openings as a percentage of total employment plus current job openings) for May was flat at 3.3 percent. On a smoothed, 12-month moving average basis, the open position rate for the construction sector increased to almost 3 percent, a post-recession high. The peak (smoothed) rate during the building boom prior to the recession was just below 2.7 percent. For the current cycle, the sector has been above that rate since November 2016.

The overall trend for open construction jobs has been increasing since the end of the Great Recession. This is consistent with survey data indicating that access to labor remains a top business challenge for builders.

To us, two questions arise.

Can firms with unfilled construction job openings fill them at a greater rate than they have been doing since the housing recession ended?

Secondly, can firms reduce start-to-completion construction cycles if they don’t do a better job at filling unfilled construction headcount positions?

Let’s back up for a moment.

Construction is not alone in its current capacity plight, a shortage of relatively cheap labor to perform relatively rote tasks in what works out to be a highly variable process of producing shelter.

Here, when we raise the lens and look across a wider scope of the United States economy, we see that construction is by no means a leader among business and industry sectors with a shortage of workers. The capacity constraint condition is generalized. CNBC correspondent John W. Schoen writes:

The number of job openings dipped slightly in May, but continued to outpace last year’s levels. The decline in openings came as hiring increased by 173,000 to 5.8 million. And the rate of hiring—as a share of all jobs—rose one-tenth of a percentage point to 3.9 percent, the highest since March, 2007.

The result was a job opening for every unemployed person who was looking for one.

There’s good news and bad news in this data. The good news is that builders don’t have to look at the challenge of trying to attract fresh, trainable, hard-working talent into the building trades as one that is any easier or harder than that any other business or industry sector has to appeal to a next generation of value producers.

The bad news is that all of those other business and industry sectors will focus on the same universe of potential workers in their efforts to draw them in, making it tougher to convert such and such a high school student into a future building trade rock-star.

Now, let’s move the lens back in, focusing on residential construction.

A dream many hiring firms in home building are reluctant to awaken from is that if only the government would fix the immigration issue—agree on a guest worker program, for example—a reliable stream of low-cost workers would swell to its former size, and all would be well.

Many, though, are waking up from such a dream, and looking afresh at both the issue of attracting a new generation of people who want careers in the trades, and making those people part of a holistic push for greater productivity—faster, higher quality, more profitable, and more regenerative—in building processes.

One of the bright spots of transformation we see is that some builders don’t look at what they’re doing solely as getting the best deal—the lowest bid, often—from another firm to get a job done, or get products and materials that go into a house.

Instead, they look at their own organization—their company—as a value producer, not just for shareholders, investors, and customers, but for their trade and manufacturing partners as well. A preferred partner—the builder of choice—is not simply one who pays promptly and schedules for the fewest number of wasted trips to the site. A preferred partner is the builder who wants its trade partners to succeed, to be great places to work, to be attractive to a next generation of workers, and one that makes productivity—not just the lowest bid—the measure of success on both sides of the equation.

The right question to be asking, then, is not, “Why don’t young people want to go into home building?”

The right questions to be asking is, “How can I get young people to want to work at my firm? How can I get people to compete for jobs when I have an opening?”

The answer will involve commitment and investment on at least three levels:

1. Compensation.

2. Job growth and security through housing cycles.

3. Culture, where interests in sustainable profitability balance with interests in social impact.

Now, you and I know that a lot of the cause underlying longer authorization to completion times in home building traces to local government encumbrances and other regulatory delays. So, is that an acceptable state of affairs?

To read more stories like this, visit Builder.