This story was originally published in Builder.

From the Fed yesterday–as the Super Worm Equinox Full Moon hid behind thick clouds in many markets–builders got both carrot and stick.

Tidings that came as music to their ears are that pressure’s off expectations for mortgage rate increases, following the Fed’s signal it would hold steady on its benchmark rate for at least the balance of 2019.

What builders may not have wanted to hear is the Fed’s accompanying message, that it’s revising economic growth projections and inflation expectations down, and unemployment up, a combination of household spending and business fixed investment hesitancy, and declerating momentum in China and Europe.

All in all, the first day of Spring and the Federal Open Market Committee signal confirms a storyline that suggests that builders whose strategic and operational focus and execution is on lower-priced offerings for monthy-payment sensitive buyers have a good, clear run ahead of them into 2020, but after that, look out.

National Association of Home Builders chief economist Robert Dietz looks at yesterday’s FOMC mixed message as follows:

As a result of the Fed’s announcement, our next forecast update will include a reduced mortgage rate path. We had previously reduced our rate forecast due to our call for slowing growth for 2019 and, in particular, 2020. However, it is important to keep in mind that the reason for the anticipated change in Fed policy – softening economic growth headed into 2020 – means that the lower rate path will be accompanied by additional macro headwinds in terms of lower growth.

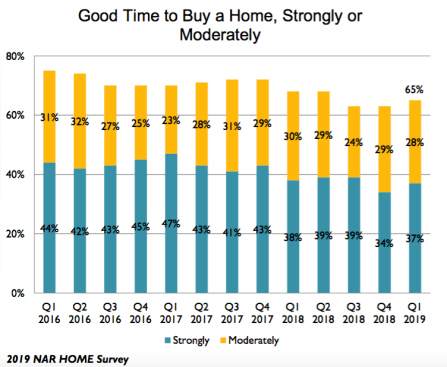

The impact of a steadied Fed benchmark lending rate–and lower 30-year mortgage interest rates–is already coming through in another indicator, the National Association of Realtors survey, Housing Opportunities and Market Experience first quarter release. A bounce-back in consumer moods about home buying is loud and clear:

NAR’s chief economist Lawrence Yun said several factors are helping to improve the attitudes of potential home buyers. “First, inventory has been rising, so those buyers interested in making a purchase will not be limited in choices. Additionally, more stable home price trends are leading to more foot traffic at various open house gatherings.”

While Dietz lauds the Fed telegraph of its plans, and asserts it will work as a helping force for builders in 2019, underlying reasons for the Fed monetary policy pivot are less than comforting. A silver lining may lie in fact that–in spite of some pretty severe turbulence and intensifying across-the-board volatility, fundamental drivers like jobs and income growth continue to construct a solid basis of demand.

Meyers Research director of economic research Ali Wolf considered this in a recent post to her blog:

“One would expect that once an economy hits full employment, generally defined by a 4.5% unemployment rate, wage growth would follow. The US economy hit full employment in March 2017 and it took a year and a half to see a shift. According to ADP, the payroll processor, wage growth hit 3.5% in the second half of 2018 after nearly a decade of minimal growth. Interestingly, individuals that switched jobs saw a 5.5% increase in their wage, a full percent and a half higher than last year. This is relevant because job quits are close to their highest level on record and 25% of Millennials voluntarily left their job in the past year.”

Jobs, good jobs, job formations, wage growth, and how all of these correlate with and fuel housing demand across the more or less pitched fields and shifting grounds of supply constraint–these conditions will likely make 2019 a tale of four housing markets.

Winners: those with new communities–open or ready-to start selling, finished land positions, and well-honed product and operations to meet demand for lower-price point homes and communities in each market, submarket, and customer segment. Stealth winners: those who’ve secured a solid, value-based position with known buyer groups in varying price-points, achieving higher margins via operational excellence, customer knowledge, and reputational strengths with suppliers and trades. Losers: Those whose product mix and real estate cost basis is exposed to weaker demand among move-up and second-time move-up buyers, contingency purchasers who have to sell a place to buy one, and others. Big losers: Anybody locked into personally-guaranteed debt on land positions that don’t model to predictable inventory turns over the next eight to 10 month.

In the tale of four markets, we see plenty of motivators for both buyers and sellers in the mergers and acquisitions arena, especially now that capital markets seemed to have regained appetites for deals to come.

This story was originally published in Builder.