This story was originally published in Builder.

Housing’s affordability crisis has gone global and risen–in our own country–to the highest level of policy focus almost ever in history. It’s a hot topic of the national conversation on Capitol Hill, the talk of happy hours and backyard barbecues, on the bus to work, on the radio home, and everywhere, all the time, and at a growing volume. It may even become a critical theme among candidates for the 2020 Presidential election.

Not building enough homes has caught up to us all, and the price we pay, and will continue to have to pay more as the consequences of not having enough new home development and construction goes up, and up, and up.

Wall Street Journal staffer Laura Kusisto writes:

Acute shortages are persisting despite millions of dollars invested and hundreds of thousands of units built. Some countries have focused on solutions promoting unshackled free markets while others have turned more to rent control and subsidies.

But no approach has solved the crises and most have other negative ripple effects.

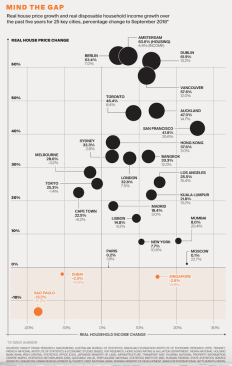

Across 32 major cities around the world, real home prices on average grew 24% over the last five years, while average real income grew by only 8% over the same period, according to Knight Frank, a London-based real-estate consulting firm.

Economists say it is striking that affordability has worsened even during a period of global prosperity over the last six years. But income growth has been unable to keep pace with a rapid run-up in home prices.

Still, the pervasiveness, progressive and accelerating nature, scope of impact–and now, sudden recognition and high-level discussion–of housing’s affordability crisis has had a numbing effect on many of housing development, investment, and construction’s market-rate players.

In a “what-you-control-vs.-what-you-can’t-control” world of tight reins, short tempers, and nervous, impatient financial capital, the affordability problem, and growing crisis is more and more, other people’s business. Mostly, the feeling is, big and little governments that make all the rules that factor into why it costs so much to develop and build new units for people to live in.

Fact is, though, the affordability crisis has begun to encroach in a widening gyre on turf, among would-be willing and able home buyers, and in the mindset of a society whose beliefs have begun to form around a shrinking universe of people who can pay to own or even rent in more and more communities around the United States.

What, we imagine, would it look like for market-rate players, with private-sector capital, and private enterprise strategies, and for-profit stakeholders to declare war on housing’s affordability crisis?

Such a war might begin by bending cost-of-entry barriers for essential workers–teachers, police and fire professionals and other first responders, key local personnel, etc.

Each month, we get reminded of where household incomes range, with stark clarity as to a growing gap between median income levels and what it takes to set aside money for a down payment and make monthly payments. This data, spotlighted by New Strategist Press editorial director Cheryl Russell, clocks in with the latest read on median household incomes:

The February 2019 median was 1.9 percent higher than the February 2018 median, after adjusting for inflation. It was 15.0 percent higher than the post-Great Recession low reached in June 2011 ($55,134)—a bottom hit two years after the official end of the Great Recession.

Sentier’s Household Income Index for February 2019 was 103.9 (January 2000 = 100.0). In other words, after adjusting for inflation, the February 2019 median was just 3.9 percent higher than the median of January 2000—almost two decades ago.

Problem is, people who make median incomes–and many more people who are in the 60% to 120% of area-median-income ranges, with wages that often come from essential worker occupations that towns, cities, and counties need to keep thriving–are priced out of a growing number of neighborhoods, and markets.

That’s where programs like Landed and Turner Impact–each designed to impact the workforce’s access to affordable for-sale and for-rent homes and communities, and each a top 10 finalist in the $250,000 Ivory Prize for Innovation about to be announced this week in Washington, D.C.–come in.

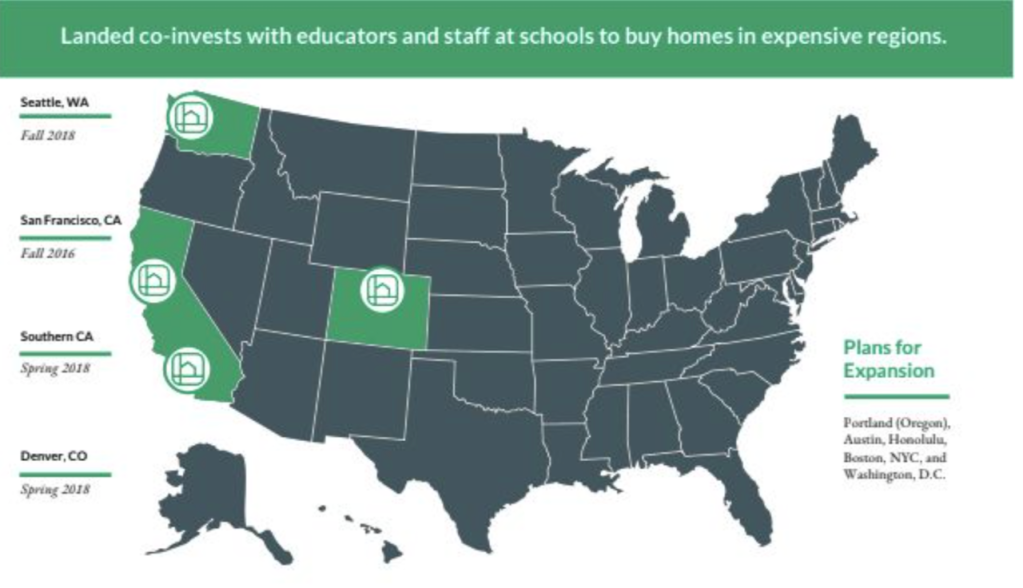

Landed, a financial fund, partners with teachers’ families on buying $100 million worth of properties by the end of 2020 in expensive markets around the nation, like California, Colorado, Seattle, and the east coast. Here’s its statement on how the money goes to work, first as down payment assistance, and then as an investment aimed at a share in the owners’ exits profits.

Landed: Impact

- Number of homes purchased with Landed down payment support

- Number of homebuyers

- Value of homes purchased with Landed down payment support

- Wealth built for Landed homebuyers

- Value of funds available to help educators purchase homes

- Number of school district partners

- Net promoter score of homebuyers Impact of retaining each educator, such as the number of students they reach and the number of years without turnover/hiring for their position

Landed plans to invest $100M over the next 24 months to support 1,400 educators. In doing so, the Company will talk to 100,000 educators about their financial health. Based on Landed’s impact framework, $100M to support educators will save public schools $50M in recruiting/retention spend and increase student earnings by $1B.

Landed is equalizing access to homeownership across income and race by providing a pathway for middle-class homeownership with equal opportunities for underserved minorities. In the Bay Area, only 24% of homeowners have a household income below 120% of the local median. Notably, 52% of Landed homeowners in the Bay Area have a household income of below 120% the local median, which demonstrates that Landed is unlocking homeownership for the middle class. Further, only 12% of Bay Area home buyers are underserved minorities, whereas 30% of Landed households include a black, Latino, or Pacific Islander homeowner.

Although it is too early to gauge the long-term impact of Landed on teacher recruitment and retention, we believe that down payment support is a powerful tool as districts work to attract and retain high-quality educators. Landed estimates that Landed-supported homebuyers serve more than 10,000 students across the Bay Area, Denver, and Los Angeles, of which approximately 38% of students qualify for free or reduced-priced lunch.

To date, Landed has helped nearly 150 public school employees purchase $100M worth of homes and put down roots in their communities.

Turner Impact, like Landed, is looking for an accupuncture-like effect through its capital investments in the preservation of affordable multifamily, primarily through a multi-pronged financial and community enrichment initiative. The Turner Multifamily Impact Fund is focused on protecting the supply of affordable workforce housing in urban areas by acquiring, preserving and enriching apartment communities for working individuals and families. As an established social impact investor, Turner Impact Capital advanced as a finalist for their work to invest in the preservation of affordable housing at scale.

Here’s a download on what the program is accomplishing:

Since its launch in 2015, TMIF has preserved affordability for over 11,800 families and individuals, over 1,500 of whom were children, growing the portfolio to a total of 6,877 units. These families and individuals reside in 20 communities, throughout 8 Metropolitan Statistical Areas across 5 U.S. states, all acquired and enriched over the last three years. These communities are generally mid-1980’s vintage, garden style apartments in low-income census tracts with 220 to 600 units per community. On average, rents at these communities are $1.04 per square foot, or $893 per unit, well below the 80% area median income average rent limit of $1,208 per unit. TMIF tracks price per square foot, resident income, and census tract affordability in order to adhere to its focused mission of preserving access to quality workforce housing.

The Fund’s typical resident is a mid-thirties high-school graduate who works in the service industry earning about $39,000 per year and has marginal credit, for whom for an additional $300 per month or $3,600 per year is meaningful relief from the spending tradeoffs they might otherwise make. There are, on average, 1.7 residents to each unit in the portfolio, demonstrating an even mix between single individuals and families of two to three children each, and other household structures.

During this time, the Fund has engaged residents in over 32,400 enrichment program participant hours, providing needed access to vital services. TIC has involved 137 resident professionals such as teachers, healthcare professionals, and police officers, as well as over 75 community-based organizations, to deliver these enrichment programs and ensure that the programs offered are truly responsive to the needs of that community as measured by a list of targeted program outcome key performance indicators, including overall improvements to residents’ sense of community and pride of rentership.

TIC currently measures the following impact metrics, among others, in addition to many other operational outcomes:

- Water Consumption

- Energy Consumption

- Environmentally-friendly materials used

- Environmentally-friendly upgrades or replacements made

- Program Participation

- Program Satisfaction

- Community Satisfaction

- Resident lease renewal rate

- Self-reported knowledge increase after program participation

- Self-reported change in academic achievement after program participation (youth educational programs)

- Improved Credit Score

- Resident Professional Utilization

- Resident Professional Efficiency

- Program Partners Engaged

- Crime Incidents

- Amount of security resources deployed

Through its innovative approach to property management, financial strategy and program implementation, TIC has increased resident tenure by over 20% and decreased economic loss by over 15%, demonstrating substantial impact for both stakeholders and shareholders. Additionally, TIC has completed substantial environmental improvements at each community, contributing to a 14% and 8% savings in energy and water consumption respectively across the portfolio. TIC has driven significant improvements in tenant behaviors between program participants and non-participants. For example, program participants are nearly twice as likely than non-participants to renew their lease. In addition, 95% of residents report satisfaction with the enrichment programs offered onsite.

By identifying, quantifying, and tracking these outcomes, as well as further developing new metrics on an ongoing basis, TIC can better support onsite teams and develop mechanisms for enhanced financial, social, and environmental outcomes.

A war on housing’s affordability crisis would take more than low-income tax credit investors, property managers, developers, and lenders to win.

It will take the market-rate players entering and engaging full-on, both to lower the barriers for people and households the economic and housing recovery has–to date–left behind, and to raise the achievable financial goals of many of those households who have begun to believe the housing business is not for or about them.

You can prove them wrong, and restore them to a willing–and able–role in expanding the business universe for market-rate players. The war is on.

The winners for the Ivory Prize will be announced at the National Press Club in Washington, D.C. on April 10th, 2019.

This story was originally published in Builder.