This story was originally published in Builder.

Quiz time. Which of the following statements could be “fake news,” and why?

1. Housing affordability remains flat in 2017

2. Homeownership is increasingly for the wealthy, according to the latest sales data

3. Homeownership is still financially better than renting

4. One of the above

5. All of the above

Fact is, there’s data that would back up all three statements as true. So, although it would appear that at least parts of each assertion would have to contradict at least parts of the other two, it’s hard to decipher how they all add up factually. And this is important because, while the data point you quote may be correct, the inference, interpretation, and action you take based on the data point might be off base.

One conclusion we’d reach, looking at the three claims in total, is this: New home building at the lower part of the price spectrum is more important this year than it has been in a long time.

To more fully appreciate this assertion, let’s look at some pictures.

First, a scatter plot graph that shows the relationship between Case-Shiller house prices—based on the sale of existing homes—and inventory levels from Calculated Risk housing and economics observer Bill McBride. McBride writes:

There is a clear relationship, and this is no surprise (but interesting to graph). If months-of-supply is high, price decline. If months-of-supply is low, prices rise. … In the existing home sales report released this morning, the NAR reported months-of-supply at 3.4 months in January. Based on the historical relationship, months-of-supply could double before house prices started declining.

This is where a healthier new-home market historically plays a big role in both housing momentum and the broader economic recovery plot line. By “healthier,” we mean that in normal recoveries, home builders can martial costs and push up volumes to compress the disparity between new homes and used homes. They’ve struggled to do that for a number of reasons, but they’re pivoting—like turning an aircraft carrier in a harbor—as we speak. If you look at the chart below, showing new home sales by price-range, you can see that, through August 2017, very few (less than 13 percent) new homes price in at below $200,000.

We show here how local, regional, and national regulation costs layer added expense to buyers of new homes. In broad strokes, the effect of land use fees, hook-ups, taxes, entitlements, etc. alone make it so that people who buy new homes pay, on average, $20,000 more for homeownership than people who buy existing homes.

This is the regulatory premium new home builders and buyers pay these days, on top of other expense items that make new homes more costly. Fact is, though, people want home ownership for good reason. The rents are too damned high, and renting, for many, doesn’t offer the stability, security, and a place to prosper financially as homeownership does.

Still, even as builders loudly lament regulatory burden as a reason they’re hesitant or constrained when it comes to offering lower-priced new home communities and homes, it doesn’t take them long to notice that one or two among them has figured out how to navigate those burdens, lower their own costs, vacuum out waste in their processes, size their homes, and deliver.

Two Texas-based builders—D.R. Horton and LGI—can take credit for stoking the operational, land strategy, sales, and product design fires that have become the rush into entry-level that most of the big builders are engaged in now.

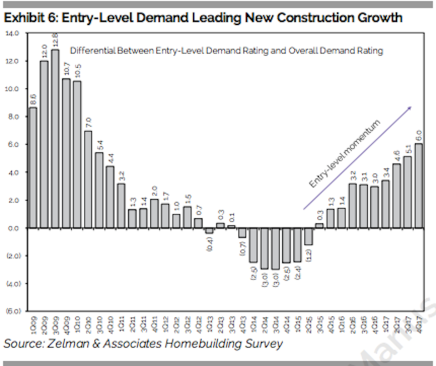

The Z Report‘s latest issue focuses one of Zelman & Associates’ analysis pieces on just how pervasive the commitment to entry-level product, communities, and price tiers among builders has become.

On a 0–100 scale, entry-level demand was rated 72.2, or 6.0 points above our proxy for all price points. That spread is the highest since 2Q10, which overlapped the expiration of the last home buyer tax credit. By year, the spread was worst in 2014, remained slightly negative in 2015 and then first turned positive in 2016.

Building more attainably comes down to this ongoing big challenge for each building firm, small, medium, and large.

Either you’re the cause of increased inventory—and more sales for you—at that sweet spot below FHA limits, or you’re the reflection of housing’s inability to fully activate a full housing recovery. Which will it be?

This story was originally published in Builder.