This story was originally published in Builder.

Hot markets are out there.

Although domestic migration and mobility rates are down, economies and housing activity have selected some markets as magnets for movers, some for jobs, some for improved prospects of attainable housing, some for prosperity and well-being, and some for the mere sake of starting over somewhere new.

Suburbs–considered dead or dying five years ago among popular commentators–have regained pep in their step and viability for the future, and small towns are showing up on more radars as baby Meccas of both solid employment, good cost of living, and affordable housing options. All this in stark contrast to the big 25 or so cities whose home prices and rentals have skyrocketed beyond both pocketbooks and belief.

What’s more, mobility, economic, and household trends that have sharply defined themselves over the past five years–putting increasing distance between themselves and the Great Recession–appear to have legs to last a foreseeable future for the next three to five years.

The presence and power of these conditions and their forward trajectory provide a moment of clarity, big-decisions, and determinism for small- to mid-sized production home builders in many of housing’s most active markets.

As we’ve been commenting in some way or another for the past 12 to 24 months, builders that have been able to or still can pivot, into land positions, product spec, and construction and sales operations toward the lowest and even lower spectrum of each market’s asking price range have improved prospects in many of those local economies still abrim with life.

Naturally, those who are first to establish, first to scale, and first to gain purchase with local land sellers, vendors, trades, and the surge of incoming customers get an edge.

For others to make the pivot, they’ve got to have two things going for them–besides a track record of excellence in porting operations across and into new operating arenas–capital and data.

Data that can match product, operational KPI, community development characteristics, customer segments, search behaviors, and financial models, needs, it goes without saying, to be more precise and less prone to mislead than ever. Fortunately, BUILDER siblings Meyers Research and Metrostudy have evolved tools, solutions, granularity, and scope of coverage to support pivot decisions for both large and small players.

Capital is another matter, partly because, while residential real estate writ large has enjoyed Belle of the Ball status as a safe haven for investors over the past six or seven years, most of that wherewithal has focused on multifamily investment in a finite sphere of markets.

Here’s Meyers Research Managing Director Steve LaTerra’s take on the current predicament for builders seeking capital to make their big pivot just when they need it most:

The amount of dry powder (cash reserves) has been steadily increasing since 2014. In fact, more money is chasing real estate opportunities today than at any time in history. However, over the last several years, much of the money raised for real estate investment went into apartments, industrial and other cash flowing asset classes.

$278 Billion

Available Real Estate Dry Powder – June 2018

Very little capital was directed to land and homebuilding which has led to the significant housing shortage today. While the downside risk of an investment in housing is limited, the threat of recession and the memories of 2009/2010 are keeping much needed capital out of homebuilding today.

This assessment gets affirmation in the latest data released by the National Association of Home Builders as part of its AC&D lending survey. NAHB chief economist Robert Dietz notes:

The volume of residential construction loans decreased 0.2% during the fourth quarter of 2018, ending a period of 22 consecutive quarters of growth. While the decline was small, the slowdown in the stock of lending for development purposes mirrors a recent NAHB survey finding neutral conditions for AD&C lending as interest rates increased.

Tight availability of acquisition, development and construction (AD&C) loans has been a limiting or cost factor for home building growth, but easing credit conditions and a growing loan base helped, until late 2018, expand residential construction activity, albeit modestly. According to data from the FDIC and NAHB analysis, the outstanding stock of 1-4 unit residential construction loans made by FDIC-insured institutions declined by $142 million during the final quarter of 2018, placing the total amount of outstanding loans at $79 billion.

This tightening, at this time, after fairly solid demand has depleted many private builders’ pipeline of finished vacant lots, and their need is to pivot both to less expensive, higher-maintenance, land positions, and to do it when uncertainty hovers over the next couple of years is hitting a crescendo.

Dietz further notes in a HousingWire piece that calls for Fannie Mae and Freddie Mac to step in and support builders in their efforts to pivot into land pipelines that support building more attainably-priced homes, that builders flat-out need building sites:

Since 2016, approximately two-thirds of home builders have reported low or very low lot supplies in their markets, according to NAHB surveys. The lack of affordable and ready-to-build lots is often cited by builders as one reason new construction volume remains below historic levels.

NAHB forecasts call for just under 900,000 single-family starts in 2019, compared with a need for between 1.1 to 1.2 million new single-family homes to keep up with population growth, household formation and replacement housing needs.

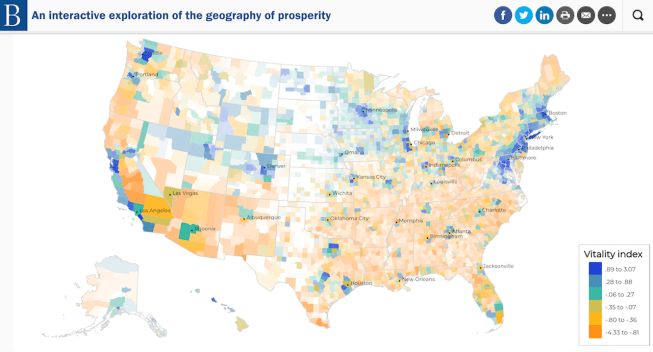

A heat-map is only helpful insofar as one can move development and building operations into the heat.

This story was originally published in Builder.