This story was originally published in Builder.

Builder sentiment has improved. Perennial optimism may partly account for this. Also, low–and fairly assured continued low–interest rates and a concurrent surge of consumer confidence gave builder respondents a boost as they looked at 2019 through a fresh lens of a new year.

Many might describe conditions this way: “Better than when they were worse.”

Coming off a mystifyingly weak sequence of monthly sales patterns in the final months of 2018, a fair number of builders, at least in some markets, report signs of life and improvement–in traffic and absorptions–as they rev the Spring Selling engines, open new communities, and try everything they can to keep expenses within a Maginot Line of price-vs.-pace acceptability.

A monthly report that takes a pulse of medium and smallish-production builders from BTIG analysts led by Carl Reichardt on behalf of HomeSphere concludes–at a high level–that what’s going on out in their selling communities is roughly flat with expectations, with nearly equal parts better and worse news at the margins.

Check for yourself from the top line commentary, and you’ll maybe agree that the most positive possible interpretation is that there maybe a few less negatives than in the prior report.

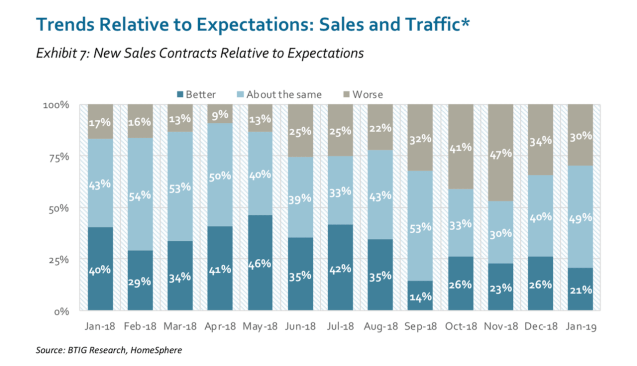

More builders continued to report sales down vs up yr/yr in January (32% down vs 29% up, nearly the same ratio as in December). Traffic looked a bit better with 33% of respondents mentioning yr/yr gains, and 28% declines. However, only 21% of builders said orders were better than expected, with 30% reporting worse than expected orders. Traffic quality (in terms of ability or desire to buy) was relatively stable yr/yr. Over half the builders we surveyed increased sales incentives on some or all of their homes for sale. The read-through for public home builders: we see no significant inflection point in January sales activity beyond seasonal norms.

- Sales & traffic. In January,29% of respondents reported yr/yr increases in orders vs 28% last month and 52% in January 2018. 32% saw a yr/yr decrease in orders vs. 31% last month and 15% in January 2018. 33% saw yr/yr increases in traffic vs 29% last month and 61% in January 2018. 28% noted a decrease in traffic, an improvement from 34% last month but well above the 6% seen in our January 2018 survey. While we note very slight sequential improvement in this data, we note no significant change, and comps remain well below data from a year ago. However, modest improvement in builders reporting up yr/yr traffic is at least a bright spot.

- Expectations. 21% of builders reported that sales were better than expected vs.30% reporting worse than expected sales. The better- than-expected reading was the second worst in survey history (September 2018 was 14%). We key on this data as reflective of, if anything, a disappointing January for builders.

- Pricing & incentives. 26% of builders increased some or all sales incentives in January (with no decreases), down from 41% in December but well above the 4% seen in January 2018. We would expect builders to ease off on incentive increases seasonally in January relative to December. 10% of respondents lowered some or all base prices in January (with no increases) vs 15% in December – again a change in line with what we would expect as builders anticipate a seasonal traffic pick-up.

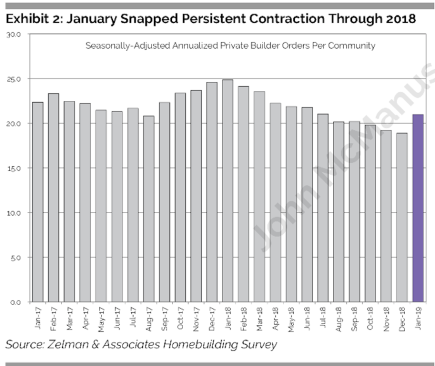

Another monthly survey of big builders–this one from Zelman & Associates–concurs with the “less-bad-is-good” take of the moment, with an overarching caveat that one month’s orders-per-community uptick a trend does not make. The best that can be said is that the losing streak has ended.

For most homebuilders, 2018 was both disappointing and frustrating, with demand and pricing power weakening unabatedly through the year despite continued macroeconomic health. For perspective, we analyze orders per community (absorptions) aggregated from private homebuilders participating in our monthly survey versus normal seasonality. Last year, this seasonally-adjusted measure declined in 10 months, with January and September (barely) the exceptions. This was the most negative annual skew over the 11-year history of our survey data. It was even worse than in 2008 when contraction was registered eight times.

We certainly would not suggest that 2018 was a worse overall housing market than in 2008, but it was void of good months to offset the bad. Thankfully, our recently-published survey results for this January broke this disheartening streak. From an order standpoint, absorptions climbed 39% sequentially, easily better than the 23-31% range over the last eight years and the 27% average for that period. Said differently, our seasonally-adjusted index jumped 11% from December, the best monthly improvement since May 2009.

It needs to be said, in addition to the observation that builders–except when they’re perennially pessimistic–are invariably optimistic, that comparables mean a lot when it comes to expectations and mood.

Compared with January 2018, last month and this one pale. After all, 12 months ago the new year came in buoyed by a tax reform that whacked corporate tax rates from 35% to 21%, and increased average tax payers’ standard deduction enough to send sentiment through the roof. That was supposed to be the accelerant to an already hot economy, plenty of job growth, and a big focus on killing regulatory barriers to residential and financial development.

Still, compared with the end of 2018, when global trade dislocation, political turmoil, cost inflation, and spiking interest rates sapped momentum out of the housing recovery’s confidence mechanisms, January and February simply “feel better” and there are signs that builders can calibrate switches and levers on their operations, pricing, and productivity to new settings that may reignite mojo, at least where economic fundamentals still underlie the market.

Comps on a year-to-year basis are likely to remain humbling, and comps to 2016 or 2017 activity levels may be as good as it gets. Many builders would certainly choose that scenario over an alternative one that suggests that a pre-recessionary housing deceleration is already pivoting a slow, steady upward trajectory to one that’s on a slippery downward slope.

One way or another strategy, tactical, and decision-making debate seems to center on how to control the controllable in 2019, positioning for opportunity, but more importantly, reducing exposure to big risk.

One camp of strategists proposes to focus their firms and offerings as outliers, distinguished from a crowded field of new, resale, and rental options on platforms of solid data, operational excellence, customer-experience fanaticism, and value. Such a strategy–amid ongoing expense pressure and a potentially shrinking pie of total universe buyers–would protect per-unit gross margins, and manage expected pace slippage with financial discipline and low debt service.

That camp–probably represented by local and regional private companies with prior cyclical downturn experience, rigorous processes, and outstanding customer care and marketing execution–is very likely the minority among today’s market rate for-sale players.

In the other camp are two separate types of firms who’ll pull out the stops at the expense of margins to drive volume.

One type–home building’s equivalent of the 1% population in wealth terms–will play the volume game as an offense strategy. The other type–more like the 80% of the middle and lower wealth and income spectrum among private home builders–will sacrifice margins, push discounts and incentives, and do nearly anythiing they can to keep pace at acceptable per-community-per-month absorption rates, as a defensive measure.

Let’s look at the two.

Large, public builders who’ve spent the past few years amassing local scale in their operating markets, and, concurrently, exposure to land positions, designs, operational processes, selling systems, and trade partners aimed at the lower-price spectrum of new home ASPs, look at playing the volume game in three stages. One, amass market share to even better leverage local scale. Two, eliminate competitors by undercutting them on price and rapidly drying uyp their access to customers. And, three, when the moment is right, leverage the market share and scalability gains into better margins entering the next cyclical pivot.

A defensive focus on volume has the goal of driving inventory turns at faster rates as a way of mitigating future risk–carrying costs, loan payments that come due without the cash-flow to meet them, covenants being tripped, etc. I.e. distress.

Which path you decide is the one for you and your team to take in the next 10 to 24 months depends on the data and operational DNA of your firm, its products, and how you connect and activate your customer. We would not venture to say that one size fits all.

What we would safely say is that, oftentimes, human beings err when they make decisions based on what they think the future has in store. So, while your forecast and strategy may correctly either focus on driving value, maintaining your margins, and standing apart from everybody else in quality and service, or the inverse, tempting buyers to act now on the purchase of a lifetime with inducements, incentives, discounts, upgrades, and then some, it’s a good time to review the catches, snags, snafus, and showstoppers that come with intensified focus on velocity in inventory turns ahead of an expected overall slowdown in activity.

Here are a couple of links to resources you may have missed recently, but that are worth keeping in mind as you reach the volume or value fork in the road.

and

Construction’s Seven Deadly Sins.

Fast, after all, is only fast when it’s right. Now is no time to let margin compression devolve into epic risk.

This story was originally published in Builder.