This story was originally published in Builder.

Just as the spring sales season starts to heat up, housing affordability has improved, according to Nationwide’s latest Health of Housing Markets Report.

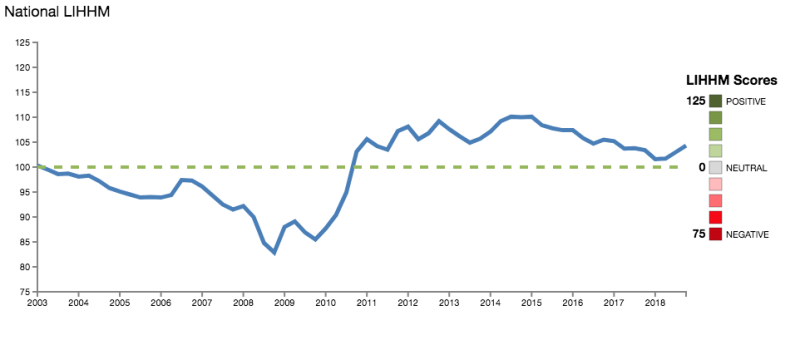

The report found that house price appreciation is slowing, mostly in response to higher mortgage rates. For the first time in a year, the report’s proprietary Leading Index of Healthy Housing Markets (LIHHM) is forecasting a positive outlook for the national housing market.

“The last few years have been difficult for home buyers. From unsustainably rapid price gains to higher mortgage rates to tight supplies of homes for sale, it’s been an increasingly difficult time to buy a home,” said David Berson, Nationwide senior vice president and chief economist. “But, with slower house price increases and recent declines in mortgage rates, coupled with a still solid job market and rising wages, the spring home buying season looks as pretty positive.”

LIHHM is unusual among housing market indices as it is a forward-looking measure of housing market sustainability. The demand metrics within the LIHHM remain positive with an ultra-low unemployment rate, continued solid job gains and a steady mortgage market.

Regionally, more than half of the LIHHM performance rankings were positive, an improvement from the last six months. Income growth is more aligned with house price appreciation, and household formations are strong in most markets. But, low housing supplies continue to hold back sales, even with stronger demand.

The 10 metro areas with the most positive LIHHM forecasts are, in order: Lawton, Okla.; Waterloo-Cedar Falls, Iowa; Sumter, S.C.; Trenton, N.J.; Watertown-Fort Drum, N.Y.; Houston-The Woodlands, Texas; Chicago-Naperville, Ill.; Hinesville, Ga.; Des Moines-West Des Moines, Iowa; and, Abilene, Texas.

The 10 MSAs with the least positive LIHHM outlooks are: Bismarck, N.D.; Kennewick-Richland, Wash.; Owensboro, Ky.; Pueblo, Colo.; Beckley, W.V.; Yakima, Wash.; Rapid City, S.D.; Midland, Texas; Ogden-Clearfield, Utah; and, Janesville-Beloit, Wis.

Tax reform affecting the high-end market?

New limits for the state and local tax (SALT) deduction and mortgage interest deductions in the Tax Cuts and Jobs Act of 2017 were expected to have a negative impact on the upper-end housing market.

Data from 2018 suggests that this has occurred. Price gains slowed the most for the highest-priced tier of homes, from 4.7% at the end of 2017 to 2.1% in December 2018, according to data from Black Knight. By comparison, the lowest-priced tier slowed more modestly – from 8.8% to 7.4% over the same time period.

The degree to which the tax changes were a principal cause of these price trends can be difficult to separate. Still, there are regional differences that suggest a measurable impact on the price appreciation of higher-priced versus lower-priced homes – likely as a result of the new tax deduction limits.

For example, in states such as California, Maryland, Massachusetts and New Jersey where homeowners would be more likely to use SALT and mortgage interest deductions due to higher home values and property tax rates, there was a sharper slowdown in price gains for the highest-price tier relative to lower-price tiers. In New York, while price gains accelerated across all tiers, the increase was smallest in the highest-price tier.

Going forward, the potential drag on demand for high-end housing from the tax changes could have a continuing impact on prices and sales activity in some local markets.

Hurricane-ravaged markets recovering

Local housing markets historically take about a year or more to recover from the rise in mortgage delinquencies that commonly follow hurricanes.

The HoHM Report found that heavily impacted housing markets in Florida and along the Gulf Coast of Texas by Hurricanes Irma in September 2017 and Harvey in August 2017, respectively, are finally returning to pre-storm conditions.

“While those areas are still recovering from the storms of 2017, the drop in delinquency rates shows that conditions are improving,” said Berson.

Texas markets running along the Gulf from Corpus Christi to Beaumont-Port Arthur and Florida markets from Tampa-St. Petersburg south saw significant reductions in mortgage delinquencies by the end of 2018.

This story was originally published in Builder.