The Olympics of higher volume residential development and building are on. As urgency and momentum show signs of fatigue in home building’s higher price tiers, a long-awaited moment–the activation of the entry-level market–has taken shape for a next leg of housing’s recovery marathon.

One of the big questions for home builders of all stripes, capital structures, and sizes is–as the pace quickens for lower-priced homes and communities–can margins hold as moving-parts heat up and multiply?

Mortgage products and innovation–two terms you just wouldn’t have seen together in the same sentence for the past 6 years or so—-have re-bonded for a fast friendship, as both Federal housing finance agencies and private financial service companies are amping up lending activity among a more inclusive universe of borrowers.

Risk-based pricing of loans, manual underwriting, higher loan to values, multiple-income household qualifiers, lower and lower down payment requirements, lender-paid mortgage insurance, and an expanded credit box based on borrower credit scores are gaining currency, with banks like PNC, Bank of America, US Bank and Wells Fargo leading a more aggressive charge into mortgage lending to first-time and entry-level home buying borrowers.

A virtuous cycle of growing confidence, set in motion by an intrepid, glacial improvement in the jobs and household income outlook over the past several years has sparked the housing recovery’s tipping point, tilting the playing field from exclusive, discretionary, opportunistic new home buyers more toward those whose early careers and family plans are now just kicking into a higher gear.

We talked about this important inflection point with Zelman & Associates ceo Ivy Zelman, who’s graciously serving as our HIVE Conference dean for capital finance, guiding a conversation to focus on what’s solvable among housing’s affordability challenges. Ivy notes that a recent raft of new lending and credit initiatives won’t change the complexion of the housing market wholesale, but they are likely to positively affect incremental improvement in the important entry-level tier of the housing price spectrum.

Ivy and her team have been seeing an important shift take place in market dynamics, which will have a dramatic effect on both headlines around housing’s recovery and on challenges to home builders’ business models, given that amping up in pace comes with a whole new set of risks to profit margins.

What’s happened to spark builders’ more concerted and aggressive move to respond to entry level demand that’s now been pent up for a few years? Here’s Ivy’s take:

“Once home builders felt confident that the mortgage products were more available, they responded by developing more lower-priced new homes and communities, and we’re seeing that play out in our field data,” Zelman says. “The consumer psyche improved, which in turn moved into the builders’ psyche, which is important when you’re running a company and putting capital to work, you want to know that there’s going to be a pool of demand who find the product to be attainable.”

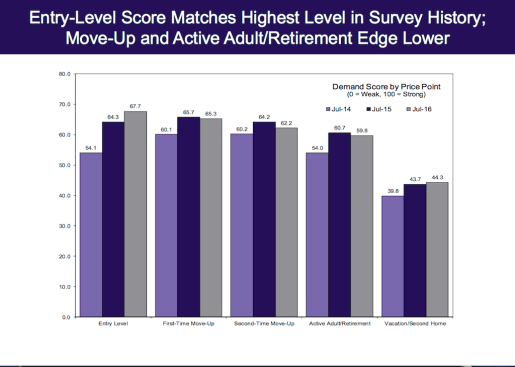

Zelman & Associates’ July analysis of the residential for-sale landscape notes among its bullet-pointed positives, “Entry-level segment score reaches highest level in history,” with commentary that volumes are positive in most segments, but higher-end and active adult have lost some spring in their step.

Here’s a look at that:

With permission from Zelman & Associates

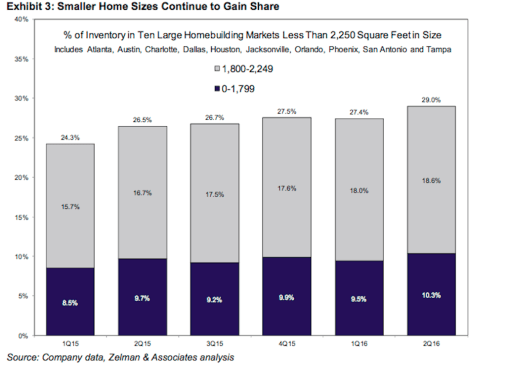

Now, as a proxy for better understanding what’s happening in home building’s lower price points, what Zelman & Associates does is to look carefully at square footage trends, since square footage and price points have a strong correlation irrespective of the variance in absolute prices in different geographical and economic regions.

In particular, Zelman has noted that, historically, homes of less than 1,800 square feet represented more than two out of five total new homes. That share shrank by half, to 21% in 2015. The news is this: big builders have started building more smaller–less than 2,250 square feet–homes with each successive quarter.

Here’s a slide that shows the progress.

With permission from Zelman & Associates

Now, there’s still a ways to go. As National Association of Home Builders chief economist Rob Dietz notes in a post published yesterday, the average square foot for a new single-family home fell from 2,658 to 2,616 square feet for the second quarter.

However, as you see from the activities of the public builders in her coverage, Ivy and her team are observing a tipping point in home sizes, so it follows that the down shift in prices is happening as we speak.

If you want to know the path, the trajectory, and the implications of the single-family for-sale housing mix shift, Ivy Zelman’s leading the conversation on how to manage production volume, investment, and operational performance as mortgage and credit product innovation flows into the system. Be with us at HIVE, September 28 and 29, in Los Angeles’ LA Live. Register here. Attendance is limited.