This story was originally published in Multifamily Executive.

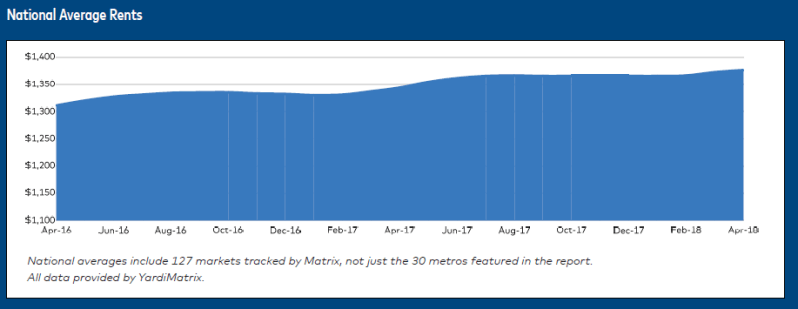

The national average U.S. multifamily rent rose by $4, to $1,377, in April 2018. This marks the second straight month of $4 growth and a $10 increase in the national average over the past two months, following a period of relatively flat rent growth from the summer of 2017 through February 2018.

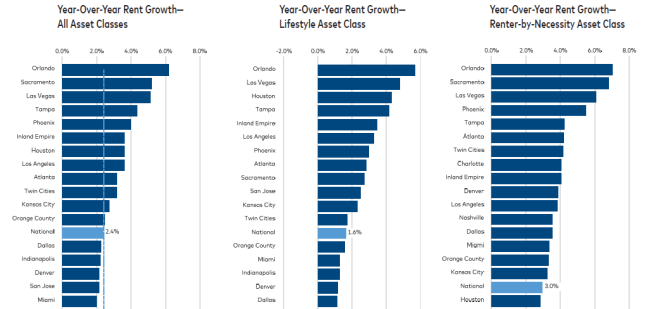

On a year-over-year (YOY) basis, rents rose 2.4 percent through April, down 20 basis points (bps) from March but close to the market’s 2.5 percent average growth range. The “Renter by Necessity” (RBN) apartment market’s rents rose 3.0 percent YOY at the national level, maintaining a 140 bps rent-growth difference from the “Lifestyle” renter market’s rent growth (1.6 percent YOY).

The latest Yardi Matrix Multifamily Monthly report attributes the period of flat rent growth and ongoing occupancy declines to the current supply glut in many metro markets. However, according to Yardi, the strong seasonal rent gains signal that rent growth will remain stable in the long term despite market headwinds. Demand is expected to remain high, and housing stock will continue to grow.

Supply types remain out of skew in some markets; some suffer from oversupply of new units while others don’t have enough market-rate or affordable units available. Yardi expects rents in these areas to drop slightly or flatten.

The Regional Picture

At the regional level, rent gains were observed in every major metro covered by Yardi Matrix except for Raleigh, N.C. Orlando, Fla., saw the strongest YOY rent growth, at 6.2 percent. Sacramento, Calif., followed close behind, at 5.2 percent, falling back into more moderate rent gains after a period of rapid growth. Other strong markets include Las Vegas (5.1 percent); Tampa, Fla. (4.4 percent); and Phoenix (4.0 percent). Yardi attributes their growth to their strong job markets, domestic migration, and warm Sun Belt climates.

Gains in high-growth Western tech markets, including San Jose, Calif.; Seattle; Denver; and San Francisco, were at above-trend levels in the latest three-month period following a longtime deceleration trend from 2015 to 2017.

On a trailing three-month (T-3) basis, which compares the past three months to the previous three months, rents increased by 0.3 percent at the national level. San Jose led the nation, with 0.7 percent rent growth on a T-3 basis, while Chicago, Denver, and Seattle bounced back at 0.4 percent after short-term rent declines in late 2017 to early 2018.

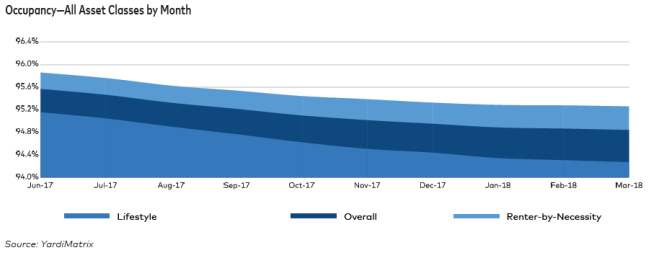

Occupancies

In 11 of Yardi’s top 30 metros, the occupancy rate on stabilized properties dropped by 100 bps or more YOY through March. Of those metros, only Sacramento had rent increases above the 2.4 percent national average; the average increase in this group is 1.3 percent.

At the national level, the occupancy rate fell by 80 bps, to 94.9 percent on a national level as of March 2018. (All occupancy data are current as of the previous month.) Seattle, Raleigh, and Nashville, Tenn., all saw 160 bps drops in their occupancy rates through March. Seattle’s YOY rent growth fell to 1.4 percent from 5.4 percent one year ago, while Nashville’s declined to 0.8 percent from 2.6 percent and Raleigh’s to 0.7 percent from 3.3 percent.

At the same time, about 360,000 new-unit deliveries are expected across the country this year. Yardi “isn’t bearish” on markets where occupancy drops have dovetailed with rent-growth declines but notes that rent growth there will likely remain weaker until new inventory is absorbed.

Houston is the only metro market in the top 30 where occupancy increased over this period, while Phoenix and Los Angeles saw the smallest declines in their occupancy rates.

To read more stories like this, visit Multifamily Executive.