This story was originally published in Multifamily Executive.

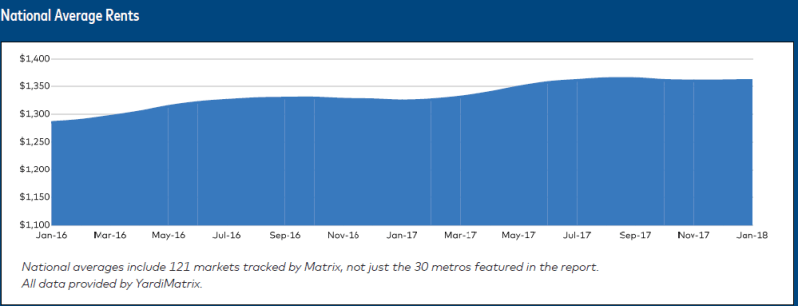

The national average U.S. multifamily rent rose by $1 in January 2018, to $1,368, matching the national average rent recorded in July 2017 by Yardi Matrix’s Matrix Monthly report. Rents rose 2.8 percent year over year (YOY) at the national level through January, a 20-basis-point jump from December 2018.

YOY rent growth has remained between a high of 3.0 percent and a low of 2.4 percent in the past year, following two years of above-trend increases. Yardi expects rent growth to remain in the 2.5 percent range but believes the next few months will provide a better idea of rent trends for 2018, as rent-growth trends flatten during the winter.

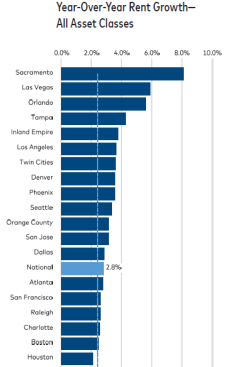

Two-thirds of the top 30 metros by multifamily rent growth are within 100 basis points (bps) of the national average, signifying metro-level rent growth that trends closer to the national median. Sacramento, Calif., sported the strongest YOY rent growth last month, at 8.1 percent, or more than 220 bps above the next metro on the list, Las Vegas, at 5.9 percent.

Sacramento’s rents have grown 40 percent over the past four years, and the average rent in the city has risen from just over $1,000 in February 2014 to $1,393 in January 2018. Yardi attributes this growth to Sacramento’s proximity to San Francisco, where the average rent is $2,545, and its low new-apartment stock, which has grown only 0.3 percent in the past 12 months.

Other top metros for rent growth include Orlando, Fla., at 5.6 percent, and Tampa, Fla., at 4.2 percent. Growth factors include low cost of living, warm climate, strong population and job growth, and, on a minor level, migration from Puerto Rico following the aftermath of Hurricane Maria.

Renter-by-Necessity (RBN) properties out-performed Lifestyle properties YOY, 3.3 percent versus 2.1 percent. Long-lasting demand for affordable units and an oversupply of luxury units have served to widen this gap over an extended period of time, Yardi notes.

On a trailing three-month (T-3) basis, Tampa topped rent increases in the short term, at 0.3 percent, followed by Miami, at 0.2 percent. The top three markets on a T-3 basis are all in warm climates with tight labor markets. Proximity to Puerto Rico may also be a factor in their growth. Seattle (-0.3 percent) and Portland, Ore., (-0.2 percent) are at the bottom of the T-3 rent-growth list for the second month in a row.

Occupancy and Supply

Roughly 300,000 new apartment units were introduced nationwide in 2017, and the national occupancy rate fell by 50 bps, to 95.2 percent, in December. (Matrix Monthly’s occupancy data are current as of the previous month relative to growth data.) Lifestyle occupancy stood at 94.7 percent in December; RBN, at 95.4 percent.

Five of the bottom six metros in rent growth added new supply at a rate above the national average last month: Washington, D.C. (2.2 percent); Austin, Texas (3.5 percent); Nashville, Tenn. (5.2 percent); San Antonio (3.4 percent); and Portland, Ore. (2.4 percent). Occupancy declined across all five metros.

This new supply is necessary to meet current and future demand, according to Yardi, and to address affordability issues in some heated markets. Overall, occupancy is healthy despite these regional declines. Rent growth will weaken as the new stock is absorbed, but the amount of deliveries is likely to peak in 2018, with new construction permits on the decline.

To read more stories like this, visit Multifamily Executive.