This story was originally published in Multifamily Executive.

Housing affordability is an issue of growing importance for the multifamily industry. Twenty million renter households—49% of all renter households—are rent burdened, meaning they spend more than 30% of their incomes on rent. And of those, nearly half (9.5 million) spend more than half their paychecks on rent, according to the U.S. Census’s 2017 American Community Survey.

There are a handful of factors contributing to this situation, but none so much as a fundamental demand–supply imbalance. Simply put, we haven’t been producing enough new apartments for the number of people who need and want them. And this problem will continue to worsen if it’s not addressed—research shows that, by 2030, the nation will need 4.6 million new apartments to meet demand. However, based on the average annual construction rate from 2011 to 2017, we’re likely to have only produced in the ballpark of 3.4 million units by then, leaving a potential shortfall of roughly 1.2 million apartments, according to estimates by the National Apartment Association and the National Multifamily Housing Council (NMHC).

It’s clear we need to build more. However, a major impediment to doing so is the increasing cost to build. The more expensive to build, the higher rents must be to make the project feasible financially. And the higher the rents, the greater the affordability challenges. As a result, most new development this cycle has been concentrated at the higher end of the market, with limited new development at the lower and middle ends of the income spectrum.

But just how expensive is it to build? While we hear anecdotally from multifamily developers and builders that construction costs continue to rise, it’s generally difficult to locate good data sources to put a numerical figure on those increases. A big part of that issue is that multifamily construction represents a relatively small segment of the overall construction industry.

However, NMHC recently pulled together, from government surveys as well as our own surveys, indicators that do exist. What we found is that all existing measures confirm that it does, indeed, continue to get more expensive to build.

Regulations

Research last year by the NMHC and the National Association of Home Builders (NAHB) found that 32% of a multifamily project’s total development cost can be attributed to the cost of complying with regulations. These regulations range from necessary regulations to protect life and safety to duplicative and onerous regulations such as using a particular type of construction material for aesthetic purposes.

Construction Inputs

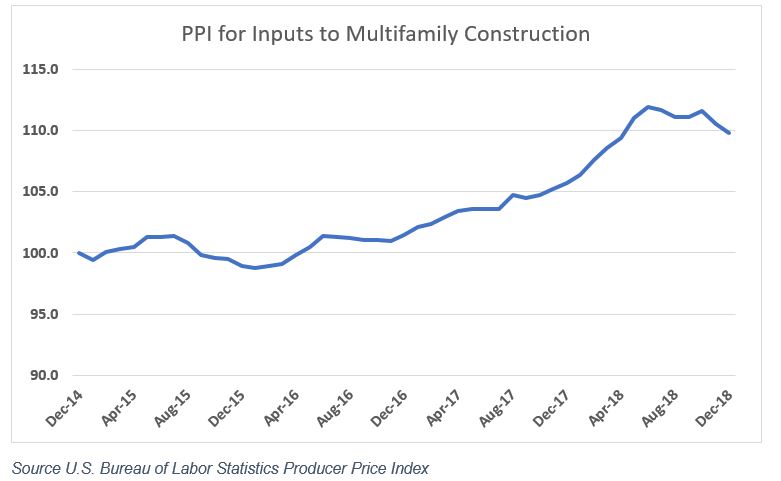

But regulations are just one cost consideration. The Bureau of Labor Statistics (BLS) releases its monthly Producer Price Index (PPI) for inputs to multifamily construction. This measure includes goods and services for multifamily construction but excludes labor and hard costs such as land. While data are only available back to 2014, the PPI rose significantly in the past year in particular, increasing 3.4% from December 2017 to December 2018 and 9.8% from December 2014. And while we don’t have hard data regarding multifamily land prices, anecdotal evidence, as well as increases in other sectors for these inputs, suggests these costs increased as well.

Tariffs

Beyond rising materials costs, tariffs have also had an effect on construction pricing. In NMHC’s January 2019 Quarterly Survey of Apartment Market Conditions, more than half (59%) of respondents said tariffs had raised costs—20% said by more than 5% and 39% less than 5%. In addition, over a quarter (27%) responded that tariffs had caused delays to projects, although no cancellations were reported. These results are consistent with the previous quarter’s survey, which asked the same questions.

Labor

Labor is increasingly scarce for a sector that has seen record demand, meaning for the already short supply of workers, they can command a higher price due to the increased call for their services. In NMHC’s July 2018 Quarterly Survey, more than half (54%) of respondents reported that labor was less available than one year prior, even at higher compensation levels. An additional 28% said labor was less available than at 2017’s pay levels, but when higher compensation was factored in, availability was about the same as in the previous year.

To be able to meet the demand for apartments by 2030, the apartment industry is going to have to build an average of 328,000 new apartments every year. Those apartments need to be at a variety of price points, because demand for new apartments won’t just be at the higher end of income distribution.

The above four, major cost drivers, along with others not discussed here, could translate into even higher rents down the line. In an era when affordability issues are becoming more acute, these high costs could pose risks for both residents and developers.

This story was originally published in Multifamily Executive.