RTKL.com

American Society of Hematology RTKL Washington, D.C. Last …

There’s something about surviving a financial crisis that changes people’s expectations. How else could a market that continues to report a national vacancy rate north of 16 percent, according to Colliers International, be considered anything close to “optimistic”? Still, preface that with “cautiously,” and you’d be describing how most experts assess the country’s current Class A office market.

After rising for 12 quarters, U.S. office vacancies declined in the last quarter of 2010, according to Colliers’ fourth-quarter 2010 office report. At the same time, the market absorbed just under 15 million square feet of space, more than double the amount absorbed in the prior quarter. This alone indicates that the office market has “turned the corner,” the Colliers report says, but CB Richard Ellis (CBRE) points out that new construction prospects for North America are dismal, with 7.8 million square feet expected to come online in 2011, followed by just 2.6 million square feet in 2012.

Hiring Power

It is easy to be encouraged by corporate profits, which rose to an estimated $1.64 trillion in the third quarter of last year, according to data from the Bureau of Economic Analysis. But the need for space isn’t driven by profits—it’s driven by employment, says Todd P. Anderson, a senior managing director in the El Segundo, Calif., office of CBRE. It’s not until a company hires more people that it increases its space requirements.

The nation’s unemployment rate is on a downward trend, according to the Bureau of Labor Statistics, but nonfarm payroll employment has yet to show significant gains. Still, Jones Lang LaSalle (JLL) identifies three “rising markets”—Pittsburgh, San Francisco, and Washington, D.C.—in its U.S. fourth-quarter 2010 Office Outlook. The balance of the country is moving through the “bottoming market” phase.

“Fourth-quarter data confirms our view that the U.S. office market has entered the recovery stage and will likely make continued progress, assuming the economy stays on the current path. Most encouraging is the 12-month-long gain in private sector employment,” says Colliers chief economist Ross Moore in that company’s report.

Richard Kadzis, vice president of strategic communications for CoreNet Global in Atlanta, agrees that there is an undercurrent of optimism. “Boards are starting to pressure companies out of asset-protection mode,” he says. “Companies are going to start reinvesting in their businesses again.”

Stay or Go?

Many American companies are still cutting margins and not inclined to deal with the capital outlay associated with relocating. Because of that, says James E. Prendergast, AIA, a partner of Goettsch Partners (GP) in Chicago, many more tenants are choosing to stay put. “The conventional leasing model assumed 25 to 30 percent of tenants would ‘re-up and stay’ when their leases came due. From 2008 through today, it [the renewal rate] is 65 to 70 percent,” he says.

In New York, where Colliers reports that the vacancy rate fell to 12.8 percent at the end of last year, landlords continue to make tenant concessions, says HOK principal Anthony Spagnolo. “Offers such as completely demolishing a space at no additional cost to the tenant and providing generous space upgrade packages have been more of the norm lately,” he says. Spagnolo also is seeing “strategic upgrades” to common areas, all designed to help landlords market properties as Class A.

JLL’s report notes that several of the largest leases signed in New York in 2010 involved less square footage than the tenants’ prior locations. In general, JLL says, tenants continue to remain stable from a size standpoint and are even rightsizing.

Joseph Brancato, AIA, managing principal of Gensler’s Northeast region, confirms that the firm’s corporate clients are focusing on strategic real estate decisions. “For many, their current portfolios are like Swiss cheese—in that there are pockets of vacancy throughout. They want to consolidate,” he says.

Green Gains Ground

Hraztan Zeitlian, AIA, principal and design leader in DLR Group WWCOT’s Santa Monica, Calif., office, argues that the most surprising development in Class A office development is the tenants’ awareness of and demand for green building measures. “In fact, a high level of incorporation of sustainability measures is now a prerequisite for Class A office buildings,” he says.

An ongoing study of a national office portfolio managed by CBRE reveals that sustainable buildings are expected to generate stronger investment returns than traditionally managed properties. The study found that owners of sustainably managed buildings anticipate a 4 percent higher return on investment than owners of traditionally managed buildings, as well as an increase in building value. Roughly 79 percent of owners surveyed believe that sustainable properties yield an increase in building occupancy and rental income.

A Better Balance Sheet

If growth plans or a desire for more efficient, greener spaces don’t spur moves, a proposed lease-accounting change from the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) might make firms reconsider their office needs.

In what Real Capital Analytics (RCA) cites as the largest single-asset transaction of 2010, Google paid $1.8 billion for 111 Eighth Avenue in New York. Not only did this result in a fast-schedule job for HLW International, which followed LEED-CI guidelines to transform the 100,000-square-foot floorplate into individual and team spaces fit for “Googlers,” it may portend more corporate buyers, according to RCA’s U.S. Capital Trends January 2011 Year in Review.

As CBRE’s Anderson explains, the proposed accounting change, known as FAS 13, will require companies to record real estate leases and leased equipment as amortization and interest expenses on the income statement, and add them to their balance sheets as assets and liabilities. The final standard isn’t expected until later this year, but Anderson says his colleagues and clients expect it to be codified.

“On a practical basis, FAS 13 will have the biggest impact on publicly traded companies because private companies are less sensitive to the analysis of their financial statements,” Anderson says. Kadzis estimates that $1.3 trillion, at a minimum, will be moved to corporate balance sheets as a result of FAS 13, and more expensive, short-term leases are expected to rise in popularity as a means to minimize the rule’s effects. As for who will opt to build or buy, Anderson says a company that leases most of its space will have to decide if it makes more sense to lease or buy, especially if it needs to control space for 10 years.

“This will result in a higher ratio of owned assets,” Kadzis says. “People previously leased [more than owned] for flexibility and lease purposes. With the FASB change, everyone has to think differently.”

Foreign Affairs

With so little new office development in the U.S., architects have increasingly been drawn to Asia. Matthew C. Larson, Assoc. AIA, GP’s director of business development, estimates that Asia work used to account for one-third of the firm’s practice. Today, it’s closer to 40 or 45 percent, he says, adding that GP has about 15 projects currently in some phase of development in China. RTKL vice president Scott Kilbourn, AIA, reveals a similar pattern at his firm. “Three years ago, one half of our commercial work was in the U.S., and Asia accounted for one-fourth or one-fifth of the pie.” Now, half of that work is overseas, much in Asia, he says.

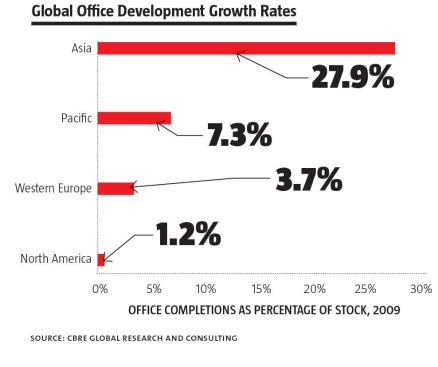

Driving this shift is the fact that 65 percent of new office development slated for completion between 2010 and 2012—190.6 million square feet—is planned for the major commercial centers of Asia, according to CBRE Global Research and Consulting.

Like many American firms working in the region, RTKL and GP can trace their work in China back about 20 years, and both maintain China offices. While larger firms may be better equipped to serve foreign markets, design the complex mixed-use projects typical of the region, and navigate its financial system, Kilbourn contends that smaller firms can create opportunities through associations with Chinese firms or joint ventures.

“In China, there remains a very high demand for international architects,” Kilbourn says.