This story was originally published in Multifamily Executive.

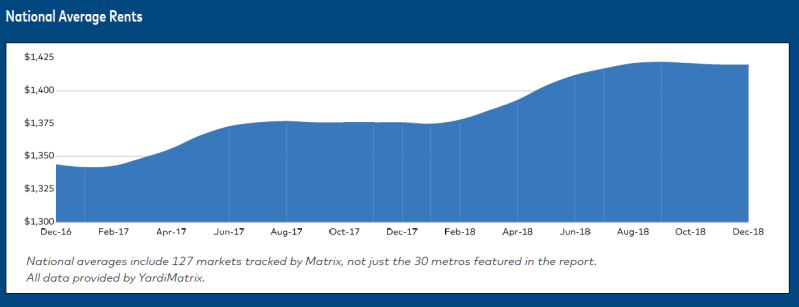

The national multifamily rent remained at $1,419 in December, according to the latest Matrix Monthly report by Yardi Matrix, while year-over-year (YOY) rent growth stayed flat, at 3.2%, unchanged from November 2018.

2018 marks the multifamily sector’s eighth-straight year of strong performance. Rents have increased by 31% at the national level since January 2011, and annual rent growth has been at least 2.9% in each of the past eight years except 2017. While rent growth has remained flat since the summer, the year’s final rate of 3.2% slightly exceeded Yardi’s expectations.

Although the cycle’s length has sparked some worry about its continuance, multifamily fundamentals are expected to remain strong in 2019. Multifamily demand continues to be high, despite financial volatility in some markets, and various social factors are working in the sector’s favor, including student loan debt (which inhibits homeownership), retiree interest in rentals, and families remaining in rentals for longer periods of time. Supply remains growth’s largest obstacle, with 300,000 new deliveries expected again this year.

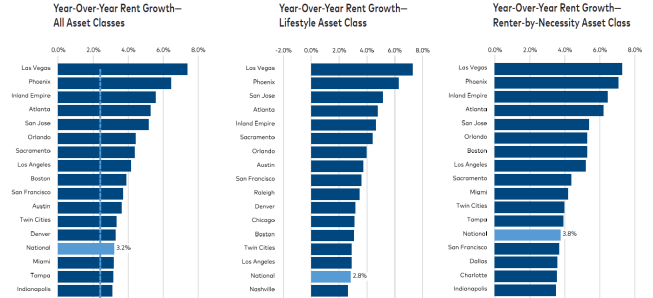

Western, Southern, and Southwestern markets are again expected to lead rent growth at the regional level in 2019. Las Vegas experienced the strongest December rent growth, at 7.3% YOY, followed by Phoenix, at 6.5%, and the Inland Empire (Calif.), at 5.5%. Las Vegas and Phoenix both benefited from migration out of high-cost markets, job growth in tech and finance, warm weather, and a relatively low cost of living.

Rents remained unchanged on the national level on a trailing three-month (T-3) basis, which compares changes from the past three months with those from the previous three months. According to Yardi, the final three months of the year are the slowest for rent growth, especially in cold-weather markets.

Las Vegas was the fastest-growing market on a T-3 basis, at 0.3%, followed by Phoenix, at 0.2%, and Los Angeles, the Inland Empire, and Orange County, Calif., all at 0.2%. Yardi attributes this spike to the failure to repeal California’s Costa-Hawkins Rental Housing Act, which would have allowed municipalities to impose rent control.

Overall, the financial market volatility that exploded at the end of 2018 is expected to continue into 2019. The 10-year Treasury rate has fallen 60 basis points over the past two months, and Federal Reserve chairman Jerome Powell has indicated the Fed may slow its tightening in 2019. Economic growth is slowing across the world, and a trade war remains a consistent threat.

In the short term, however, Yardi expects this activity will have very little impact on the stability of the commercial real estate sector. Space demand is based on long-term rather than short-term drivers, and U.S. real estate remains a favored asset for investors across the globe. As stocks and bonds remain volatile, more capital may even enter the sector as investors look for stable assets.

This story was originally published in Multifamily Executive.