The Rules is a monthly series covering important regulations in a clear manner for architecture, engineering, and construction professionals.

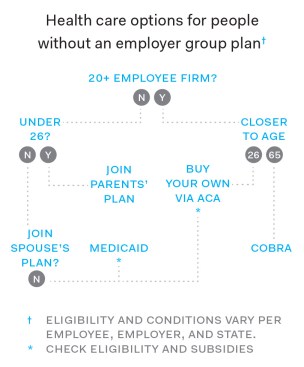

One immediate concern following a layoff or work-hour reduction is the impact on health care coverage. If your firm has 20 or more employees, the Consolidated Omnibus Budget Reconciliation Act (COBRA) gives workers the right to keep their group health insurance plan if they lose or leave their jobs, or if they no longer qualify for coverage due to reduced work hours. Ask “if your employer will be helping to subsidize COBRA coverage,” says Jennifer Berman, CEO of Pikesville, Md.–based MZQ Consulting, which specializes in benefits compliance. Otherwise, individuals “can be required to pay up to 102% of the cost of that coverage,” which amounts to the cost of the plan plus a 2% administrative fee.

That may be too expensive for the newly unemployed. The national average COBRA premium is approximately $600 per month for individual coverage, estimates Den Bishop, president of Holmes Murphy & Associates, a Des Moines, Iowa–based insurance brokerage that represents more than 750 architecture and engineering firms in the Midwest. “While there is debate in Washington, D.C., about subsidies for COBRA continuation,” he says, “there is nothing in any of the recovery funding for this yet.”

Losing health coverage is typically considered a qualifying life event, so you can be enrolled in your spouse’s employer health care plan, if the option exists. If you are under the age of 26, you can join your parents’ plan thanks to the Affordable Care Act. You may also be eligible for Medicaid, a government-funded, means-tested program for low-income adults, families, and the elderly; eligibility varies by state.

Another option is to purchase an individual health insurance plan. The Affordable Care Act Marketplace offers a range of options, though not every insurer offers plans through that exchange. “These plans are priced based on location and also age,” Berman says. “In many cases, COBRA will be better in terms of pricing for those closer to age 65, but younger individuals may be better off purchasing coverage on their own.”

Bishop says, “Based on an individual’s income—which may be difficult to determine if they just lost their job—they might qualify for a subsidy for individual coverage, or could even qualify for free coverage through Medicaid.” However, you can only receive the subsidy if you purchase a plan through your state’s health insurance marketplace.

Though the ACA continues to be contested in court, Berman believes it is here to stay. “It has now been over 10 years and [the ACA] is deeply entrenched in our system at this point,” she says. “Any change would also severely disrupt the health care system in the midst of a health care crisis. In light of these factors, I believe any Supreme Court decision in the current cases would be very narrow.”

Introduced as part of the CARES Act signed into law in March, the Families First Coronavirus Response Act requires health care plans to cover all costs related to COVID-19 diagnostic testing—but nothing after that. “As a result, most health care plans cover COVID-19 treatment with the same deductibles and copays that apply to any other medical treatment,” notes John Arendshorst, a partner at Grand Rapids, Mich.–based law firm Varnum. “We have seen a few employer group health plans reducing or waiving cost-sharing with respect to [COVID-19] treatment as well, but they are not required to do so.”

Staying informed about health care coverage for you and your employees is even more crucial during the COVID-19 pandemic. “Health insurance in the U.S. is the most complicated consumer industry on the planet,” Bishop says. “And that was before COVID-19 came along.”