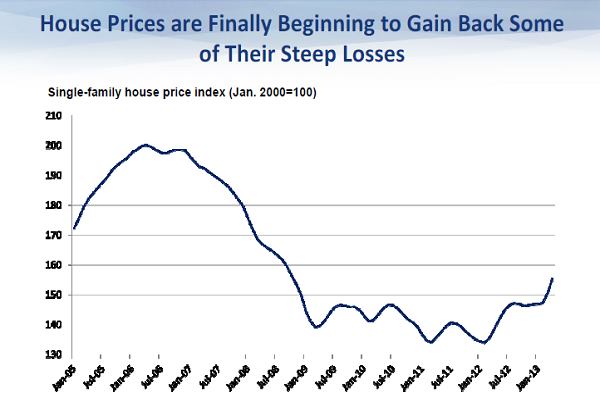

Residential construction is one the rise. Nearly every major residential sector is now reporting growth, thanks to the strength of remodeling. As the economy enjoys its fourth year of recovery, all signs indicate good, if not great, continued near-term growth, according to economists who participated in a mid-year construction forecast panel today.

One of those economists—Anirban Basu, chief economist for Associated Builders and Contractors—used the forum to explain an anomaly in the improving economy: nonresidential construction. Despite favorable market conditions, such as low interest rates, a boom in domestic energy production, and improving housing figures, nonresidential construction remains flat.

It’s reasonable to expect such a lag for about a year after an economy turns around, because nonresidential construction is a lagging indicator. The peak for nonresidential construction put-in-place, for example, came in October 2008—11 months after the start of the recession. But several years into the recovery, nonresidential construction spending has been flat—worse than flat, for the last few months.

Basu explains that the sectors of the economy that are experiencing the strong growth make up the smallest sectors of nonresidential construction. And vice-versa: The largest sectors of nonresidential construction aren’t recovering at all.

Lodging, for example, makes up just 2 percent of nonresidential construction spending. On the other hand, highway and street (a grab-bag of infrastructure projects) and educational together account for almost one-third of all U.S. nonresidential construction spending.

Now see how those sectors are faring in the recovery:

The almost 17-percent gain in spending on hotel construction has very little effect on national figures for nonresidential construction. The nearly 11 percent drop in spending on education-related construction does.

Further, some of the effects are more localized than others. The transportation sector comprises a relatively small number of large projects: the O’Hare Modernization Program, the Dulles Corridor Metrorail Project, and high-speed rail in California, to name a few projects under way or about to begin. Elsewhere, public spending is flat—and to a large extent, public spending determines nonresidential construction.

The effect on national construction employment is clear enough, so long as one understands that, by and large, the Specialty Trade Contractors sector comprises residential home builders, Basu says. These contractors are finding two-thirds of the new construction jobs, and the work is heavily tilted toward residential construction—consistent with an economy in which residential and remodeling spending is driving the recovery in construction.

Sequestration is only partly to blame. AIA president Jeffrey Potter, FAIA, has said that the budget sequester will cost more than $2 billion in federal investments in construction and design. It’s not the direct cuts to agency-related construction for the current fiscal year, Basu says, but the indirect costs associated with underfunding future public projects that is hitting nonresidential construction so hard. Despite the low interest rates and growth—good, if not great growth—stakeholders appear reluctant to authorize nonresidential-construction spending. Perhaps this owes to the sense of political deadlock of which the sequester is a symptom and not the cause.

The stubborn slow growth (or, not even growth) in nonresidential construction is simple to describe: The categories of nonresidential-construction spending showing improvement are small, while the categories declining are relatively huge. What turns it around is harder to say.

“Sequestration is just a taste of things to come,” Basu says.