For much of the spring, there were tentative signs that architecture firms might finally be emerging from one of the profession’s longest and most frustrating downturns in recent memory.

Project inquiries were improving. Multifamily work appeared to be stabilizing. Design firms that had spent much of the past two years navigating delayed projects and cautious clients began expressing guarded optimism that a recovery was taking shape.

That optimism may have been premature.

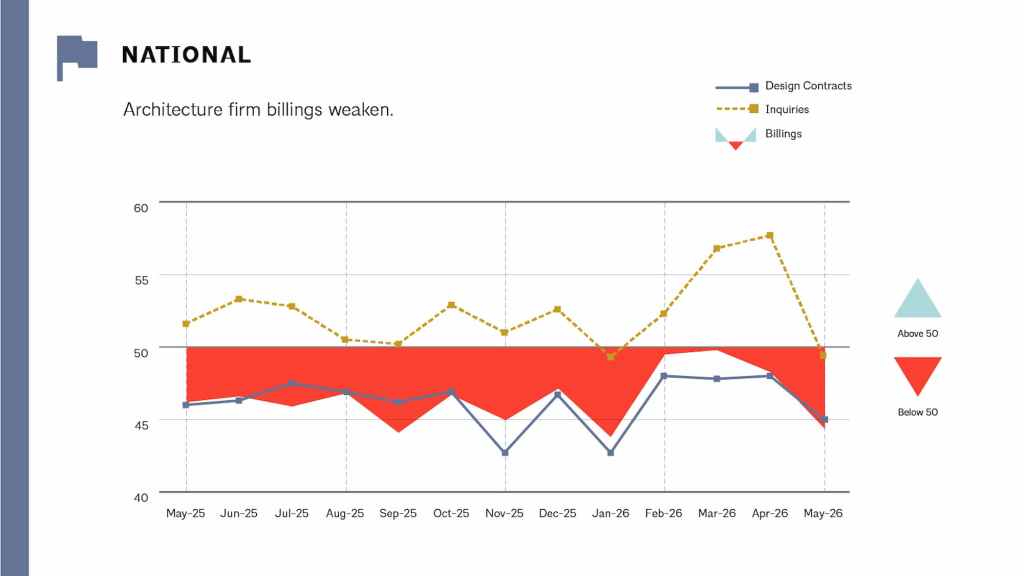

New data released by the American Institute of Architects shows that business conditions at architecture firms weakened significantly in May, with the AIA/Deltek Architecture Billings Index (ABI) falling to 44.5, its lowest reading since January and well below the threshold of 50 that signals growth.

The decline suggests that many clients remain reluctant to move forward with new projects amid a volatile economic environment shaped by geopolitical instability, elevated interest rates, persistent inflation, and uncertainty about the broader economy.

More concerning, the weakness extends beyond billings alone.

The project’s inquiries index—which measures potential future work—fell below 50 for the first time in four months, while the value of newly signed design contracts dropped to its weakest level since January. Together, those indicators suggest that the slowdown may persist well into the second half of the year.

For architects hoping that 2026 would mark a return to sustained growth, the latest data delivers an unwelcome reality check.

A Recovery That Never Quite Arrived

The architecture profession entered 2026 cautiously optimistic.

Following a difficult stretch marked by rising borrowing costs and a slowdown in commercial real estate development, many firms expected improving financial conditions to gradually unlock projects that had been stalled during the previous two years.

Instead, uncertainty has continued to dominate decision-making.

Developers remain challenged by financing costs. Institutional clients face budget pressures. Corporate tenants are still reassessing workplace needs in the wake of remote and hybrid work patterns. At the same time, geopolitical tensions have introduced a new layer of unpredictability into an already fragile market.

“The uncertainty created by the Iran conflict, and substantially higher energy costs, weighed on architect billings in May,” said AIA Chief Economist Richard Branch. “Higher interest rates, rapidly rising material costs, and continued labor shortages all contributed to softer demand.”

The comment reflects a growing concern across the design and construction industry that external economic shocks are increasingly influencing project decisions.

Architecture firms often experience economic shifts months before they become visible elsewhere. Because design work occurs at the earliest stages of the development process, changes in billings can serve as a leading indicator for future construction activity.

When architecture billings weaken, contractors, engineers, manufacturers, and developers often feel the effects months later.

Weakness Across Every Sector

One of the more troubling aspects of the May report is the breadth of the slowdown.

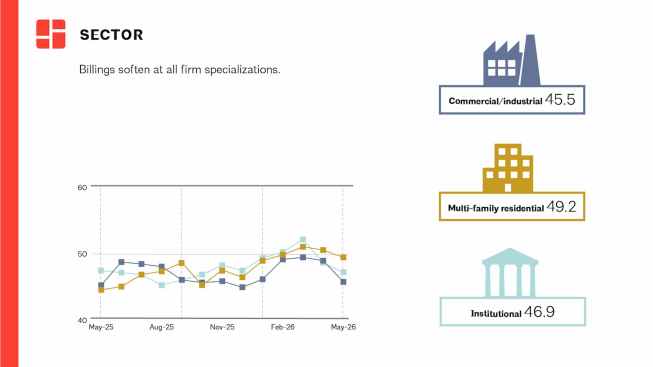

Every major practice sector reported declining billings.

Multifamily residential firms performed best with a sector score of 49.2, nearly reaching stabilization. That result follows several months in which residential practices showed signs of improvement after a prolonged correction triggered by higher interest rates and declining transaction activity.

Institutional firms—which include education, healthcare, and civic projects—recorded a score of 46.9.

Commercial and industrial practices posted a reading of 45.5.

Mixed-practice firms, often considered a useful barometer because they work across multiple sectors, reported the weakest performance at 44.1.

The data suggests that the slowdown is no longer confined to a particular building type.

Instead, caution appears to be spreading throughout the market.

For architecture firms that have relied on diversification to weather previous downturns, that trend could prove particularly challenging.

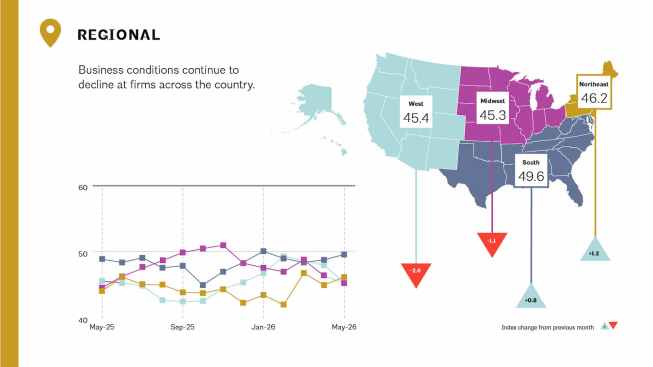

The South Remains the Bright Spot

Geography offered little relief.

All four major regions reported declining business conditions, though the South remained the strongest-performing market with a regional score of 49.6.

The Northeast followed at 46.2, while the West and Midwest posted readings of 45.4 and 45.3 respectively.

The South’s relative resilience continues a pattern that has defined much of the post-pandemic economy. Population growth, corporate relocations, manufacturing investment, and large-scale infrastructure spending have helped support development activity throughout much of the region.

Yet even there, growth remains elusive.

A score of 49.6 suggests firms are hovering just below expansion rather than experiencing meaningful gains.

In other words, the strongest region in the country is still contracting.

A Profession Stuck in Wait-and-See Mode

Perhaps the most important takeaway from the latest ABI report is not the decline itself but what it reveals about client psychology.

The architecture industry is confronting an environment in which many potential projects remain economically feasible but strategically uncertain.

Developers can still build.

Institutions can still invest.

Corporations can still expand.

But many are choosing to wait.

Questions surrounding energy prices, construction costs, labor availability, financing conditions, and geopolitical stability have combined to create a climate in which caution often feels safer than commitment.

That hesitation is increasingly visible in the design contracts index, which fell to 45.0 in May.

Because signed contracts represent actual commitments rather than preliminary interest, the decline suggests that clients are delaying decisions rather than simply exploring options.

The weakening inquiries index points to a similar pattern.

Fewer conversations today often translate into fewer projects tomorrow.

What Comes Next?

The architecture profession has become accustomed to volatility over the past several years.

Pandemic disruptions, supply-chain crises, inflationary pressures, labor shortages, and changing workplace patterns have all reshaped the industry’s expectations about growth and recovery.

Yet the latest ABI data raises a larger question.

What if the industry’s long-awaited rebound is taking longer than expected—not because projects have disappeared, but because uncertainty itself has become the dominant market force?

For now, architecture firms appear to be navigating precisely that reality.

The good news is that billings remain stronger than during the depths of previous downturns, and sectors such as multifamily housing continue to show signs of stabilization.

The bad news is that the recovery many firms anticipated earlier this year remains frustratingly out of reach.

As summer begins, architects are once again confronting an uncomfortable truth: the biggest challenge facing the profession may not be a lack of opportunity.

It’s a lack of confidence.