Before the pandemic hit in early 2020, most architecture firms were expecting another year of solid (if unspectacular) revenue growth. Almost half of firms expected to see billings increase at least 5%, a quarter projected declines of that magnitude, and the rest anticipated revenue close to 2019 levels. The biggest business concerns for firms entering 2020 were how to increase profitability, manage escalating overhead costs, work out ownership transition issues, and find new qualified staff to fill positions that they were planning to add or replace.

However, as the fallout from the pandemic began to intensify in March, many projects underway or planned suddenly had an unclear future, and firm leaders faced a period of unprecedented uncertainty. Over a two-month span beginning in March, our economy lost over 22 million payroll positions, and the national unemployment rate rocketed up from 3.5% to 14.7%. Consumer confidence in current conditions and expectations of future conditions each dropped by about 30% over this period.

Design and construction, while certainly not among the worst hit sectors in our economy, still felt the fallout. AIA’s Architecture Billings Index saw the steepest monthly decline in its 25-year history in the spring of 2020, in part because there were fewer new projects, but also because existing projects were running into problems. A survey of architecture firms conducted in September 2020 found that on a dollar basis, over half of all pre-pandemic active projects had been negatively affected by the recession. The most common cause was delays imposed by clients, contractors, or local and state governments. And a significant number of projects were put on indefinite hold or canceled.

Planning for the Coming Year

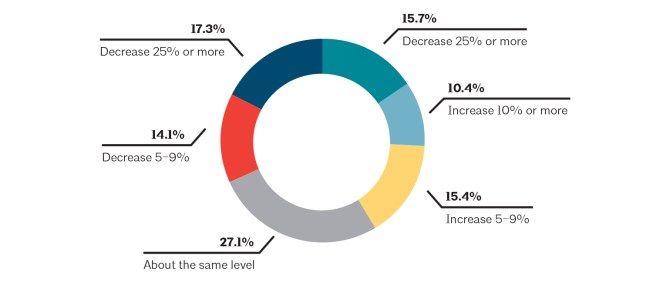

With promising news on the COVID-19 vaccine front, architecture firms are anticipating a return to more normal times. However, the bridge from the current situation to better market conditions will undoubtedly be challenging. While the slowdown in billings nationally has moderated in recent months, firms don’t believe that a return to growth will happen anytime soon. Almost half of architecture firms expect their billings this year to decline 5% or more from 2020 levels, according to an AIA survey conducted in October 2020. In a bit of good news, just over a quarter of firms are expecting growth in billings in 2021.

Figure 1: Architecture firms are projecting that revenue declines will continue into 2021

The outlook for this year varies a lot by a firm’s specialty. A surprisingly strong residential market—particularly for new single-family homes and home improvement projects, but also for more affordable multifamily units—has produced healthy project workloads for most firms specializing in this sector. Indeed, almost twice as many multifamily residential firms are expecting growth in billings of at least 5% this year as are expecting a decline of that magnitude. For firms specializing in commercial, industrial, or institutional facilities, it is just the reverse. More than twice as many firms with these specializations are expecting declines as are expecting growth this year.

However, firms of all specialties, sizes, and locations are expecting a challenging year ahead. For most firms, the sudden and steep economic downturn has left them struggling to retain their existing clients and projects, while simultaneously scrambling to find new projects. And virtually all firms have been dealing with a new set of issues—operating a practice in a pandemic and post-pandemic world.

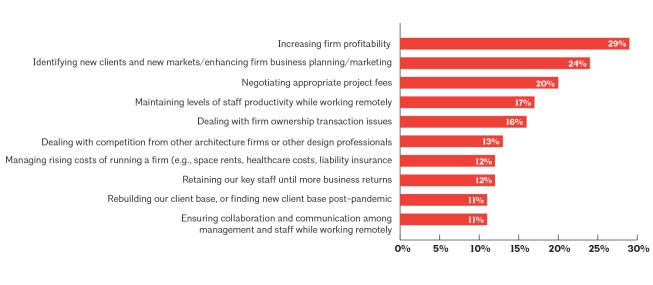

Some problems atop the list of firm business concerns for 2021 are chronic. When asked to list their top three concerns for the coming year, 29% mentioned increasing firm profitability—the top response from the extensive list offered to them. It was also the most frequently cited concern last year, when 28% mentioned profitability as one of their top three concerns, demonstrating that this is an ongoing challenge no matter the strength of the economy. Other concerns that topped the 2021 list that also ranked high a year ago are dealing with ownership transition issues (number 3 last year) and managing the rising cost of running a firm (number 4).

Fortunately, some concerns that were high on the list last year have largely disappeared this year. Given the extended period of growth in design and construction activity before this current recession, having adequate staffing to handle project workloads was a pervasive issue. Firm leaders mentioned “finding adequate staff”; “retaining staff”; and “offering competitive salaries and benefits” all as on their Top Ten list of concerns last year. With many firms reducing their payroll hours or headcounts this year, those staffing issues are no longer such a concern for most firms.

The changes to practice brought on by the pandemic within the last year have forced firms to operate very differently, and the prospects of running a practice post-pandemic are fraught with challenges.

Of the Top Ten business-related concerns for firms heading into 2021, four have direct connections either to operating conditions during the pandemic or to firm practices that will need to be addressed post-pandemic. These include:

• Maintaining levels of staff productivity while working remotely. Many firms understand that staff working remotely occasionally need to focus on household obligations instead of project work. Sensitive to this situation, many firms have enabled staff to vary their work hours, have encouraged staff to take more personal time, or have provided support in other ways.

Figure 2: Pandemic related issues emerge as firms’ top concerns for 2021

• Retaining key staff until more business returns. During any extended period of economic weakness, firms need to walk a fine line between financial responsibility and retaining as many employees as possible so that they can rebuild their practices once the economy recovers.

• Rebuilding the firm’s client base or finding new clients post-pandemic. While finding clients and projects can be a challenge even in the best of times, the pandemic offers a new set of marketing issues. Some established clients may be casualties of the pandemic. Other established clients may survive but will need to shift their design needs. Alternatively, given the way that the pandemic has fundamentally changed the economy, other potential clients and projects may emerge that are a good fit with the core competencies of a firm. Still, most firms will probably have to re-engineer their marketing strategies.

2021 Outlook: Nervous, But Optimistic

Staring at a steep economic recession that looks to linger for a while, a worldwide pandemic that could be mostly reined in midyear by vaccines, a staff that likely needs a remedial course on collaboration and communication, and a firm culture that likely needs a major reboot after an extended period of remote work, firm leaders face a daunting list of issues. However, most are feeling fairly optimistic that they can overcome these obstacles.

When asked at the end of 2020 about whether 2021 would be a great, good, so-so, challenging, or potentially disastrous year for their firm, firm leaders were generally optimistic. Almost half expected it to be a good or great year, and another quarter expected it to be a so-so year. However, the level of their optimism depended greatly on the firm’s specialization and the health of the local and regional markets that they serve.

Firms specializing in multifamily residential projects are typically feeling the warmth of the red-hot residential market, even if most of that activity is focused on single-family construction and the remodeling of existing homes. Still, over half (54%) of these firms are expecting at least a good year in 2021, with 12% anticipating a great year. Firms specializing in the commercial, industrial, or institutional sectors are a bit less sanguine about their prospects, but even so, about four in 10 of these firms are anticipating at least a good year, with about three in 10 expecting at least a challenging year. Regionally, firms in the Midwest are the most optimistic about their prospects for the year, and firms in the Northeast the least. In the Midwest, almost twice as many firms are expecting at least a good year as are expecting a challenging or potentially disastrous one. In the Northeast, those two groups are just about equal in size. No doubt there will be other issues as the year unfolds, but most firms seem to feel that the worst of this pandemic is behind them.