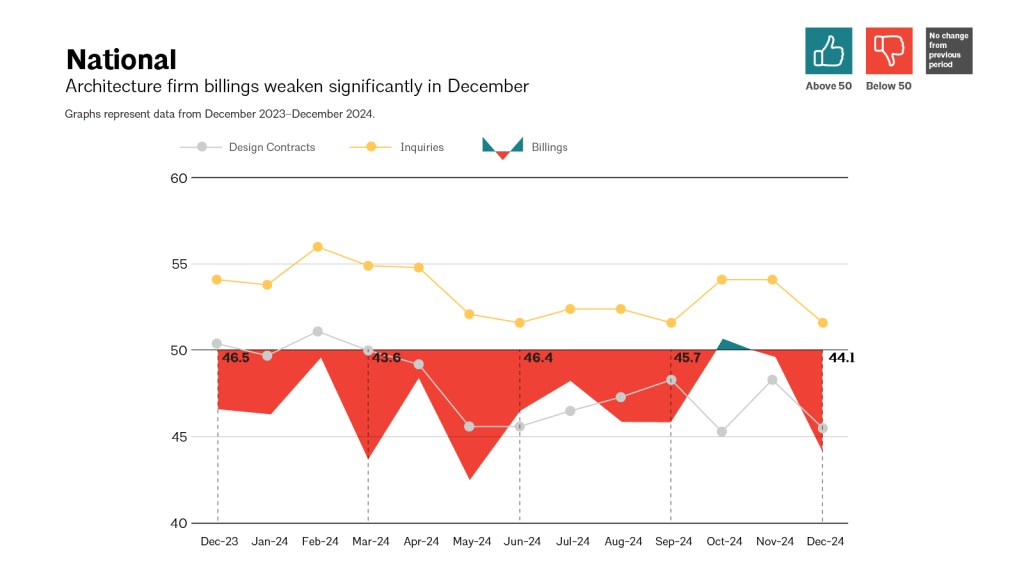

December brought a downturn in architecture billings, with the AIA/Deltek Architecture Billings Index (ABI) dropping to 44.1, marking a contraction in business conditions for the sector. After a period of stability in October and November, billings decreased, indicating a challenging environment as 2024 drew to a close.

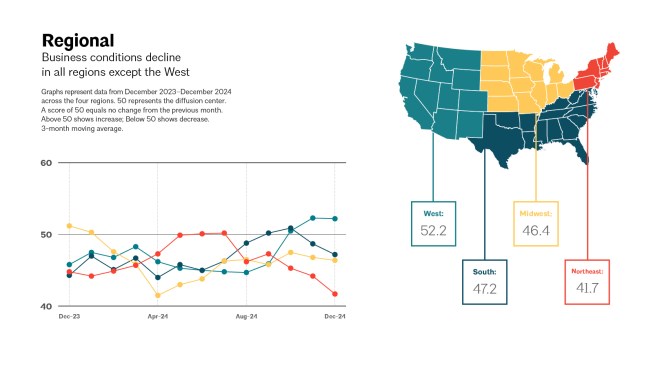

The ABI, a leading economic indicator of construction activity, reflects a nine to twelve-month lead time between architecture billings and construction spending. The December index suggests a decline across most of the United States, though firms in the West experienced growth for the third consecutive month.

Dr. Kermit Baker, Chief Economist for the AIA, expressed concern about the latest figures. “While there were signs that the design cycle was bottoming out in the fourth quarter, the December reading indicated a step back,” he stated. The persistent uncertainty about the viability of many planned construction projects has led to an extended period of cautious waiting into 2025.

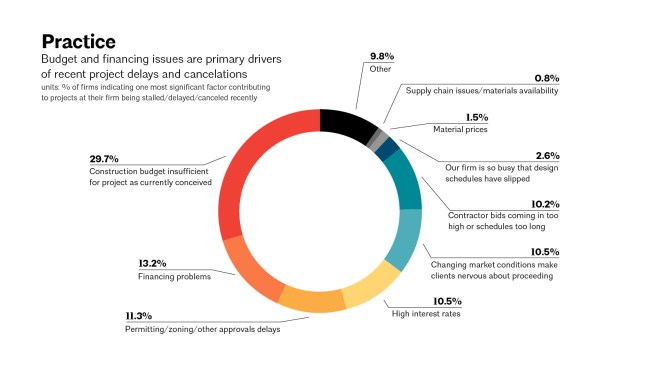

Despite the overall downturn, there are pockets of opportunity, particularly within the institutional sector, which has shown potential for growth over several months. However, other regions have not fared as well, especially the Northeast, where firms reported significantly softer business conditions.

The ABI detailed breakdown by region and sector for December includes:

- Regional averages: West (52.2); South (47.2); Midwest (46.4); Northeast (41.7)

- Sector index breakdown: multifamily residential (46.5); institutional (49.8); commercial/industrial (44.1); mixed practice (46.0)

- Project inquiries index stood at 51.6, suggesting a slow but ongoing interest in new projects.

- The design contracts index fell to 45.5, reflecting a decrease in newly signed design contracts.

These figures are calculated as three-month moving averages to smooth out the volatility and provide a clearer view of the trends.

Click here, to learn more about the AIA Billings index.