This story was originally published in Builder.

They call Warren Buffett’s age a Steinway. Eighty-eight white and black ivories make up a piano keyboard. To get to Buffett’s partner in profit at Berkshire Hathaway, Charlie Munger’s age of 95, you need a pipe organ.

They call Buffett the Oracle of Omaha. Each of his utterances–especially those he wordsmiths into his annual “Chairman’s” letter to shareholders–is extolled not merely for investment wisdom, counsel, and a bellwether view of risk and opportunity, as well as financial reporting accountability stripped of gobbledygook, but also for a signature plain English, salt-of-the-earth testament to honest and true American principles and simple, life-guiding values.

This past weekend Mr. Buffett’s annual letter came to light at 15 pages, shorter than has been its norm, but no less than usually freighted with matter, meaning, and portent, with piercing clarity, penetrating insight, and a call-to-action voice of transparency that rings so genuine it’s almost its own source of mystery and enigma.

As if to say, how can anybody this smart and so wildly successful also so openly chalk it all up to a humble blend of common sense and moral compass?

This year, Buffett urges us–as stakeholders in American business and the global economic complex as much as shareholders in Berkshire–to look at the forest for the trees.

“Investors who evaluate Berkshire sometimes obsess on the details of our many and diverse businesses – our economic “trees,” so to speak. Analysis of that type can be mind-numbing, given that we own a vast array of specimens, ranging from twigs to redwoods. A few of our trees are diseased and unlikely to be around a decade from now. Many others, though, are destined to grow in size and beauty.

Fortunately, it’s not necessary to evaluate each tree individually to make a rough estimate of Berkshire’s intrinsic business value. That’s because our forest contains five “groves” of major importance, each of which can be appraised, with reasonable accuracy, in its entirety. Four of those groves are differentiated clusters of businesses and financial assets that are easy to understand. The fifth – our huge and diverse insurance operation – delivers great value to Berkshire in a less obvious manner, one I will explain later …”

Buffett’s thematic gamut–real earnings performance, debt, what to do with cash, deals, and the health of the economy–adds up to a proof-case for continued investor trust in the Berkshire juggernaut, irrespective of ways momentary forces and accounting changes may obscure what’s really going on there that adds or subtracts value. Much of his message would be well taken as sage perspective, no matter what the business, what the sector, what the area of endeavor may be.

However, for those of us with vested and invested stakes in residential capital investment, development, and construction, Warren Buffett’s take, on both Berkshire Hathaway performance and on the economic and financial switches and levers he sees playing out in the months and years ahead through an almost inimitably reality-checked filter carry an extra charge of meaning.

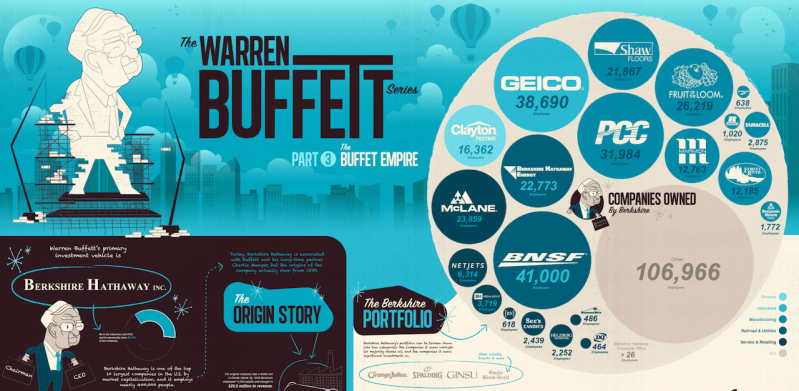

Berkshire’s investment portfolio of holdings includes a diverse basket of mostly consumer goods, services, financials, and transportation blue chips that produce the lion’s share of value and financial impact.

Still, it’s the enterprise’s fully-owned subsidiary operations Buffet names as “Berkshire’s most valuable grove – our collection of non-insurance businesses” that include some of housing’s own blue chip businesses that are of particular interest.

In them, we see a line-up of separately operated over-achievers, where the potential of convergence, integration, and cross-pollination has barely yet to have been tapped or leveraged to any significant degree.

Buffett writes:

Our two towering redwoods in this grove are BNSF and Berkshire Hathaway Energy (90.9% owned). Combined, they earned $9.3 billion before tax last year, up 6% from 2017…

Our next five non-insurance subsidiaries, as ranked by earnings (but presented here alphabetically), Clayton Homes, International Metalworking, Lubrizol, Marmon and Precision Castparts, had aggregate pre-tax income in 2018 of $6.4 billion, up from the $5.5 billion these companies earned in 2017.

The next five, similarly ranked and listed (Forest River, Johns Manville, MiTek, Shaw and TTI) earned $2.4 billion pre-tax last year, up from $2.1 billion in 2017.

Not even mentioned here, but included among Berkshire’s wholly-owned units are Benjamin Moore & Co. and Acme Brick. All told, Berkshire’s “building products” units employ about 57,000 people, and, together with real estate, financial services, insurance, retail, tech, distribution, transportation, energy, and very recently, health care insurance–make up an entire ecosystem of potential synergies, efficiencies, and opportunity for productivity and value improvement.

Our focus at BUILDER over the past four years or so has primarily been on the fact that Berkshire’s Clayton Homes has been busy acquiring site-built home building operators–seven of them now–each well-distinguished for having particular proficiency at delivering homes at lower price tiers profitably in their respective markets.

It’s a known and frequently asserted point that Berkshire has not assembled its portfolio of fully-owned and operated companies for synergies. They’re each discretely expected to perform–or, rather, outperform–at levels that set them apart.

Still, what Mr. Buffett seems to get as few strategic leaders do, is that housing–housing essential workers, working households, people anywhere and everywhere who depend on their day jobs for access to housing options–is a big part of what he calls the American Tailwind, the force and substance of bright promise for the nation’s future.

Laddering Clayton Homes up in terms of design appeal and quality, and yet keeping its pricing and financing solutions to within the means of average working American households is a big, bold affirmation in the sustainability and resilience in that American Tailwind.

And when you look at the possibilities for leveraging the entirety of Berkshire’s “building products” holdings with the transportation, distribution, real estate agency, finance, and insurance properties, and know that one of Warren Buffett’s areas of demonstrated passion and purpose is housing for working Americans, one can imagine that intra-empire deals, initiatives, efficiencies, and opportunities would only be natural as means of improving business performance for each of the entities.

And in a stretch–say, over the next 10 years or so–where it looks increasingly likely that disruptive innovation will upend and dislocate incumbent home building and development players who’re bound up in outdated methodologies, operational processes, and business models that can’t achieve 10x productivity gains, bets that Berkshire Hathaway’s “most valuable grove” might be a big part of that disruptive innovation would be well-placed.

The lens of near-term ups and downs, uncertainty, and jitters we’ve experienced in home building’s landscape over the past half-year-plus, as interest rate increases and the threat of more to come, shook confidence in monthly payment comfort zones.

Low to no debt, cash on hand for opportunities–which eventually will come when debt is less cheap and the number of bidders for each deal shrinks, and business operations that can work off retained earnings are critical keys to Buffett’s plan to weather another cyclical shift.

Meanwhile, a portfolio of operators–ideally positioned to blend housing products and materials, distribution, construction, design, technology, and marketing and sales– with the potential to learn from each other, invent things together, and try a lot of things, is the “grove” within the Berkshire Hathaway forest we’re most fascinated with right now. Why? Because, together it seems like they could bend the cost- and regulatory burden curve toward making more new housing more affordable to more workers in more geographies. Pretty good reason to be fascinated, eh?

Last week, it was Jimmy Buffett hogging the headlines in housing, thanks to the wild success of Margaritaville-themed 55+ communities from builder-developer Minto Homes. This week it’s all Warren. No, they’re not related, but that doesn’t mean the lessons learned from both are not pretty valuable right now.

This story was originally published in Builder.