This story was originally published in Builder.

The hazards of a top-down housing market–where several years running of success among mostly discretionary, higher-end buyers sling-shots a recovery without the benefit of underlying strength at the lowest price baseline–are coming clear.

The evidence, increasingly, shows that a housing recovery’s “second wind” may depend almost entirely on the residential investment, development, and construction community’s ability to blitz markets and sub-markets around the nation with attainably-priced, entry-level homes and communities.

All the [valid] noise about cost challenges notwithstanding, if builders fail to amp up production of quality affordably-priced homes for the kinds of people who’ve been the more recent beneficiaries of the nation’s second longest economic expansion on record, then all bets are off as to the sustainability of this housing cycle.

Last week, after housing starts, permits, and existing homes data came in for the month of August, the Wall Street Journal proclaimed, “The U.S. Housing Pipeline is Clogged,” noting:

New-home construction jumped in August, though underlying numbers suggest the housing market is stuck in the mud. Notably, the pipeline for new homes is moving in the wrong direction. Permits for multifamily homes are at the lowest level in years. Single-family homes aren’t much better—permits hit the lowest level in a year at an annual pace of 820,000. During the 1990s, single-family permits averaged more than 1 million a year.

The 1990s economy–much as it won a reputation as being a period of “conspicuous consumption”–managed to spread the benefits of a prosperous Wall Street across to Main Streets, fueling demand and pricing supply capacity in a relatively harmonious cycle after the early-decade regional bank meltdown and recession.

Year-on-year measures show 2018 as ahead of last year, but month-to-month, the last few months’ direction at the macro level has started getting people nervous in spite of economic momentum, especially in a broad context of volatility and political turmoil.

National Association of Home Builders chief economist Rob Dietz unpacked some of the consternation on August’s fall-off in single-family permits by looking further into data on the relationship of permits to the start of construction on new homes.

There has been an increase in the count of homes for which permits have been authorized but construction has not started. For single-family homes, there are currently 93,000 permitted units that have not begun construction. This is up 19% from August of 2017, when the total was 78,000. This increase is consistent with NAHB survey data indicating a pause in some planned construction activity due to the increase in building material costs during the first part of 2018.

One- and two-month housing metrics–prone to revision and significant margins of error–are really no lodestar to base investment and business decisions. They’re full of head-fakes, time-frame biases, and normal inconsistencies.

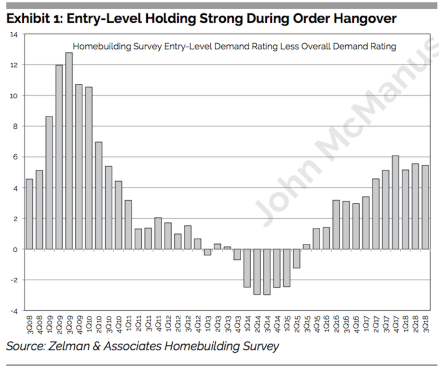

Still, a full industry-wide plunge into serving an as-yet, largely unmet need to attract aspirational, early-career households on to the ownership dance floor can not come a moment too soon. From the looks of things, that all-out immersion may be forthcoming, but not until 2019. From The Z Report’s latest series of analyses (for a free trial, link here), Zelman & Associates notes:

“According to our contacts, 35% of this year’s land investment dollars are being spent on future entry-level communities, which compares to a current share of deliveries for the same group at 30%. Translating today’s investments into future units, we estimate that this differential implies entry-level housing production will be expanding at a rate roughly twice the overall market.”

Of course, the clamor over go-vertical costs–labor, land-use, materials, and now, pricier finance terms–may be justified, based on forward business modeling of a more concerted mix-shift to the lower end of the new home price spectrum. Risk quotients are high and rising.

A timely insight in how company leaders measure and respond to risk crops up among the Harvard Business Review’s current line-up of business strategy essays, “A 6-Part Tool for Ranking and Assessing Risks,” by Security Management International execs, Luke Bencie and Sami Araboghli.

CARVER is an acronym that stands for:

- Recognizability: how likely it is that an adversary would recognize the asset as a valuable target

What builders and their design, development, investment, construction, and distribution partners must assess–and make urgent choices about–are risks to their individual business models of having input costs imperil their profits, or risks to the entire housing ecosystem of having unmet need for affordably-priced new homes doing big damage to the housing recovery itself.

The Autumn of 2018 will go far toward revealing individual firms’ resiliency in light of these challenges, and the housing cycle’s sustainability beyond a few more months that comp positively with year-earlier data points.

This story was originally published in Builder.