The Rules is a monthly series covering important regulations in a clear manner for architecture, engineering, and construction professionals.

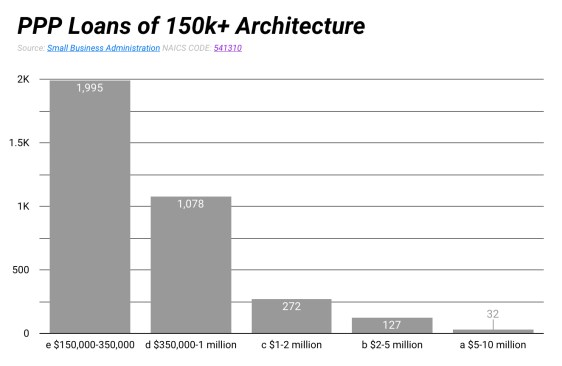

As part of the U.S. government’s $2 trillion CARES Act signed into law in March in response to the COVID-19 pandemic, the $349 billion Paycheck Protection Program provided low-interest and potentially forgivable loans for businesses to help keep their workforce employed. The Small Business Administration program has helped thousands of firms subsidize rent, utilities, and wages. As of July, 3,504 firms providing architectural services had received loans of greater than $150,000, according to public records. But how much must firms pay back and by when?

As of July, 3504 firms providing architectural services received PPP loans greater than $150,000.

For the federal government to forgive the loan in part or in its entirety, firms must meet several conditions: Namely, the loan must have been spent on sanctioned purposes—mortgage interest, rent, utilities, and other business debts—and at least 60% of the prospective amount to be forgiven must have been directed toward payroll.

Borrowers also need to show how they applied their loan toward PPP’s primary objective: keeping employment numbers similar to pre-pandemic levels. In June, Congress passed the PPP Flexibility Act of 2020. Katharine Kohm, a Providence, R.I.–based partner at the law firm Pierce Atwood, says that the most notable changes from this addendum were the extension of the loan coverage period from eight to 24 weeks and the extension of the safe harbor period through Dec. 31, both of which allow employers “more time to rehire workers without facing the reduction penalty to their forgiveness amount.” This amount may decrease depending on the ratio of the borrower’s average number of full-time employees during the loan-spending period to that between Jan. 1 and Feb. 29, 2020, or between Feb. 15 and June 30, 2019. Borrowers receiving a loan prior to the June act can decide whether to use the eight- or 24-week duration as the comparison baseline.

An Aug. 24 amendment, the Interim Final Rule, introduced exceptions for companies unable to hire staff due to a lack of qualified workers or to provide a workplace environment that meets social distancing or safety requirements. Borrowers should document their attempts to potentially avoid a forgiveness penalty for the sustained workforce reductions.

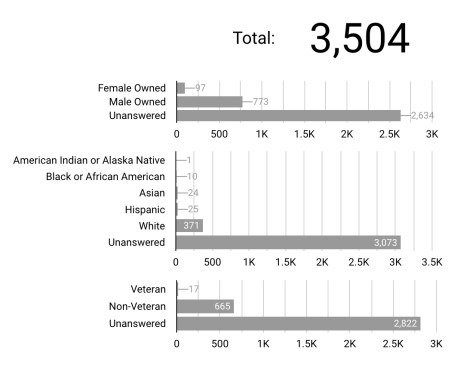

Ownership breakdown of firms offering architectural services that also received a PPP loan

While “there is no hard and fast deadline” as to when firms must begin the repayment process, Kohm says the forgiveness application currently “needs to be submitted to the lender no later than 10 months from the end of the loan-spending period,” whether that be eight or 24 weeks.

To begin the repayment process, borrowers can ask their SBA lender which documents it requires. Examples include “bank account statements, third-party payroll reports, canceled checks, invoices or billing statements, payroll tax forms, and account statements documenting the amount of employer contributions to employee health insurance and retirement plans,” says Kevin Johns, a tax specialist at Southfield, Mich.–based accounting firm Clayton & McKervey. The bank will then review the loan forgiveness form before submitting it to the SBA for approval.

Businesses should monitor the PPP for future developments because the forgiveness rules continue to evolve. The August Interim Final Rule, for instance, suggests that any expenditures toward rent will be forgivable to the extent that the underlying property owned by a related party has paid interest on a mortgage.

This “clarification,” Johns says, means that “if there is no mortgage [on the business property], then no related party rent payments would be eligible.” He worries that lenders may not have discussed this exception with borrowers during their loan application process. However, he notes, legislation is pending that would simplify the filing process and forgiveness calculation for loans under $150,000. And that would be news some borrowers can take to the bank.

Editor’s note: This story appears in the October 2020 issue of ARCHITECT. On Oct. 8, 2020, after this story went to press, the Small Business Administration released a simplified forgiveness application for PPP loans under $50,000. This story has been updated since first publication to clarify the August Interim Final Rule regarding potentially forgivable expenditures toward rent pertains to property owned by a related party.