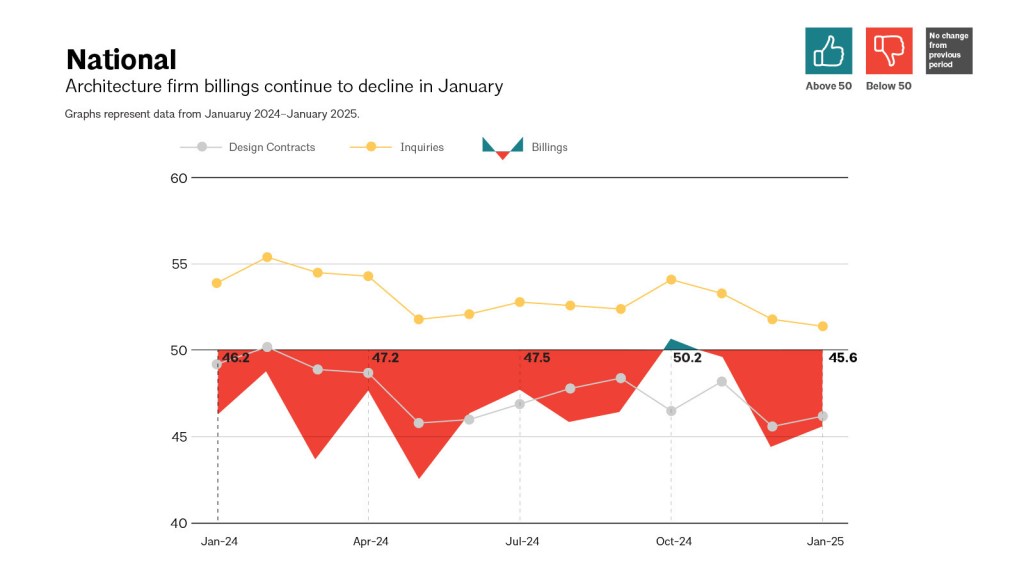

As the architecture industry navigates the complex economic landscape of 2025, the latest data from the American Institute of Architects (AIA) reveals a persistent decline in firm billings, indicating a cautious outlook among owners and developers. The AIA/Deltek Architecture Billings Index (ABI) for January stood at 45.6, suggesting a contraction in business conditions for architecture firms nationwide.

Despite a slight decrease in the proportion of firms experiencing billing declines compared to December, January marked yet another month of reduced economic activity in the sector. The ABI, a crucial economic indicator for architectural firms, reflects that any score below 50 points to decreasing business conditions.

This prolonged downturn has prompted firms to adjust their operations, trimming their workforce to align with the current demand. According to AIA’s Chief Economist, Kermit Baker, the industry saw a net loss of 1,400 jobs in 2024 alone, cumulating to a total reduction of 4,100 positions since the peak in June 2023.

The challenges facing the industry are manifold. Stubborn inflation rates, high interest rates, and labor issues continue to deter investment in new projects. The economic uncertainty continues “to weigh on the willingness of owners and developers to move ahead with construction projects,” explained Baker.

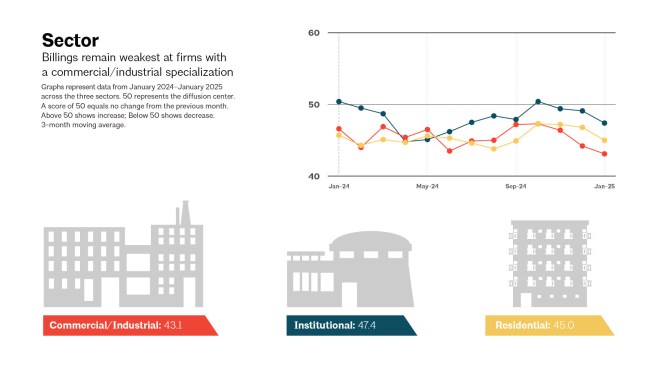

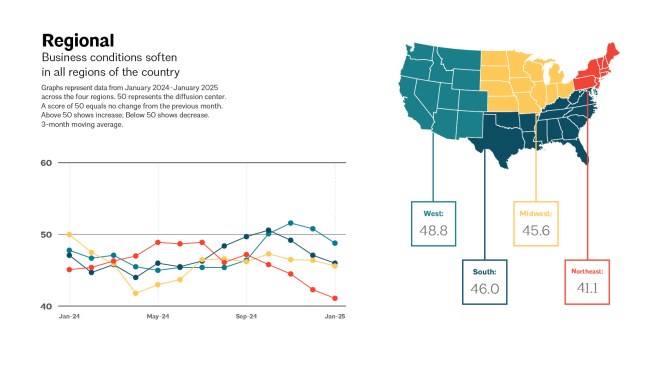

The slowdown was uniform across various regions and specializations in January. The commercial/industrial sector, in particular, faced the steepest decline in business conditions. Geographically, the Northeast was the hardest hit, continuing a trend of weak business activity in the area.

In contrast, the West fared slightly better but still underperformed relative to more stable economic conditions.

Key statistics from the ABI in January include:

- Regional averages: West at 48.8, South at 46.0, Midwest at 45.6, and Northeast at the lowest with 41.1.

- Sector index breakdown shows institutional at 47.4, multifamily residential at 45.0, mixed practice at 44.3, and commercial/industrial sectors struggling the most at 43.1.

- The project inquiries index, however, offers a glimmer of hope at 51.4, suggesting a slow but steady interest in new projects.

Despite these challenges, the industry is witnessing a modest rise in project inquiries, indicating potential for future engagements, albeit at a cautious pace. However, the value of newly signed design contracts continues to drop, marking the eleventh consecutive month of decline.

As architecture firms brace for an uncertain future, the industry’s resilience and adaptability will be tested.

For more detailed insights and historical data on billing indices, stakeholders are encouraged to visit the AIA’s official website.