This story was originally published in Builder.

As we’ve noted, builder strategies, including their land investment, community design, marketing, and operational models have pivoted in the past 24 to 36 months.

Prior to that pivot—with the exception of noteworthy outlier builders, whose product, pricing, land position, operational processes, value proposition, and strategic principles gave them a jump-start—strategic focus rightfully was fixed on a more discretionary, higher-end home buyer bent on making luxury aspirations a reality, one whose access to a relatively forbidding mortgage qualification market was a never a question.

Since the inflection in late 2015 to mid-2016, however, strategy, operations, community development, and design at a macro level has shifted—slowly at first, and now with accelerating speed—to a vast, growing, pent-up pool of entry-level would-be first-time buyers, for whom the mortgage markets once again wish to be of service.

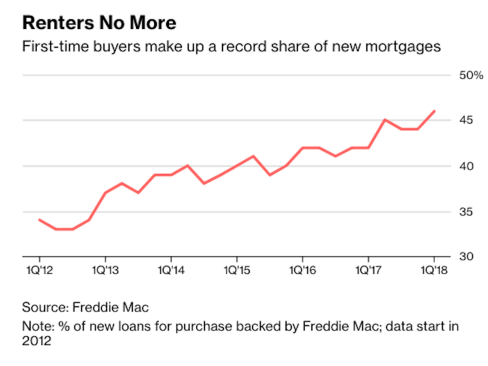

First-time buyers accounted for 46 percent of new mortgages (excluding refinancings) that Freddie Mac backed in the first quarter, their biggest quarterly share in data going back to 2012, according to the company. Meanwhile, the National Association of Realtors puts the median age of first-timers in the U.S. at 32.

In other words, it appears that young people, helped by easier credit and an improving job market, are acting fast as rents rise and a surge in property values and borrowing costs threatens to price them out of homeownership.

The sluice-gates barricading demand among younger rental refugees and other Millennial seekers and achievers of homeownership have opened, again mostly for the relatively higher end of the entry-level price elasticity spectrum, and mortgages have become more widely marketed and accessible to a bigger, newer universe of buyers.

This is a positive.

And it’s just a start.

In fact, given the directional changes in society, economics, technology, geography, and age demographics, there are at least two relatively wide-open opportunities for builders to address that will require a learning curve that they’d better get on sooner than later.

As a brief lead-in to discussion of these opportunities here’s a couple of factoids that remind us of phenomena that should really need no reminding.

One is recent data—noted here by New Strategist Press editorial director Cheryl Russell—from the Center for Retirement Research at Boston College, a report entitled “What Explains the Widening Gap in Retirement Ages by Education?” Russell writes:

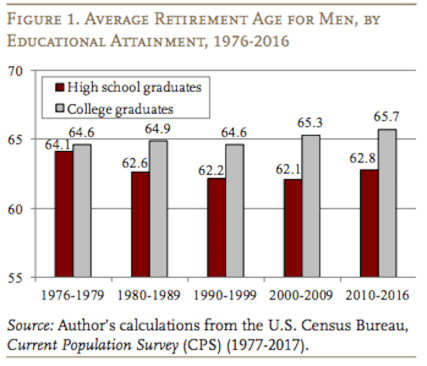

The average age of retirement is rising among men, but the increase is almost entirely limited to those with a college degree, according to an analysis by Matthew S. Rutledge of the Center for Retirement Research.

Among men with a college degree, the average age of retirement climbed from 64.6 in the 1990s to 65.7 in the 2010s—an increase of 1.1 years. For men with no more than a high school diploma, the average age of retirement rose from 62.2 to 62.8 during the time period—an increase of just 0.6 years.

Why?

Explanations vary: health, retirement financial planning, access to Social Security benefits, and marital status figure in to the reasons less educated people tend to retire sooner than those with higher educational attainment.

It also may be that the kinds of occupations less educated workers tend to pursue may be becoming obsolescent due to automation and offshoring, which means their career horizons may move up faster on them than those types of jobs and careers more educated people are in.

Too, incentives to retire when one has reached peak income levels in one’s career may be diminished, especially when financial market gyrations and volatility infuse uncertainty into personal financial and investment planning.

The other factoid is just this. The “middle class” as America once knew it and prided itself on cultivating, is threatened. Extinction of a basic belief, that work can result in upward social, economic, educational, and culturual mobility, is a real possibility. What’s a regular household, reaching the end of a regular career (or two), to do about where they live, and how they live in a post-career world?

The issue here has everything to do with the present and potential addressable market for 55-plus new homes and communities, and it has to do with defining economic and financial needs.

Just as a few outliers were all-in early on the push for entry-level primacy in their respective operating arenas—D.R. Horton, LGI, Wade Jurney, Smith Douglas, Dan Ryan Builders, to name a few—some of the same ones, and a few others, including Horton, Dan Ryan, and Epcon Communities have seized on the idea that a wave of retiring and near retirement buyers may be almost as financially boxed in in their way as young adults early in their careers.

Just as builders might be looking for flash point moments—like the purchase of an engagement ring, or the setup of a wedding gift registry, or the purchase of a pregnancy test as key instances to consider a first point of interaction for the young adult renter looking to buy, the same thinking could apply to the late-career behavioral signs for a potential 55-plus buyer.

Perhaps, it’s the moment a soon-to-retire individual signs up to become an Uber or Lyft driver to supplement income. Maybe, it’s when a couple establishes an Ebay or Craig’slist account to start purging a home of furnishings and other household items that may be of value to others.

Clearly, the really big universe in 55-plus for new-home and community developers is not the higher-end, discretionary retiree with resources to pay for a dream home for the next stage of an active life.

The truly big universe will compete for buyers with age-in-place remodels, with moves to inner circle downsized rentals, and with those who’re financially locked in where they are currently because there is no viable exit strategy.

Despite the fact that America’s 55-plus population is where the nation’s wealth and resources lie, the concentration of that wealth and those resources is held by a small share of the total population.

This speaks to one of the two thus-far “wide-open” opportunities for builders: a formalized “entry-level” 55-plus strategy that would encompass real estate, capital investment, universal design, healthy-smart home engineering, floor-plan adaptability, pricing that can compete with median rental living, and communities connected to culture, food, income options, and transportation.

Dan Ryan’s Elevate community in Raleigh, Horton’s Freedom, and Epcon‘s single-story intentional community model each address 55-plus living from an attainability, and no-fuss lifestyle angle that sets them apart from many of the 55-plus strategies of other builders, whose positioning reflects a “finally get the home you’ve deserved” pitch to near-retirement prospects.

The second wide-open business opportunity is not an entirely original or new concept, but given the kinds of “kit of parts” design and engineering likely to continue making inroads into new-home construction, it may be a more viable business model option for new residential builders.

In the spirit of housing and well-being as a service model, what an enterprising and innovative builder might do is to sell people into 55-plus homes and communities that come—over time—with an age-in-place remodel contract.

In other words, create a “componentized” floor plan that’s future-proofed to the extent that replacement contractors might 10 or so years later update, retrofit for universal design, and adapt the floor plan for a caretaker or revenue unit.

Rather than simply multigenerational, the home would have the potential to evolve along a health, economic, and financial need continuum to serve residents across a longer post-career timeline.

Just a thought.

To read more stories like this, visit Builder.