This story was originally published in Builder.

The Great Recession officially started 10 years ago, and what I dub the Anemic Housing Recovery began eight years ago. Just how bad was the Great Recession for housing?

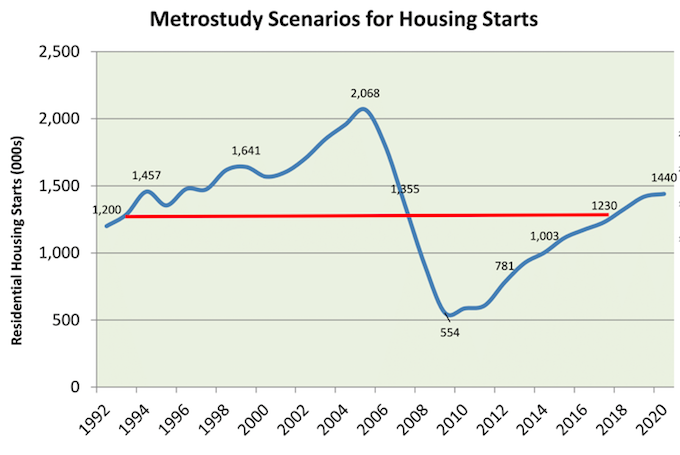

As if you don’t know, it was terrible. As it became more and more obvious that housing’s unprecedented great run from 1992 to 2007, when single-family starts exceeded 1 million units every year, would have to end, most economists nonetheless predicted a soft landing for housing, with total starts drifting down from 2.1 million to roughly 1.5 million units. That would have been well above the 1 million unit housing starts trough typical in all previous post-war housing recessions.

Boy, were they wrong. Starts dropped to 550,000 units in 2009, a 75 percent decline from 2005’s peak of 2.1 million units.

Next question: How anemic is the eight-year-old housing recovery?

Well, in the worst previous housing downturn, housing starts bottomed out in 1982 at around 1.1 million units. However, just a year later, starts soared to 1.7 million units, an almost unbelievable 60% year-over-year turnaround. In 2010, the first year of the Anemic Housing Recovery, starts inched from 554,000 units to 609,000 units. That’s only about a 10 percent increase off a woefully low base.

It took until 2014 for housing starts to reach 1 million units, and, if that isn’t depressing enough, consider this: even this year, with starts pushing 1.3 million units, housing activity will still fall below its long-term average of 1.4 million to 1.5 million units a year.

Now what? Far be it from me to forecast housing activity. I got it wrong in 2007 and expected the recovery to accelerate strongly about five years ago. So no more wishful thinking from me. (Except about the Super Bowl: I see my hometown Steelers winning it.)

If we stick to housing, I’ll turn over the task of helping you understand where it is headed to Mark Boud, chief economist for Metrostudy, a housing data and analytics sister business to BUILDER. As he sees it, housing starts will continue their long, slow-but-steady climb through 2020, when they will reach 1.45 million units—finally equaling the industry’s long-term average. Other key takeaways from his 2018–20 outlook include:

- The national housing market is under-supplied and will remain so through 2020.

- Overall housing prices are somewhat overvalued, but much less so than in 2005–06.

- In most markets the window for land purchases and land development will remain open for two more years.

- The market is top heavy with high-priced housing and a glaring shortage of starter homes.

Boud’s full forecast is available here. And remember that when it comes to housing starts, up, even a little, is better than down.

To read more stories like this, visit Builder.