When mortgage interest rates dropped between 2% and 3% in 2020 and 2021, people rushed into the housing market. For a while, the low rates enabled consumers to get more bang for their buck by pushing down monthly mortgage payments even as home prices rose. The elevated demand, however, was not met with a similar level of supply. Resale inventory was snatched up quickly, and builders found they could not bring homes to the market fast enough given constraints on land, labor, and materials, plus governmental delays. The impact was a massive run-up in home prices over a historically short period of time. Through early 2022, consumers proved willing and able to look past the high top-line pricing in return for locking in a low 30-year, fixed-rate mortgage. That willingness turned into reluctance earlier this year when mortgage interest rates shot up, causing a record affordability shock.

As the rate on the 30-year, fixed-rate mortgage rose from 3% to 6% this year—according to data from Zonda, ARCHITECT’s parent company and the largest home-building property technology company in North America—some 16 million households were priced out of the market. With rates now flirting with 7%, the number is closer to 21 million households. Further, Zonda’s affordability ratio captures that just 39.5% of households can afford the median-priced home nationally, down from 51% at the start of 2020.

While the affordability pressure is slowing the conversion to homeownership for many Americans, it is also forcing additional creative thought from the development community.

Many of the markets that saw rapid home price appreciation over the past couple of years were historically more affordable—ones where home prices and incomes were within a somewhat reasonable range. As we look at these markets, many spread across the South and Midwest, we see potential for land planning and new home product.

Even a modest change in the kind of homes being built can help address affordability; denser land planning and smaller homes generally allow for lower average selling prices. Builders in these markets are now looking at higher-density, single-family detached homes, changing the level of finishes within homes, adding accessory dwelling units where policy allows them, and, notably, constructing more attached homes such as condos, town houses, and duplexes, which are generally more affordable.

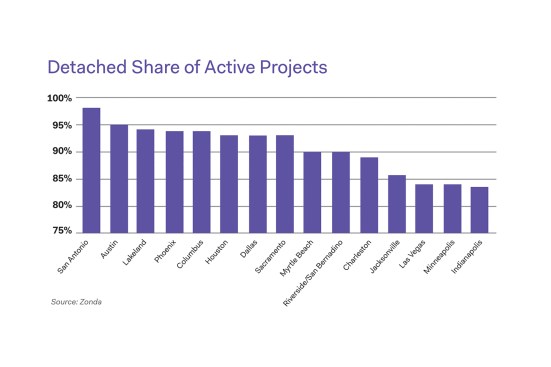

As of September 2022, 79% of new home projects are single-family detached homes, down slightly from 81% in 2018, per Zonda data. As always with housing, though, the rate varies by metro area. For instance, about 98% of active projects are detached in San Antonio, roughly 94% in Phoenix, and 93% in Dallas. In markets like these with a high share of detached homes, building more attached dwellings, especially at entry-level price points, can go a long way toward expanding homeownership.

Conversely, in traditionally more expensive markets, attached product has represented a large share of new home projects for years. In New York, 87% of new home projects are attached, with 64% in San Francisco and 56% in Washington, D.C., per Zonda data.

Affordability will continue to be a headwind given high land prices, elevated inflation, regulatory costs, and growing borrowing costs. We need to focus on controlling what we can, including home design. Homes that address consumer must-haves, while also accounting for affordability, can help drive sales and increase homeownership.

This article first appeared in the November/December issue of ARCHITECT.

Read more: Phyllis Kim on embedding yourself in the community|Melanie Fairchild and Jessica Dole on parental leave in the architecture profession|Gabriel Keller on alternative pathways to professional licensure