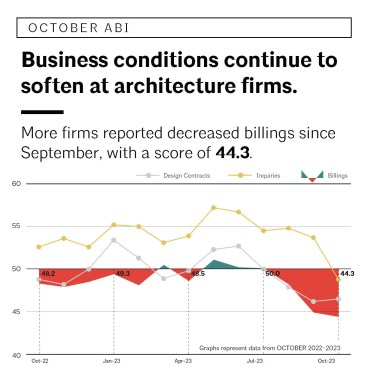

The American Institute of Architects monthly Architecture Billings Index posted at 44.3 in October, dipping slightly below the score of 44.8 in September. For the third consecutive month, the ABI score was under 50, indicating that a significant share of firms is seeing a decline in billings.

“This report indicates not only a decrease in billings at firms, but also a reduction in the number of clients exploring and committing to new projects, which could potentially impact future billings. The soft conditions were evident across the entire country as well as across all major nonresidential building sectors,” said Kermit Baker, PhD, AIA Chief Economist.

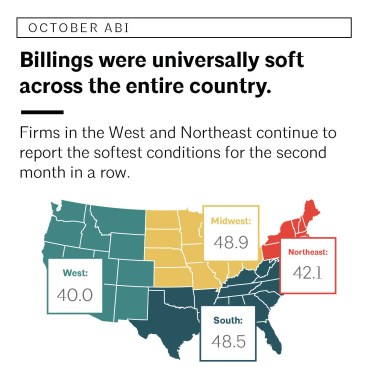

The score of 44.3 for October dipped slightly below the score of 44.8 in September. Billings were universally soft across the entire country in October, with firms located in the West and Northeast continuing to report the softest conditions overall for the second month in a row.

Key ABI highlights for October include:

• Regional averages: Northeast (42.1); South (48.5); Midwest (48.9); West (40.0)

• Sector index breakdown: commercial/industrial (43.7); institutional (49.1); mixed practice (firms that do not have at least half of their billings in any one other category)

(44.0); multifamily residential (40.1)

• Project inquiries index: 48.8

• Design contracts index: 46.5

The ABI is a leading economic indicator of construction activity in the U.S. and reflects a nine- to 12-month lead time between architecture billings and construction spending nationally, regionally, and by project type.

The ABI score is a leading economic indicator of construction activity in the U.S., providing an approximately nine-to-twelve-month glimpse into the future of nonresidential construction spending activity. The score is derived from a monthly survey of architecture firms that measures the change in the billings from the previous month.

The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

A score above 50 represents an increase in billings from the previous month, while a score below 50 represents a contraction.

Read more business news: March Billings Improve | Decline Slows for December Billings | Billings Slow Again in November | Moderated September billings reflect pressures in housing market