While the music industry was upended by Apple, the taxi industry by Uber, and the entertainment industry by Netflix, the construction industry had largely escaped notice. But the reprieve has ended. A number of tech companies have made their move, flush with the capital to cause significant disruption.

In 2015, Alphabet, the parent company of Google, launched New York–based Sidewalk Labs, an organization that aims to build Quayside, a new neighborhood in Toronto that “combines the best in urban design with the latest in digital technology.” In 2016, Tesla announced its entrée into the roofing business with a photovoltaic shingle designed to “complement your home’s architecture.” And last year, Airbnb unveiled plans to apply its disruptive business model “more broadly to architecture and construction,” throwing away conventional wisdom to “prototype new ways that homes can be built.”

A plethora of startups have also emerged, each of them promising to reimagine aspects of the building industry. Prefabrication startups FullStack Modular, Kasita, and Blokable are each attempting to create a manufacturing-style production system for buildings. Well-funded, vertically integrated organizations, namely Katerra and WeWork (where I previously worked as director of research), bring design, construction, and operations in-house rather than contracting it out. The list of startups setting up shop at every corner, every market, goes on: Hypar and Higharc are tackling design software, Leko Labs is taking on fabrication systems, and Test Fit, Spacemaker, and ArchiStar are upending estimating software.

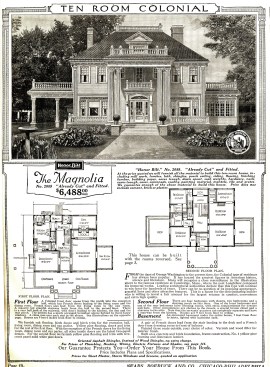

Sears Magnolia kit house from the Sears Modern Homes catalog (circa 1921)

Rhino Retrospective

Of course, the profession is no stranger to part-ambitious, part-naive upstarts from the outside. For example, Sears, Roebuck & Co. began selling housing kits direct to consumers via mail-order catalogs in 1908. Largely known for its department stores, Sears sold 70,000 houses this way, with production only ceasing due to material shortages during World War II.

In a similar vein, tech entrepreneurs have been pushing the industry forward for decades, although not at the scale we’re seeing today. Take the example of 3D modeling and visualization program Rhino, which Seattle-based Robert McNeel & Associates began developing in 1992. Founder and CEO Bob McNeel tells me that though a dozen 2D drafting companies existed at the time, only two would become wildly successful: Bentley Systems, the maker of MicroStation, and Autodesk, the maker of AutoCAD. During these early days of CAD, investors were more interested in companies like Adobe, which already had a large user base. What his company was doing, McNeel says, was “so specialized and narrow that nobody paid any attention.”

Instead, McNeel & Associates was initially funded through consulting gigs, developing AutoCAD plug-ins and content for various architecture firms—“bootstrapping” in today’s startup parlance. Its main competitor in the 3D modeling space was Alias, which cost tens of thousands of dollars per license. (Alias was acquired by Autodesk in 2005 and still costs an inordinate amount of money.) By introducing a lower-priced product, Rhino disrupted the market and began to take off. Since McNeel & Associates had no outside shareholders, it could decide its fate without the pressure that many of today’s investor-backed companies face to grow at any cost.

The company proceeded cautiously, avoiding seemingly obvious markets to instead develop tools for other businesses to pursue said markets. “If they’re building something that makes Rhino more useful, we’ll do whatever we can to help them all out,” McNeel says. “I don’t know how else to think about it.”

The result was a growing ecosystem of startups and consultancies that are built on Rhino. Responding to requests from these businesses, McNeel & Associates has begun developing Rhino Inside and Rhino Compute, two platforms that make Rhino’s geometric engine available in other software, something that may fuel the next generation of disruptive startups.

Lumion LiveSync is one example of a collaboration between Rhino and other tech platforms.

Today’s Dollars

Investment in the construction space today dwarfs everything in the past. It’s difficult to calculate exactly how much is being invested, but one estimate by CREtech puts the figure upward of $12 billion into real estate startups—which includes construction, co-working, and underwriting—in 2017, with another $10 billion in 2018. For comparison, the U.S. architectural services industry altogether is worth about $45 billion, according to AIA.

For the most part, investors aren’t going after architects, but rather the real prize: the $10 trillion global construction industry. A February 2017 McKinsey Global Institute report advocated for dramatic changes to the design and construction sectors, arguing that a manufacturing-style production system would boost productivity and save $1.6 trillion per year.

As companies battle to capture parts of this enormous industry, architects are finding themselves at the mercy of these larger changes in the economy. Many firms I’ve spoken with are unfazed, seeing their work as distinct to these new ventures. But others expressed real concern that they are losing work and employees to well-funded newcomers.

Some AEC companies have seized the opportunity to start their own business offshoots. New York–based Thornton Tomasetti launched TTWiiN, a discrete incubator that has partnered with venture capitalists to commercialize the firm’s innovations. In Amsterdam, UNStudio started UNSense, a startup aimed at “integrating sensorial adaptive design into architectural output.” And Philadelphia-based KieranTimberlake has tried productizing some internal tools, including Tally, a platform for calculating the environmental impact of building materials; Roast, a survey platform for measuring occupant comfort; and Pointelist, a sensor network for buildings.

KieranTimberlake

Pointelist components

Whether these efforts will succeed remains to be seen. Selling products has its own unique challenges when it comes marketing, product support, and finance. For a firm accustomed to billing services by the hour, it may be difficult to introduce and support a product-based revenue stream.

Meanwhile, some academics sense change is in the air and are preparing their students for the new reality. At Yale University, Phil Bernstein, FAIA, teaches a course that challenges students to devise an architecture firm that creates profit through something other than fixed or hourly fees. MIT’s School of Architecture and Planning has started DesignX, an incubator that helps students and faculty launch business ventures related to the built environment. Courses teaching students to write business plans and launch startups can seem dull compared to the conventional Instagram-ready curricula, but they offer skills that are as central to the future of our profession as any aesthetic innovation.

Mission Versus Money

Overall, it’s a good time to be an architect—but a precarious time to own an architecture firm. Architects have more opportunities than ever to branch out, start companies with new business models, and join organizations outside the industry with better working conditions.

Architecture firms, however, have a lot hanging in the balance. Small boutique firms are likely immune from most of these changes, the same way bespoke tailors survive in a world of mass-produced fashion. Larger firms are more likely to face headwinds, particularly in sectors where they face well-funded competitors that are willing to lose money to gain market share.

The onslaught of outsiders eyeing architecture is significant. In the canon of architecture, the heroic catalyst of change has been designers: Frank Lloyd Wright conjuring the prairie house, Denise Scott Brown, Hon. FAIA, and Robert Venturi giving us permission to love Las Vegas and Postmodernism. In the future, the new agents of change may be consigned to nameless venture capitalists and indomitable tech giants.

Daniel Davis is a regular columnist for ARCHITECT. His views and conclusions are not necessarily those of ARCHITECT magazine nor of The American Institute of Architects.

Note: This article has been corrected since first publication to state that Robert McNeel & Associates found itself among a dozen 2D drafting companies in the early 1990s.