This story was originally published in Builder.

If.

For any business, business sector, or business cycle, it’s one of the bigger, more meaningful tiny words.

For housing, durable and thriving businesses navigate a tricky path that threads both conditions and a conditional.

That jobs report. That quarterly GDP reading. That changing Fed rate. Wages. Corporate profits. Debt levels. Demographics. These are the conditions, a set of key performance indicators that reveal capital flow, capacity, and the contour and magnitude of demand in raw materials form.

The conditional comes down, in some form or fashion, to consumer sentiment, to confidence, to expectations, and how each of those figures into hopes and dreams. What’s more, while these phenomena go on at an individual level, they’re quite contagious.

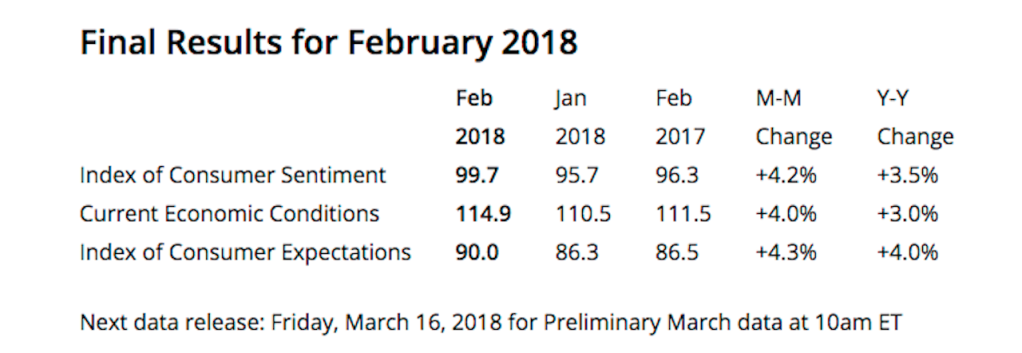

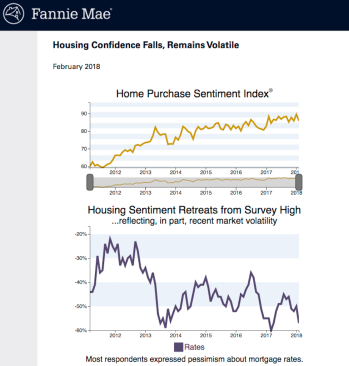

The University of Michigan Survey of Consumers reflects strength in sentiment, conditions, and expectations. What’s more, the Conference Board’s Consumer Confidence Index rose last month, and stands at its highest level since 2000, mostly stemming from jobs momentum. Fannie Mae’s Home Purchase Sentiment Index, on the other hand, appeared to pivot to the negative after new tax laws and rising mortgage rates introduced a new level of volatility into the measures.

To listen to Fannie Mae VP and chief economist Doug Duncan, tax and monetary policy are doing a number on people’s sense that it’s a good time to buy or sell, and stirring anxiety–believe it or not–on the job security front as well. Duncan’s observation:

“Volatility in consumer housing sentiment continued into February, with the new tax law beginning to impact respondents’ take-home pay and the stock market creating negative headlines due to early-month turbulence,” said Doug Duncan, senior vice president and chief economist at Fannie Mae. “Additionally, consumers’ expectations for higher mortgage rates suggest that consumers expect the Fed to hike rates a few more times in 2018. We will continue to track how consumer housing attitudes trend in the coming months as these various market forces play out.”

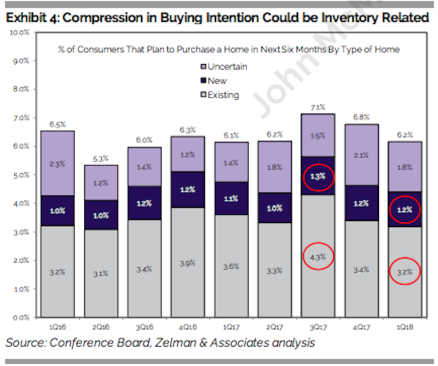

The latest The Z Report, Zelman & Associates’ twice-monthly collection of data-evidenced analyses on housing and real estate hot button themes, takes time out to look at the correlation and the implications of various consumer confidence and sentiment benchmarks.

One of the intriguing conclusions Zelman derives from the variously sourced consumer sentiment data points is that, writ large, confidence directionals that run counter to the interests of some parts of the housing spectrum may actually favor others. What’s a negative for existing home sales and apartment rentals—vis a vis confidence—may be a positive for new home sales. Here’s the Zelman conceit:

“In summary, paraphrasing the hypothetical entry-level housing consumer, prices are rising because inventory is tight, which is frustrating, and interest rates are starting to edge higher, but mortgage credit is available, affordability is still good and I’m tired of paying higher rent every year. So I’m still interested in buying, but it is looking like I should start considering new construction.”

So, a potential entry-level home buyer’s confidence, rationale, and current means of cobbling down payment and carrying costs—even if things are a little tight at the outset—match up almost identically to a home builder’s confidence as he or she eyes that tract of lots in a path-of-growth submarket that might be attractive to the entry-level buyer. Rates, prices, and tax incentives matter only insofar as how they each relate to confidence that there’ll be more than enough means to cover for all of their increase with earnings and even better expectations.

And this is a housing market recovery, such that it is.

A lot of ifs.

To read more stories like this, visit Builder.